Sassy Resources (CSE: SASY) / (OTCQB: SSYRF) is a newly-listed, high-grade, gold-silver play with two Canadian projects. The crown jewel is in the world famous Eskay Camp of B.C.’s Golden Triangle (“GT“). Its 100%-controlled Foremore project is 45 km north of the legendary Eskay Creek Mine. Sassy has 29.1M shares outstanding, (49M fully-diluted), with just 15.1M currently free-to-trade.

Foremore covers 146 sq. km (14,585 ha) and contains a number of high-grade, gold-silver targets with select, strong showings of zinc, lead & copper. Regional neighbors include — Newmont’s/Teck’s Galore Creek to the NW, Copper Fox’s/Teck’s Schaft Creek to the North, Enduro Metals’ Newmont Lake to the SW and Skeena Resources (Eskay Creek, Snip), Garibaldi (E&L, Casper), Metallis, and Eskay Mining to the South.

Sassy initiated its first drill program on July 20th. The first (11 holes) of two phases has been completed. Management will release results as received & analyzed, with the first few assays out by the end of August. Phase 1 drilling was followed by borehole electromagnetic surveys in each zone along the multi-km long historic More Creek corridor.

Sassy Resources is a spinout from Crystal Lake Mining (now called Enduro Metals). Crystal Lake negotiated the option for the Foremore project 15-16 months ago, in an entirely different market. As such, management is benefitting from attractive terms (1.25M shares of Sassy + $300k in cash over four years). The property is subject to a 3% NSR of which 2.5% can be clawed-back by Sassy for a total of $3M.

Critical takeaways from my initial review of Sassy; 1) flagship asset is an attractive, sizable property in the heart of the Eskay Camp, (and center of the GT), with ample historical exploration, incl. 71 drill holes, 2) management, board & advisors are outstanding, especially for a company with an Enterprise Value (“EV“) {market cap + (0) debt – (~$2M) cash} of just $14M, and 3) valuation + airtight capital structure is compelling.

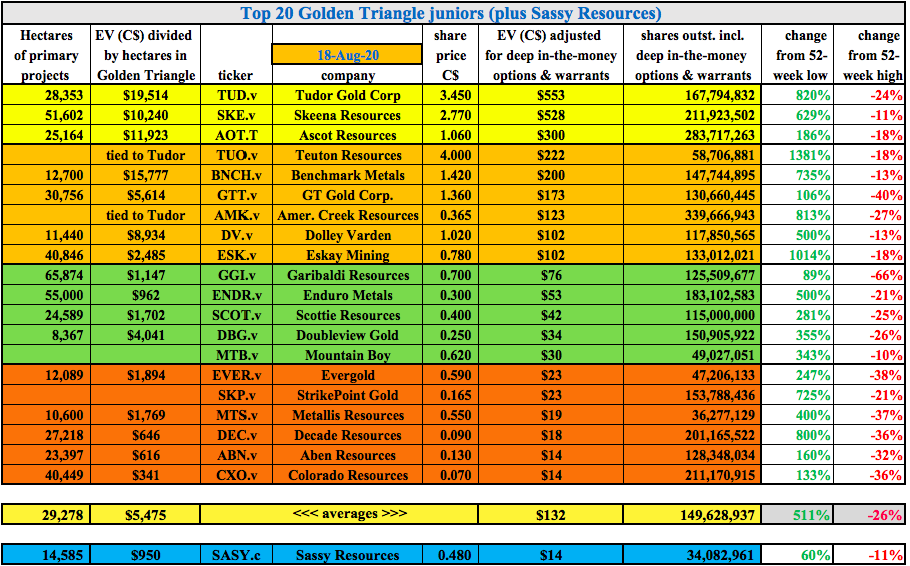

I’m tracking 480 gold-heavy juniors with market caps between $3M & $999M. Including Sassy, 34 have significant properties in the GT. The average gain of the top 20 GT juniors is +511% (from 52-week lows). The top 5 are up an average of +966%, the top 10, +792%. Compare that to Sassy at $0.47, up +57% from its last capital raise at $0.30.

Of course, this comparison is not apples to apples because Sassy did not suffer through the COVID-19-induced March selloff. On the other hand, it hasn’t benefited from the precious metal frenzy that has driven peers to all-time highs. Few know much about this company, it started trading two days ago!

The chart above depicts the top 20 pre-construction GT companies. Sixteen are pre-maiden resource. Notice that the average # of outstanding shares = 149.6M. Sassy has 34.1M. (Note: I add deep in-the-money options + warrants to company share counts, Sassy has 5M warrants struck at $0.10).

I don’t mean to suggest that Sassy’s stock will necessarily move a lot higher, but I see plenty of room to grow without running into peer valuation concerns. There are relatively few precious metal juniors, with great management teams & projects, in safe, prolific high-grade jurisdictions — with substantial near-term discovery potential & low share counts — that haven’t already soared.

The GT is one of the best performing gold districts on the planet. Yet, giant returns in gold-silver juniors are widespread. Of my 480 names, 236 (49.2%) have been (at least) 4-baggers (+300%) off their lows. Ok, enough about how hot the market is. What makes Sassy so interesting?

Sassy Resources, high-grade project, high-grade team

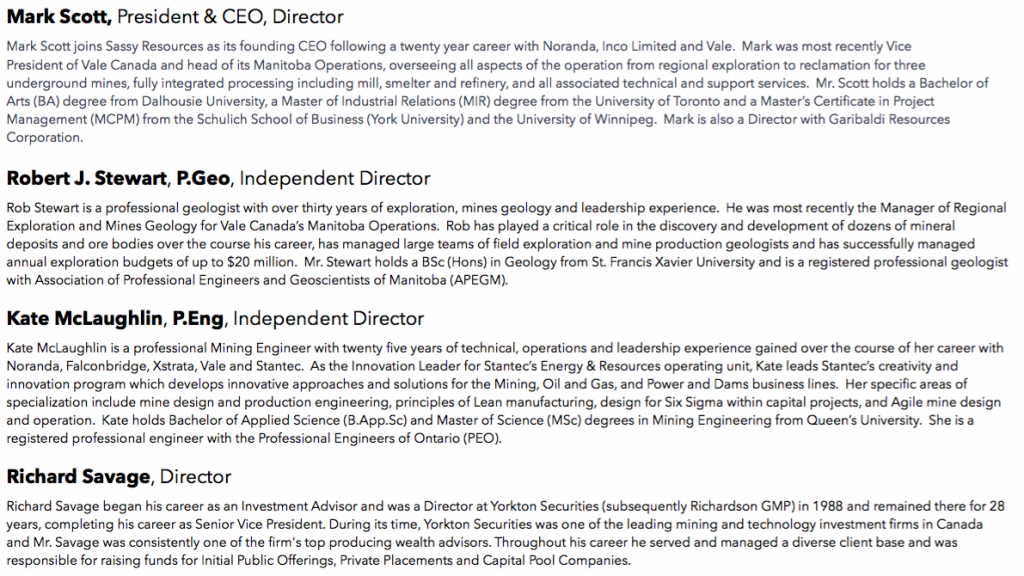

First, as mentioned, a tremendous mgmt. team, board & technical advisors. President, CEO & Director Mark Scott is a mining rockstar with 20 years’ experience at Noranda, Inco Ltd. & Vale.

He has run large operations, overseeing everything from exploration to reclamation for three underground mines and fully-integrated processing facilities, incl. mill, smelter & refinery. Mr. Scott brings a wealth of experience in mining, processing & exploration operations, strategic planning, business & organizational development.

Many mining / metals juniors of similar size & exploration stage have 3, 4, maybe 5 senior-level, highly experienced mining professionals (incl. advisors) involved. Sassy has at least seven. Instead of me describing each of them, their bios can be seen above & below.

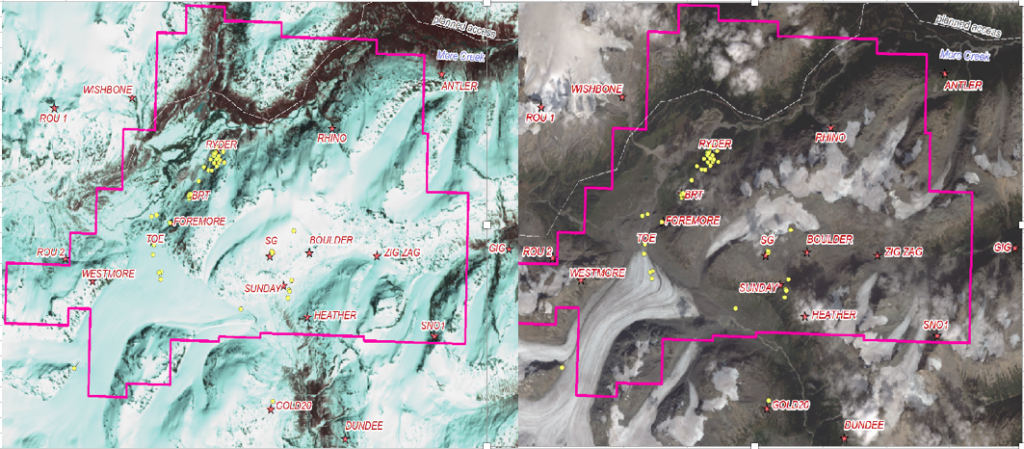

How good is the Foremore prospect? It’s of good size and is vastly underexplored. A big reason why is that 35 years ago snowpack & glaciers covered > 90% of the project area. Look below at the very dramatic before & after pictures, 1985 vs. 2019.

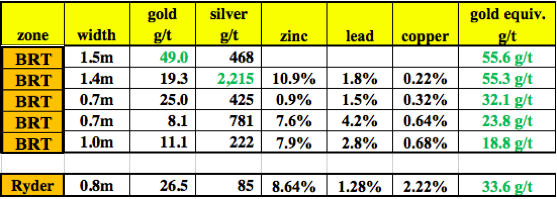

The best historical drill intercepts from a total of 71 holes:

Notice that these highlights are from just 2 of 12 named mineral occurrences. In addition to following up on these great historical assays, a lot more work is going to be directed at the Westmore / Toe / SG / Boulder / Zigzag / Sunday & Heather zones. Note: {in a follow up article I will describe exploration results and future plans in greater detail}.

Exploration in the area of the Foremore property dates back > 30 years. It includes prospecting, mapping, sampling, airborne & ground geophysical surveys & 71 diamond drill holes. Nearly an estimated $15M has been invested over the decades, probably > $20M in today’s dollars.

That’s well more than the current EV. I believe the considerable value of the historical exploration is increasing along with the price of gold & silver.

The most significant work was completed by Cominco Ltd. from 1987 to 1996, followed by Roca Mines Inc., mostly from 2002 through 2008. No diamond drilling has occurred at Foremore since 2008, as Roca went bankrupt due to an ill-timed molybdenum transaction.

From July 25 to September 20, 2019, a surface prospecting, local geological mapping & geochemical sampling program was undertaken. Sassy collected 573 samples and received noteworthy results.

At spot prices, the best 16 samples range in gold equiv. grade from ~16 g/t to ~150 g/t and averaged ~44 g/t. Although dominated by impressive gold & silver values, there were some significant contributions from zinc, lead & copper as well.

** Snowpack / glacier cover of Foremore property: 1985 vs. 2019 **

Tight share structures make a big difference in junior mining

Management stated that 15.1M of 29.1M shares are currently free-trading. Two private placements done in May (5.7M) & July (6.5M) become free-to-trade on September 22nd & November 29th.

Some of the very best junior stock performances come from companies with under 60M shares outstanding. Perhaps you’ve heard of Great Bear Resources? 50M shares outstanding, it’s up > 7,000% from its low in 2018. How about GT superstar Teuton Resources? Also 50M shares outstanding, up > 4,000%. I could go on….

I realize I sound promotional with these peer performance references, but we’re smack in the middle of an epic precious metals bull market. Gold is up +70% from its 2018 low. Silver is up +131% from March of this year!

I believe precious metal prices will remain strong, and perhaps even continue climbing. The U.S. presidential election and ongoing uncertainty surrounding COVID-19 will be with us for at least the next 6-9 months.

Management plans high impact, high-grade N. American acquisition(s)

Management plans to make meaningful acquisition(s) of high-grade properties / projects in N. America. The stated goal is to pursue trending metals such as gold & silver, but also possibly battery metals like nickel & copper. Having multiple projects diversifies exploration risk and allows for year round exploration.

Acquisitions of high-grade projects make a lot of sense in both bull & bear markets. Higher grade provides a margin for error & increased mine plan flexibility. Management believes juniors should explore & make discoveries, not spend giant sums (relative to market caps) to drill. I wholeheartedly agree. This strategy helps ensure that Sassy’s tight capital structure remains intact.

CONCLUSION

Investors in precious metal juniors can chase hot stocks, many up 500%+, or take a closer look at Sassy Resources. If the Company reports strong drill results, it might not take much trading volume to send the stock a lot higher. Only 15.1M free-floating shares until September 22nd, when 5.6M more hit the market.

As good as this mgmt. team is, I’m very interested in seeing the new properties / projects that potentially come into the Company. CEO Scott promised to remain vigilant about protecting Sassy’s capital structure.

No one can predict the future. I can’t tell readers that gold & silver prices will continue to march higher. However, I can say with confidence that high-grade assets are incredibly robust & valuable in bull markets. Sassy Resources (CSE: SASY) / (OTCQB: SSYRF) is in the right place at the right time with the right project, people & strategy.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Sassy Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Sassy Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Sassy Resources was an advertiser on [ER] and Peter Epstein owned zero shares, options & warrants in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.