The following Interview with Chris Berry of The Disruptive Discoveries Journal was conducted in the week ended June 26th. I, Peter Epstein, CFA, MBA have no prior or existing relationship with Chris Berry or any of his business interests. This is Part 3, the final chapter, of my Lithium Market commentaries from Chris Berry, Joe Lowry & Simon Moores. Please click on links to prior interviews provided at the bottom of this article.

Please provide readers with an overview of the supply side of the lithium market including possible risks to supply

The lithium market can best be characterized as an oligopoly. The major producers include FMC Corp, Sociedad Quimica y Minera de Chile (SQM), Albemarle Corp, and Sichuan Tianqui with other production in China as well. These major producers are responsible for nearly 90% of global lithium production. The USGS reported that 36,000 Metric tonnes, “Mt” of lithium metal was produced globally in 2014, equating to approximately 160,000 Mt of lithium carbonate equivalent, or “LCE,” a conventional way to compare lithium volumes.

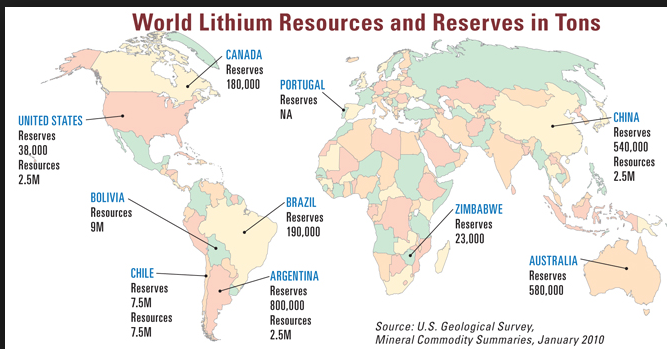

The majority of lithium supply originates in South America (the lithium triangle in Bolivia, Argentina, & Chile), Australia, and China. There are a crop of junior lithium companies that are also aiming to join the rank of producer in the next five years. The main risks for new entrants is the ability to secure off take agreements and obtain adequate financing for capital expenditures. The average cap-ex of the 4 companies that appear to be closest to production is $337 million.

Risks to supply include inclement weather (both lithium brine and hard rock projects have been impacted), ability to obtain financing, and resource nationalism, or governmental interference. Company specific challenges among majors SQM and FMC include political battles and production caps in Chile and Argentina, respectively.

The next logical question, what are your thoughts on the demand side? Are there wildcards that could challenge the conventional wisdom that demand will come entirely from batteries?

Given the relatively small size of the market, I like to say that lithium punches above its weight class. Lithium demand is growing anywhere from 8 to 10% per year mainly due to growth in the lithium ion battery business. I don’t see any wildcards at this point that could change that. Lithium is used in a number of different industries including ceramics and pharmaceuticals, that are growing more in line with global GDP. While unexciting, it offers a steady growth profile. One factor to monitor is research & development focusing on building batteries with longer life or more power density. The possibility exists that a breakthrough in this regard could potentially harm lithium demand if less lithium is required or alternative cathode materials are incorporated. I think this is highly unlikely any time in the next decade.

How important is the growing use of lithium in alloys such as lithium/aluminum for key components of airplanes, cars, etc?

Circling back to my comment on research & development, various alloys for aerospace and auto applications should be included here as well. Scandium, titanium, and other alloys are being experimented with or used on a smaller scale. Lithium appears to be the front runner, offering an optimal blend of light-weight and strength at an acceptable cost. I don’t expect alloys to become a huge source of demand, but as an example, Alcoa supplies airframes to multiple airframe manufacturers including Airbus and Boeing. Boeing said that it has contracted $100 million in lithium-aluminum alloy revenues to 2017 and has expanded production capacity to produce 20,000 Mt of lithium-aluminum per year. The preferred materials will demonstrate the optimal properties and offer the most attractive economics to manufacturers and consumers. Clearly lithium is a front runner here.

On a global scale, how important is lithium? Is it listed as a “critical metal” in any countries? Is there stockpiling lithium?

As fond as I am of lithium, it’s not terribly significant on a global scale today. Lithium is critical for next generation tech and will remain so for quite some time. That said, lithium can literally be found everywhere. Even if lithium demand were to continue on its impressive growth trajectory, it would still only be about 400,000 Mt LCE by 2025. In 2010, the US Department of Energy published a report which labeled lithium as critical to clean energy growth but only moderate in its supply risk. Despite its small overall size, secure supply will remain critical for technology supply chains. This is especially important as new energy infrastructure is built, such as distributed generation with solar and energy storage systems through batteries.

Regarding the Lithium Triangle of Argentina, Chile & Bolivia, any comments on the risk of possible supply disruption due to politics or other factors?

Despite the lengthy history of lithium production from that part of the world, a looming Presidential election in Argentina and a more vociferous government in Chile promise to increase the potential for supply disruption. Bolivia, once called the “Saudi Arabia of lithium” remains a highly challenging destination for investment based on the threat of expropriation. Adverse weather in the region in recent years has also harmed production.

It’s difficult to predict how (or if) anything will play out, but an understanding of potential alternate suppliers in other parts of the world such as Australia, the U.S, Europe and Canada is warranted.

What properties of lithium, the lightest metal, are essential in making it such an important component in many applications?

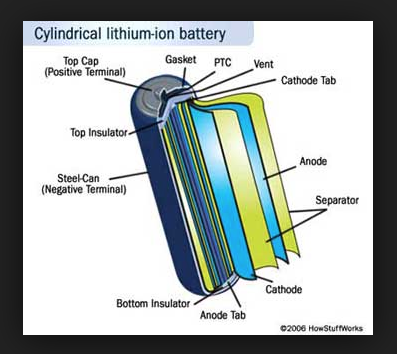

Lithium is the lightest of all metals. It is for this reason that lithium ion batteries are usually preferable to other chemistries like lead acid. Used in a car, lithium ion batteries reduce overall weight, improving efficiency. As the cost per kilowatt hour continues to fall for lithium ion batteries (currently declining at about 14% per year), we should see them replace most lead acid batteries in the future. With respect to consumer tech, while the lithium ion battery was developed decades ago, it wasn’t until the early 1990s when Sony became the first to commercialize the technology in its video recorders.

Has the use of lithium in batteries and large-scale Energy Storage Systems become the go-to metal? Or, are other battery chemistries a near or intermediate factor?

For now, the answer to your first question is yes. As mentioned, there’s a substantial amount of R&D taking place and it seems that every week a new battery breakthrough (lithium air, zinc bromide, aluminum air, etc) is announced. While these are newsworthy, these technologies are not scalable and won’t be for quite some time, if at all. For this reason, lithium ion chemistry will remain dominant – probably for a decade at least. Still, when lithium demand slows, there will remain a very substantial installed base that needs to addressed.

An important question to ask battery manufacturers as they ramp up production is how they’ll be able to shift production methods should a new and more beneficial battery chemistry emerge.

How important is grade? In sectors such as graphite, grade is frequently considered of paramount importance

Grade is important, but not the most important factor. Regarding my previous comments on lithium brine versus hard rock mining, the processing methodology is what determines the ultimate cost. There’s also an opportunity cost here. Though lithium brine production is cheaper on a per Mt basis, the roughly 18 months it takes to precipitate lithium from giant evaporation ponds represents an opportunity cost that’s difficult to quantify.

What are the main differences between hard rock mining and harvesting lithium through brines? Does each approach end up with roughly the same end products?

Elaborating on what I said earlier, yes, each process results in the same products, depending upon what one is aiming for. Brine production versus hard rock is essentially chemistry versus old fashioned conventional mining. Each have separate cost structures and operating benefits. However, lower operating expenditures are associated with lithium brine production.

Thanks as always Chris for your time and expert opinion. For ongoing commentary and analysis by Chris Berry, please visit The Disruptive Discoveries Journal

Part 1 Interview with Joe Lowry of Global Lithium LLC

Part 2 Interview with Simon Moores of Benchmark Mineral Intelligence

Leave a Reply

You must be logged in to post a comment.