The following interview of lithium expert / consultant Joe Lowry of [Twitter] Global Lithium LLC was conducted over the past 6 days by phone and email. The opinions, views and purported facts herein are entirely those of Mr. Lowry. His vast experience in the lithium industry makes his commentary well sought after. I’m thankful that Joe is willing to provide insightful market intelligence, information that most investors don’t have access to. I have no prior or existing relationship with Joe Lowry or any of his business interests.

You’re known as, “Mr. Lithium.” Please explain how you rose to lithium prominence? What does your firm Global Lithium LLC offer clients?

Not sure I’ve, ‘risen to prominence,’ but thank you for the compliment. The, ‘Mr. Lithium’ thing evolved over time. Almost 20 years ago, someone in Japan called me, Mr. Lithium in a group meeting and gradually the name spread. I lived in Asia for more than a decade beginning in 2000. I think some people found the, ‘Mr. Lithium’ moniker easier to remember than my real name.

[Linked-In] Global Lithium LLC has a broad cross section of clients. We are able to provide real time information and perspective that clients continue to value. Twenty-five years of lithium knowledge and relationships cannot quickly be replicated. Lithium is a small niche market albeit growing rapidly in significance.

Without divulging the, “secret sauce,” please explain how you collect industry data and actively monitor / participate in the industry?

The value that Global Lithium LLC offers boils down to relationships built over time, working in the lithium business, living in multiple countries and traveling to many others on a regular basis. We also monitor import & export statistics and other data sources, but again, it takes knowledge and experience to properly interpret limited available data.

As a, “lithium 101” type of question, what are the primary lithium compounds and what are they used for?

There are many lithium products but since the lithium-ion battery business is the key global market, most people are interested in lithium carbonate and lithium hydroxide – the two main products used to make cathode materials for batteries. Both products can also be used as feedstocks for many other inorganic lithium chemicals. For instance, lithium chloride is a key compound given that it’s the feedstock for lithium metal required to make organic lithium compounds such as butyl lithium – a very significant part of Albemarle Corporation’s, Ganfeng Lithium’s & FMC’s lithium businesses.

Instead of hitting Wikipedia, I’ll ask you, what characteristics of lithium make it particularly amenable for lithium-ion batteries?

At this time, it’s simply the best combination of low-weight and high energy density, with a reasonable cost profile.

Lithium pricing, for some nothing else matters. Yet there’s a wide divergence of opinion. Is there a benchmark price?

Short answer no, there is no benchmark. You’re asking this question at a point in time when lithium price volatility is at an all-time high. Due to electric transportation, Electric Storage Systems, “ESS” and continued proliferation of portable electronics, lithium demand is at a tipping point. Global Lithium LLC is in a unique position to quickly spot price changes and verify if they’re short-term or regional aberrations. In some respects, we’re better positioned than producers themselves to know what competitors are doing.

The next most important metric for investors & management teams alike is demand CAGRs. Do you have forecasts of overall demand, or demand by segment?

I do have forecasts, but that information is reserved for clients. However, I will say that the overall lithium growth rate in the battery segment will be in the low-to-mid-teens percent, portable electronics, high single-digits percentage and transportation / ESS over 20% – pulling the average up.

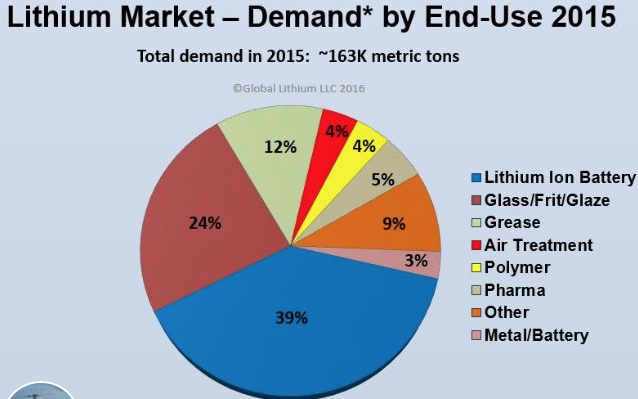

You posted on Linked-In a preliminary 2015 pie-chart depicting demand by end-use. It’s no surprise that batteries held the top rank at 39%. What might this chart look like in 2020?

Batteries will be more than half the pie chart in 2020. It’s a little early to tell how much above 50% the 2020 figure will be.

What, besides batteries, could surprise to the upside?

I see potential surprises to the upside in the battery segment, but no other segments of note. Batteries are so dominant moving forward that it’s hard to imagine anything else grabbing one’s attention anytime soon.

How likely is it that lithium demand could fall short of expectations due to substitutable materials in the lithium-ion paradigm?

I see very little risk that substitute materials will cause a negative impact to the market share position of lithium-ion batteries in the next seven years. Even if lithium-ion were to be substituted, it would likely be with a rechargeable lithium alternate, so still a win for lithium.

Reported pricing of various lithium compounds is all over the map, please provide some insight on what’s going on.

A few months ago, a number of comments regarding lithium pricing came out that were really just nonsense. However, Albemarle’s JV with Sichuan Tianqi Lithium Industries, “Tianqi,” controlling Talison Lithium’s main spodumene asset, has emerged as the, ‘Evil Empire’ in China. Spodumene is the most common, ‘hard rock’ or mined lithium mineral used to produce lithium concentrate to be further processed into lithium chemicals.

Carbonate prices in China are currently in the RMB 120,000/MT (~ $18 K/MT) range including VAT – double the global average on a VAT adjusted basis. This is not a real ‘benchmark’– there’s not just one price. The market is very volatile right now. It is an incredible ‘run-up’ in a short period although less dramatic than the rare earths run a few years ago.

I expect (hope) prices in China will moderate to a band in the RMB 80,000 to RMB 100,000 range (~ $12 K to $15 K) as the current panic settles down. Lower pricing will depend in large part on spodumene supply from Galaxy and Neometals Ltd. as well as Orocobre Ltd.’s carbonate plant getting out of, ‘start-up’ mode. The other key lithium markets of Japan and Korea have seen contracts with the “Big 3” (there’s that term again) rise 15 – 20% in 2016, but contract carbonate prices are still, in most cases, below $7 K/MT for large buyers.

Hydroxide contracts are below $10 K/MT. Pricing for companies importing either carbonate or hydroxide from China will spike into a US$ range close to the equivalent of RMB prices in China. China has a high percentage of global hydroxide capacity, so this is more significant for global hydroxide purchasers than for carbonate purchasers. The lithium market has not seen this level of volatility (in an upward direction) in my 25 years in the business.

Readers find it intellectually comfortable to think of a, “Big-3” in lithium — FMC, SQM, ALB. What are readers missing with that narrative?

The Big-3 is a legacy term that I’m also guilty of using from time to time. For now, Albemarle is the standalone lithium superpower. SQM has a great (lithium as by-product) business, but currently has no capacity or product line expansion plans. FMC is, by my reckoning, #5 in the industry after falling behind two important Chinese producers – Tianqi and Ganfeng in terms of global significance. FMC had a great lithium franchise, but it’s been devalued by loss of corporate commitment and ongoing strategic missteps since 2010.

Interestingly, Albemarle’s status of superpower may be short lived. As of today, Albemarle still has not received an expanded brine permit to operate their 20,000 MT lithium carbonate expansion in Chile. Meanwhile, Tianqi has caused havoc in China’s spodumene converter market and the JV partner’s actions are driving the recent run-up in China pricing as a result. Albemarle is now bullying at least one former Talison spodumene customer into a tolling contract.

Albemarle’s hydroxide plant in North Carolina has failed to meet expectations – under-performing both in terms of volume and quality. Albemarle has terminated many key managers from acquired Rockwood Lithium. Smart people often make foolish decisions and I think we’re seeing many unusual moves and statements coming out of Albemarle lately. On the other hand, given the price trend and strong downstream business, Albemarle’s lithium profits will continue to rise, masking the longer-term implications of poor execution in Chile and King’s Mountain, along with curious management decisions in Baton Rouge.

You have touched upon China’s role in the industry, what else about China is important to know?

China is, by far, the largest lithium market. Two globally important lithium producers have emerged and I expect you will see capital from China invested in more lithium projects outside China. Note the current interest from China in purchasing the 23% stake in SQM that’s coming onto the market.

Can you comment on the role that technology (like POSCO’s, Tenova Bateman’s) for the processing, and/or secondary processing, might have going forward?

Both companies you mention have been talking for a long time. If POSCO is really serious, why are we still waiting for them to announce a significant capital investment or deal with a company like Western Lithium? I’m not a believer in the future of clay-based production. I’m not saying it’s impossible, but I’m saying that I don’t believe there will be commercial production from clay in the next five years. This statement will likely incite the, ‘twitter trolls’ that are hopeful of Sonora, Mexico production but we are all entitled to our own opinion.

Are you able to speak to the industry’s cost curve? Might new entrants shift the curve to the left and possibly make life difficult for marginal players?

Spodumene has become such a significant percentage of global production that it would take multiple low-cost new entrants to change the situation, to make a material shift to the left on the overall production adjusted cost curve. Demand growth now requires a new plant every 12-15 months. Assuming a new plant is 15 K to 20 K MT per year, Albemarle’s expansion should be operating at a reasonable capacity by late 2017.

Hopefully, Orocobre Limited will finally right the ship and produce 12 k to 15 K MT by 2017, but until then, end users should hope that Galaxy’s reopening of Mt Cattlin and Neometals Ltd.’s Mt Marion change the spodumene supply picture in China. Perhaps that would free the converters from the clutches of the, ‘Evil Empire.’ Remember, all lithium is not the same quality and the industry is in a shortage situation as we discuss this.

Thanks to Mr. Lithium for sharing his time and considerable insights. [I have no prior or existing relationship with Joe Lowry or any of his business interests.]