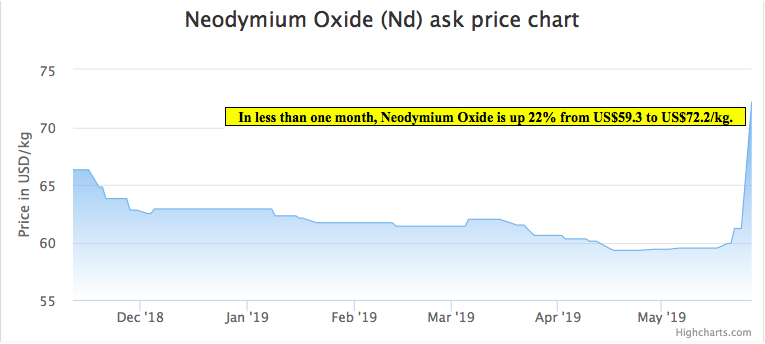

There has been quite a bit of ink spilled lately regarding the Chinese – U.S. stand off and possible implications for Rare Earth Metals. Rick Mills, from Ahead of the Herd, has written the best articles that I’ve read so far. Many Rare Earth Metals companies have seen their share prices increase, some substantially. Yet, we might still be in the early innings of a long, drawn out game. Of course, no one knows how this will end, but select Rare Earth prices have begun to move higher. For instance, Light Rare Earth Element Neodymium oxide (“Nd“) is up > 22% in just the past few weeks. As of Friday May 24, prices of Praseodymium-Neodymium oxide stood at 330,000-340,000 yuan/tonne, up from 264,000 yuan/tonne the week prior, according to SMM. That’s up 26% in a week.

From a Global Times article,

“Why did the U.S. threaten to raise tariffs on essentially all remaining imports from China, while sparing rare earth metals? Without a reliable domestic supply, the U.S. must rely on China to supply industries of high strategic importance. China can raise prices of rare earth metals exported to the U.S. in response to higher tariffs on Chinese products. The U.S. decision to omit rare earths from the China tariff list shows how much the Country depends on these minerals. In the short term, U.S. users would not be able to find alternatives, so they would have to accept higher prices. China has various tools to influence prices, cutting the number of rare-earth mining licenses, raising market access standards for miners and reducing exports of primary rare-earth products.”

In addition to Rare Earths being in the crosshairs, security of supply of Cobalt is also being discussed by industry participants & Government & Trade officials in the U.S. While less critical then the highest value Rare Earth Metals, Cobalt is important, especially for grid-scale Energy Storage Systems. Last week, execs from cobalt companies with projects in the U.S. & Canada met in Washington D.C. to discuss Cobalt’s tortured supply chain. Supply is at grave risk due to ~65% of it coming from a single country in Africa. Politicians talking about Cobalt supply is helpful in framing the Rare Earth Metals situation. Evidence that the trade war is heating up can be seen in higher Rare Earth Metals prices, it’s as simple as that, and we’re seeing higher prices of select metals….

The biggest increases have come from Dysprosium (“Dy”), Nd & Praseodymium (“Pr“), up 56%, 22% & 22%, respectively, from 2019 lows, as of May 27th. These 3 metals just happen to be 3 of the most critical metals for national defense applications, and are widely used in super magnets and other crucial high-tech fields. In many cases there are few, if any, substitutes. Rare Earth Metals juniors are catching a bid, Appia Energy, GéoMégA Resources, Rainbow Rare Earths, Greenland Minerals, Northern Minerals & Peak Resources are up an average of 114% from 52-week lows. NOTE: {2 days later, the top 6 performing REE juniors are up an average of 176% from 52-week lows.}

Interestingly, 3 of the top 6 performers I mentioned are Australian-listed, which most readers (and me) rarely, if ever, invest in. There are not that many North American-listed REE stocks to choose from. And, many of the U.S & Canadian-list names have projects that require hundreds of millions of US$ in Cap-ex. Others, that were exciting in the last REE bull market, have metals that are no longer as highly prized. In 2010-2011, there might have been 6-8 REEs worth owning. Today, only 3-4 Rare Earth Metals are truly bankable for the long-run.

With that in mind, (wait for it, I have a stock idea to discuss) readers should want to invest in companies with LREE deposits, more specifically with deposits containing as much Pr, Nd & Dy as possible. And, companies that have tight share structures so that if they move, the uptick could be very significant. I also want companies with small market caps. Less money is being deployed into natural resource stocks, it’s a lot easier to move a company with a market cap < C$10M than > C$100M. Finally, a strong management team & Board are paramount.

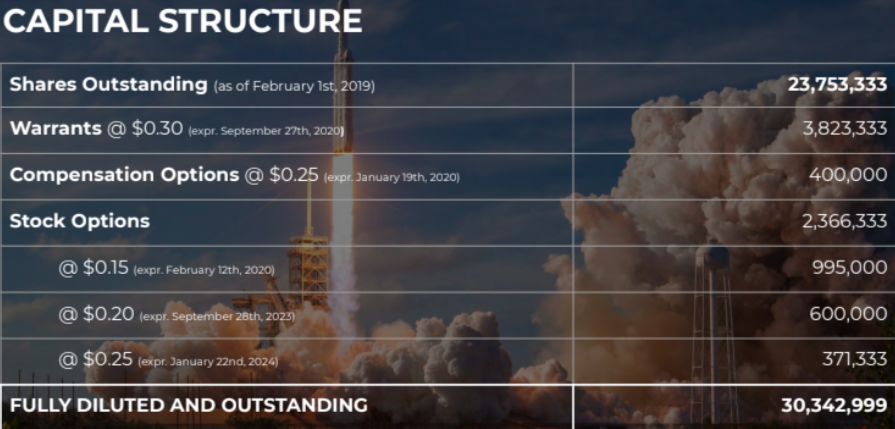

Defense Metals Corp. [TSX-V: DEFN] [OTCQB: DFMTF] has all of the attributes I mentioned and more. Earlier this year, the share price hit C$0.30 on excitement over the uranium spot price climbing above US$29/pound, (the Company has promising Athabasca uranium assets) a great management team and a cheap valuation (only 24 million shares outstanding). Since then, the uranium price has settled to around US$25/pound and Company news flow has been slower than hoped for. SGS Canada is performing a battery of tests and will write a number of important reports, mostly about metallurgy. SGS is working with a 30-tonne bulk sample from Defense Metals’ Wicheeda deposit.

However, the management team, Board & Advisors are as strong as ever, and select Light REE prices are increasing. Increasing prices? That’s strange, Lithium, Cobalt, Vanadium, Gold, Silver, Copper, Zinc, Lead, Uranium — all down over the past month or longer. Marijuana (cannabis) prices are down as well! According to Mr. David Merriman of Roskill, “LREE projects have comparatively greater concentrations of Lanthanum, Cerium, Praseodymium, Neodymium & Samarium, typically forming roughly 75%-99% of contained REEs in a deposit.” Defense Metals has a LREE deposit with all 5 of those metals.

Defense Metals has 2 of just 3 or 4 Rare Earth Metals that are absolutely critical to the global economy, and a few metals that are modestly to moderately important in enabling a growing middle class to continue moving to cities and buying their first smart phones & Electric Vehicles. The concentrations of Nd & Pr might seem low at well under 1%, but those metals trade at about US$70K/t. Compare that to ~US$54K/t for Uranium, ~US$35K/t for Cobalt, ~US$18K/t for Vanadium, ~US$12K/t for Nickel and ~US$6K/t for Copper.

One can’t talk about China and the U.S. without discussing Rare Earth Metals. If one talks about Rare Earth Metals, the ones that come to mind are Nd, Pr & Dy. Earlier this year I asked Mr. Merriman about the dominance of select metals, and of course China,

“China leads in production of both mined rare earth products & refined rare earth compounds, with Chinese production accounting for 86% of global refined production in 2017. Rare earth production outside China is forecast to grow significantly through 2028 as numerous projects in Australia, Russia, the Americas & Africa come online. Demand for rare earth permanent magnets is forecast to show strong growth through 2028, which is expected to further distort rare earth demand ratios with Nd, Pr & Dy forming a greater proportion of total demand.”

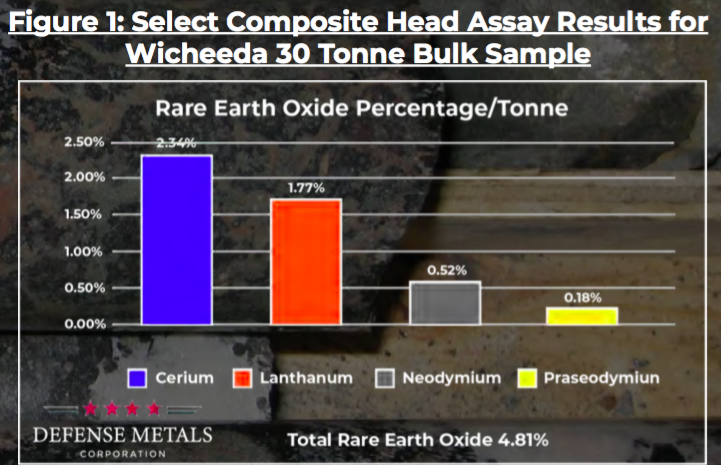

Management expects more news flow in June than in April & May as SGS Canada completes additional metallurgical test work on the 1,780 hectare Wicheeda project bulk sample. The timing could hardly be better. If the Company receives more positive news, a mini-pilot plant will be built to further advance and de-risk a process flow sheet. Select head assay results for the 30-tonne bulk sample included 2.34% Ce oxide, 1.77% La oxide, 0.52% Nd oxide & 0.18% Pr oxide, which the Company considers potentially economically significant. Total LREO (Light Rare Earth Oxide) was 4.81%.

From a recent Company press release,

“The results confirm, in conjunction with previous metallurgical head grades returned from smaller drill core samples, the presence of significant Pr values…. The Company considers the results to have potential economic significance to the advancement of the Wicheeda Property given recent indicative LREE oxide prices and their potential impact on Wicheeda, which has been historically viewed as a cerium-lanthanum-neodymium deposit.”

I look forward to news on this exciting LREE Project. Wicheeda could be in small-scale commercial production relatively quickly, if the metallurgy is as good as management believes it might be. A Project with much smaller upfront Cap-ex than many legacy projects around the world that are still on the drawing board. The reports & data from SGS should convey a tremendous amount of information about the potential feasibility of a mining operation. It’s exciting times for REE & LREE juniors, especially so for Defense Metals Corp. [TSX-V: DEFN] [OTCQB: DFMTF] shareholders.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Defense Metals Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing co-ntained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Defense Metals Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares of Defense Metals Corp. and it was an advertiser on [ER].

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.