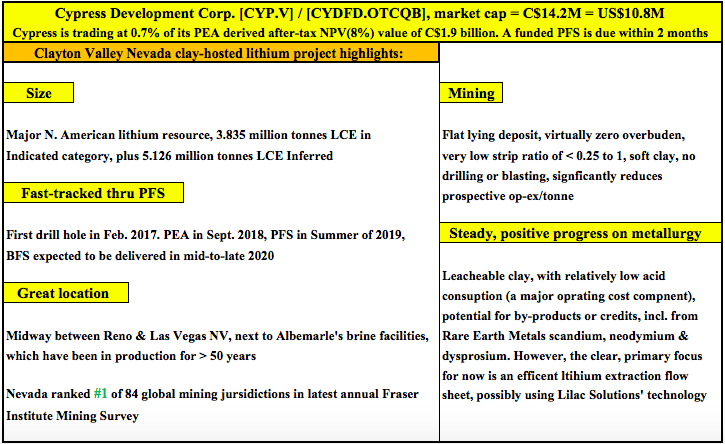

Earlier this year, Cypress Development Corp. (CYP.V) / (CYDVF.OTCQB) delivered a Preliminary Economic Assessment (“PEA“) on its 100% held Clayton Valley clay-hosted lithium project in Nevada (USA). The results were strong, (all figures post-tax, in CAD$), an IRR of 32.7%, NPV(8%) = $1.95 billion, upfront cap-ex = $645.88 million, a 40-yr. mine life, operating at 24K tonnes lithium carbonate equiv. (“LCE“)/yr.

A fully-funded Pre-Feasibility Study (“PFS“) is expected in 2H August or 1H September. After the release of this important report, management will be in a position to dive deeper into talks with a number of strategic and/or financial partners that have already expressed interest. {see new corporate presentation}

The next capital raise (or if an investment at the project level it would not require the issuance of new shares), will fund a pilot plant & Bank Feasibility Study (“BFS“). The BFS is expected to be delivered in mid-to-late 2020.

Cypress partners with lithium extraction technology company

On July 15th, Cypress and privately-owned Lilac Solutions announced a successful demonstration of favorable lithium recoveries from Cypress’ Clayton Valley project in Nevada.

Lilac is a lithium extraction technology company based in California. Cypress’ project is a large, clay-hosted lithium deposit containing 3.835 million tonnes LCE in the NI 43-101 Indicated resource category, plus 5.126 million tonnes LCE in the Inferred category. {see NI 43-101 Technical Report (PEA)}.

Cypress has developed an innovative leaching process which reduces the quantity of sulfuric acid needed (a major cost factor) to leach lithium from clay. After lithium is leached into solution (“leachate”), Lilac has proven it can extract it to produce a high-purity lithium solution, which can be processed with conventional equipment into high-purity lithium carbonate & hydroxide.

According to the news release, Lilac successfully extracted lithium from clay leachate, recovering 83% of the lithium, and rejecting greater than 99% of the sodium, potassium and magnesium impurities. Importantly, the remaining lithium in leachate can be recycled to allow for further recovery of lithium. The amount of additional lithium potentially recoverable in this manner is unknown at this time.

Cypress CEO Bill Willoughby, Phd commented,

“Lilac’s results are promising and offer another path forward to efficiently recover lithium from our process solutions. Our project is a significant potential source of domestic lithium and we are pleased to be working with Lilac in applying their ion-exchange technology.”

Several clay-hosted Li projects coming online in early 2020’s

Readers should be aware that due to technical challenges associated with lithium extraction and/or prohibitive operating costs, no clay-hosted lithium project has reached commercial production. That’s very likely to change as Ioneer Resources’ Rhyolite Ridge and Bacanora Lithium’s Sonora projects commence operations in the next few years.

Those two will likely be followed by Lithium Americas’ Thacker Pass project (Ioneer, Lithium Americas & Cypress Development each have projects in Nevada. Baconora’s flagship clay-hosted lithium project is in Mexico). Ioneer’s project will get roughly half its revenue from the sale of boric acid.

If things continue to go well for Cypress, and management is able to line up one or more strategic partners to help fund development, the Clayton Valley project could reach commercial production a few years after Ioneer & Baconora. Perhaps around the same time, or a year behind, Thacker Pass.

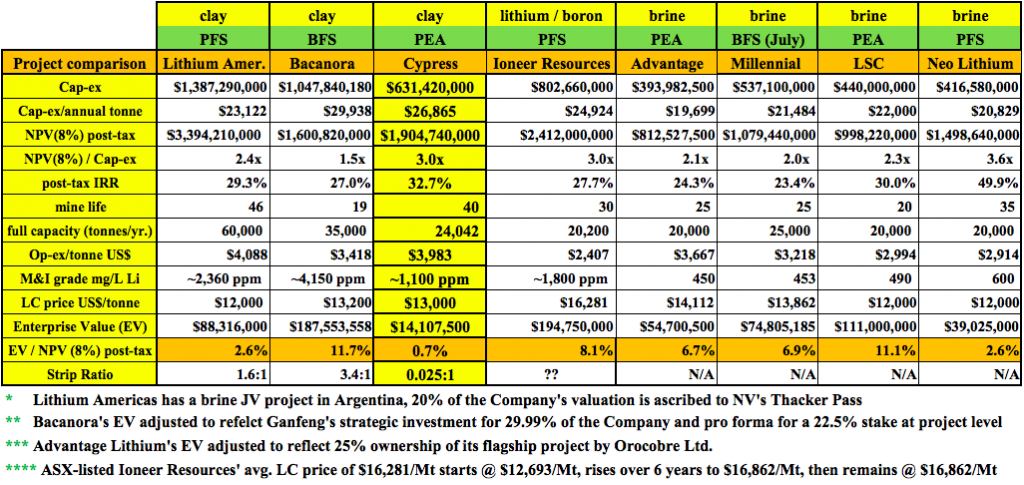

I argue that while behind the others, Cypress is in the same league, especially once it delivers a PFS. Therefore, as a percentage of independently derived, after-tax NPV, it should trade in the same ballpark. However, that is not the case. Cypress is trading at less than 1% of its NPV, while peers trade at between 2.6% and 11.7%, {see chart below}

Even if one assumes that Cypress is facing more equity dilution than peers, it is trading at a significant discount. For example, consider a hypothetical doubling in Cypress’ share count to adjust for its earlier stage. The valuation would then be 1.5% of NPV. That’s still a 79% discount to the average of the other names in the chart, 7.1% of NPV.

Next steps after a PFS this summer, a pilot plant & BFS

Following behind much larger companies has its advantages. Management at Cypress, most notably CEO Bill Willoughby, who’s a Phd Mining Engineer with nearly 40 years’ experience, is learning a great deal from technical press releases & reports filed by Ioneer, Bacanora & Lithium Americas. Management is learning what to do, but also what not to do.

The same learning process will continue as Cypress and Lithium Americas go through through their respective pilot plant stages. Ioneer & Bacanora already have pilot plants operating. However, each project is unique. Bacanora & Lithium Americas each have projects that are far different from Cypress’ Clayton Valley, and different from each other’s.

Global lithium supply next decade highly uncertain

One of the more exciting things for investors is something that has nothing to do with Cypress. It’s the happenings, or lack of happenings, in Chile & Argentina, where project after project has been delayed or is outright stalled. Not just early-stage projects, but projects at the BFS stage. Stalled over the past year or more due to a falling lithium price and inability to arrange financing.

This is generating negative investment sentiment & headlines, but in the medium-to-longer-term, it’s great news for lithium pricing. Three years into a lithium price boom, albeit one that has tapered off lately, and production from Chilean brine operations has barely budged. There are about a dozen brine projects in Argentina, from pre-drilling to BFS-stage to fully-funded, that simply are not moving forward.

I believe that the world might only get half to two thirds of the brine production expected out of Chile & Argentina by mid next decade. Said another way, if 500,000 tonnes LCE is expected from those countries in 2026, I would not be surprised if we did not see that amount until 2029.

No new brine projects have been able to ramp up to nameplate capacity, and time periods to reach just 70%-80% of full capacity are stretching out to 4 or 5 years instead of 2 or 3. Orocobre is an example of this

Conclusion

By the time Cypress gets its Clayton Valley project up and running in the middle of next decade, I think the lithium pricing environment is going to be strong, perhaps very strong. By strong I mean US$12K-$16k/tonne. Very strong would be US$16k-$20k/tonne. The current price is around US$11,000/tonne. Cypress is an earlier-stage investment opportunity than some of their peers, but should be squarely in the middle of the bunch once they have tabled a PFS later this summer.

If true, Cypress Development Corp. (CYP.V) / (CYDVF.OTCQB), and a select few other clay-hosted lithium companies, should be in a prime position to enter the market at an ideal time. And, Nevada will be a great location from which to launch the sale of high-purity lithium products to global auto manufacturing plants across North America.

Readers can learn more about Cypress by reviewing the company’s new corporate presentation and latest press releases.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Cypress Development, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Cypress Development are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned shares in Cypress Development Corp. and the Company was an advertiser on [ER].

Readers should consider me biased in my view of the Company. Readers understand and agree that they must conduct their own due diligence above and beyond reading this interview. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this interview or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.