On August 29th Cypress Development Corp. (TSX-V: CYP) / (OTCQB: CYDVF) announced the successful completion of slurry rheology & filtration studies that are an integral part of the Pre-Feasibility Study (“PFS“) for the Clayton Valley clay-hosted lithium project, located immediately adjacent to Albemarle Corp.’s Silver Peak brine processing facilities in Nevada.

Management believes its U.S. location will become an increasingly valuable attribute. While many junior lithium companies like to name drop “Albemarle” and “Silver Peak,” Cypress owns 100% of one of just a few projects in Nevada that Albemarle might actually be interested in.

More promising results from Cypress’ expert technical team

Back to the latest news…. the outcome was the result of months of testing by laboratories and a detailed review with consultants & equipment vendors. This news represents a major milestone in the project because the results simplify the process flow sheet.

Cypress CEO Bill Willoughby commented in the press release,

“A critical step for us at Clayton Valley is the separation of solids & liquids. A viable process is dependent upon the ability to separate the process leach solution (PLS) from the leached residue whether by thickeners, filters, or other means. Significant test work has allowed Cypress to identify a commercially viable process, based on filtration, to take the solid-liquid separation from the laboratory benchtop to the operational scale.”

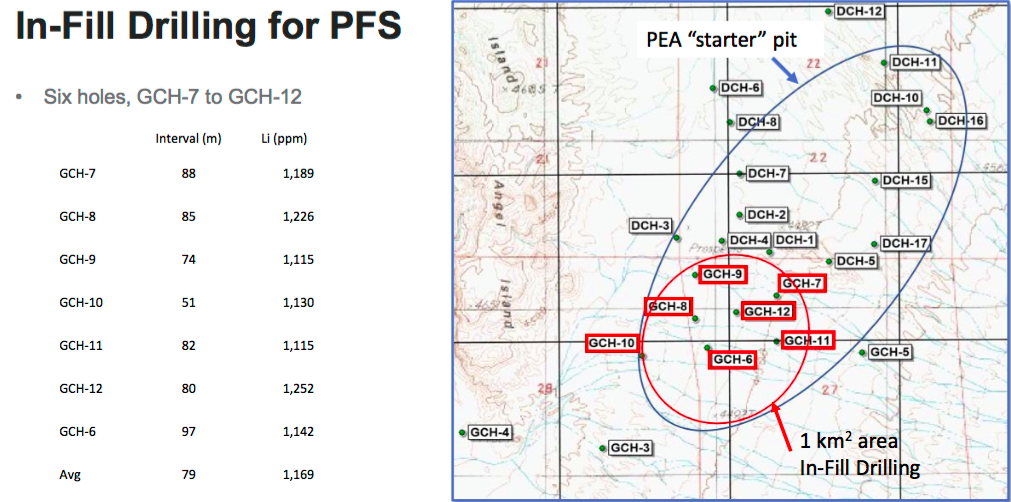

Readers may recall that Cypress released positive results from the first & second phases of its PFS metallurgical program in February & July. Since then, work has continued on other aspects of the PFS, including recovery & concentration of lithium from solution through mechanical evaporation, membrane filtration, and ion-exchange processes.

CEO Willoughby continued,

“The Cypress technical team discovered the Clayton Valley clays behave differently at varying leach conditions. By looking at the electro-kinetic potential of the clays we can select the optimal reagents & equipment. We also know under what conditions the rheology of the slurries becomes a limitation, and can design the flow sheet accordingly. With this new knowledge, we are confident we can simplify a significant portion of the leaching flow sheet.“

Cypress is looking at additional steps to simplify plant design with the goal to further streamline the production process and lower costs. With metallurgical & materials handling studies completed, Cypress expects to publish a PFS during the fourth quarter.

Next major milestone is a PFS in 4th quarter

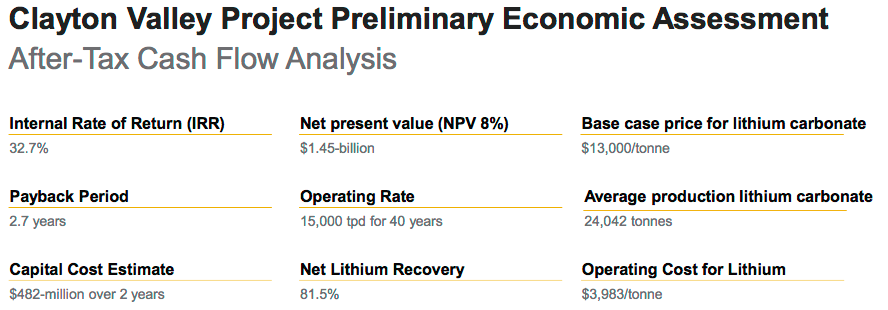

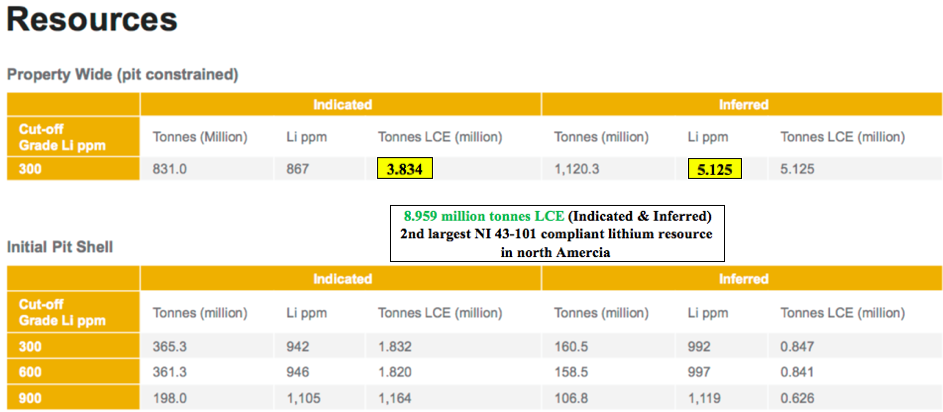

It appears the PFS has been pushed back a few months. After a recent capital raise the company is comfortably funded through delivery of a PFS later this year. Come to think of it, what’s the rush? Investor sentiment remains very weak for lithium, cobalt, vanadium & graphite juniors. As long as Cypress is funded, let them keep carrying out studies to improve the PFS! Below are some highlights from the PEA.

It’s important at this point to reiterate the considerable strength of management, the Board, technical advisers & retained consultants. All of these impressive people and groups are being effectively led by CEO Willoughby, who has a Doctorate in Mining Engineering & Metallurgy from the Univ. of Idaho.

Who on earth could possibly be better to run this show than a PhD in engineering & metallurgy!?! He knows what he’s doing, and he’s a driving force behind the very good results and progress his technical team is delivering.

I asked Dr. Willoughby about last week’s news, he said,

“It’s a major technical problem to separate ultrafine clays particles < 5 microns from a leach solution. Our solution could put us in the forefront of clay-hosted lithium projects globally.”

Demand keeps increasing, supply increasingly uncertain

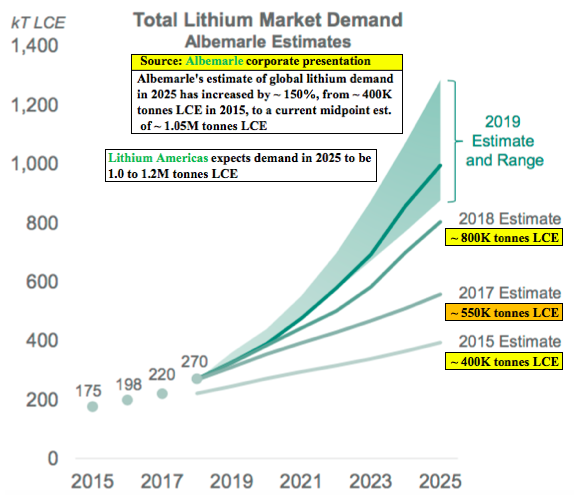

There’s a massive disconnect in the lithium world. For years, demand forecasts have been going up. The demand side of the equation — driven by both energy storage & the electrification of passenger & commercial vehicles — is likely to increase at a Compound Annual Growth Rate (“CAGR“) of at least 15%, perhaps 20% or more. For example, at a 20% CAGR from Albemarle’s 270K tonne figure in 2018, demand would reach 967K tonnes in 2025.

Albemarle Corp. has a particularly good graphic depicting this unmistakable trend. Four years ago they expected ~400K tonnes LCE demand in 2025. Now, Albemarle is forecasting demand of about 1 million tonnes in 2025. Likewise, Lithium Americas is forecasting between 1.0 to 1.2 million tonnes LCE demand in 2025, a range it says comes from industry producers & publicly reported forecasts.

Finally, Fastmarkets expects LCE demand to grow from ~300K tonnes in 2019 to “at least” 1.1 million tonnes in 2025. So, a lot of forecasts in and around the one million tonne mark, but even if it turns out to be less, I think it will be a major challenge for supply to approach that level in the next six years.

The longer the project delays in Argentina / Chile brine projects, and the more project mishaps like at Nemaska, the more room there is for unconventional projects such as Cypress Development’s Clayton Valley. The market will take every battery-grade tonne of lithium chemicals produced by any company that can supply them. Lithium juniors who can make it across the production finish line will be richly rewarded.

Despite significant fiscal & political challenges in Argentina that could further delay brine projects there, and continued slow movement in project development & production expansions in Chile, unconventional projects are still meaningfully undervalued compared to brine projects.

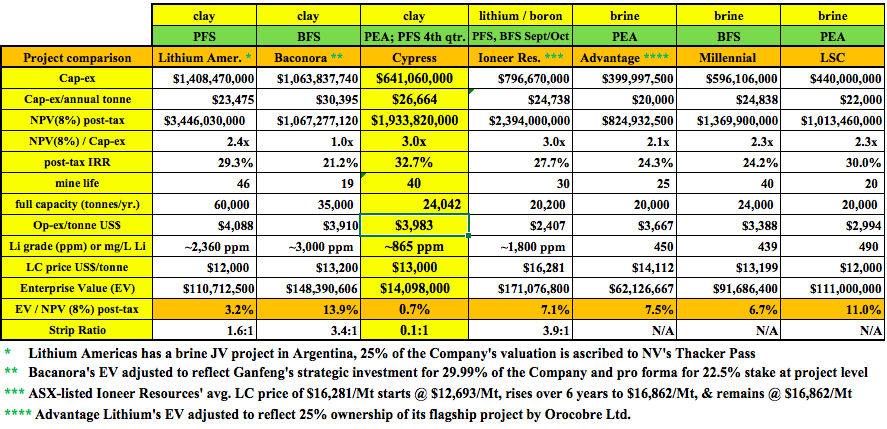

For example, Cypress Development Corp.’s enterprise value (“EV“) is less than 1% of the after-tax NPV found in its PEA. Compare that to the average 8.2% EV/NPV on the chart above. Cypress’ EV/cap-ex ratio of 3.0 times (3.0x) is 40% better than the 2.1x average of the other unconventional projects.

Cypress has the highest after-tax IRR on the chart at 32.7%, compared to an average of 26.1% among the others. And, the company’s cap-ex at C$641 million is 21% lower than the peer average.

Finally, readers should note that the Clayton Valley project has a strip ratio of 0.1 to 1. The other three projects with strip ratios average 3.0 to 1. Cypress has 1/30th the strip ratio of its unconventional peers!

That’s a big reason why the company has attractive op-ex & cap-ex, despite having lower grade Li to work with. Another reason is the mineralogy; the Clayton Valley project’s lithium abundance is hosted in a more friendly clay than that at some of the other projects. More friendly meaning easier and less costly to liberate the lithium into solution.

The extreme weakness in the vast majority of lithium juniors is actually great news. Great news for any lithium company hopeful that can produce lithium next decade. Great news for investors who may want to average down in their favorite battery metals names.

Brine projects have gone from, “can’t go wrong,” to “can’t fund”

A funny thing happened over the past two years. Brine projects went from no-brainers; (lowest cost, best understood, most reliable) — to the exact opposite. Solar evaporation ponds are getting less and less popular by the week, day, hour! And, unusually rainy weather in the Puna region of Argentina has negatively impacted pond yields. Speaking of Argentina….. well just read the headlines, it’s not pretty.

Chile imposed an onerous sliding-scale royalty on realized lithium prices from production in the Atacama salar. Albemarle’s & SQM’s best, lowest cost lithium brine operations…. the world’s best, may no longer the world’s lowest cost.

Brine projects were sure things and clay-hosted lithium projects were, “maybe in 10 years.” Now? Most brine projects are dead in the water, some of them never coming back to life. Even the top-quartile, most advanced projects are not getting funded. By contrast, the prospects for clay-hosted lithium projects are better than they were two years ago, albeit also difficult to fund.

Investors would be crazy not to consider unconventional assets. Brine projects, with evaporation ponds attached, will themselves be unconventional at some point in the future. The only question is when.

In early August, Glencore announced it was shutting a major cobalt / copper mine in Africa at the end of the year. Three weeks later, cobalt prices are up 30-35%. It might not take that much to get lithium prices back on an upswing. If prices were to improve, juniors like Cypress Development Corp., trading at under 1% of third-party derived after-tax NPVs, could do quite well.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Cypress Development Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker / dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Cypress Development Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this interview was posted, Peter Epstein owned shares of Cypress Development Corp., and the Company was an advertiser on [ER].

While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any future events & news, or write about any particular company, sector or topic. [ER] is not an expert in any company, sector or investment topic.