Last month, Drone Delivery Canada [“DDC”] (TSX.V:FLT, OTCQX: TAKOF), announced the completion of a high-tech Commercial Operations Center (“COC“) in Vaughan, Ontario. This was an important milestone. At full capacity, this state-of-the-art facility will be able to manage up to 1,500 drones in flight at once. Last week, analysts and local news reporters toured the facility.

Brand new Commercial Operations Center

With the COC complete, and in partnership with Air Canada’s (“AC“) [AC.T] ($12.4 b market cap, $5.9 b in cash) Air Canada Cargo (“ACC“), DDC said it would announce multiple customers in coming months as it rolls out its logistics service. That’s exactly what DDC has done, with two new customers so far, and a robust sales pipeline.

As a reminder, DDC entered into an agreement whereby ACC will market & sell DDC’s drone delivery services using ACC’s marketing & sales platforms. That was perhaps the biggest news in the Company’s six-year history.

On October 23rd, DDC announced the Canadian arm [DSV Air & Sea Inc. Canada] of global transport & logistics company DSV Panalpina as its second commercial customer. DSV has ambitions to utilize 20 or more routes by the end of 2020.

DDC wins Major new logistics / freight forwarding customer

This is big news, important news, as it gives the clearest picture yet of what a large customer could potentially mean. Earlier this year, management estimated that each drone delivery route could, on average, generate $10,000 per drone, per route, per month.

Therefore, if 20 routes were taken up by DSV, that could amount to $2.4 million in annual revenue. Now, for all I know, that’s an absolute best-case scenario, but at least it gives investors an approximation of how things could play out. Imagine the positive impact on business fundamentals from the awarding of additional customer mandates in coming months.

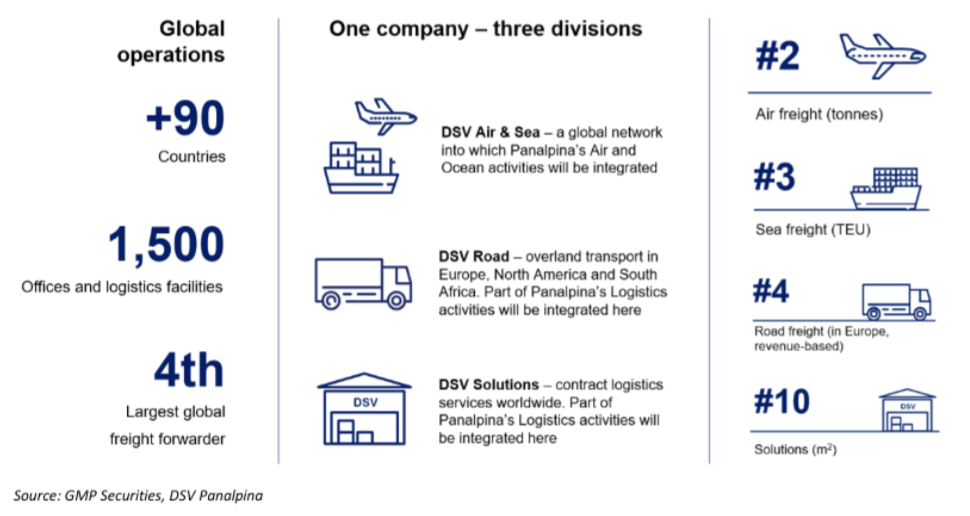

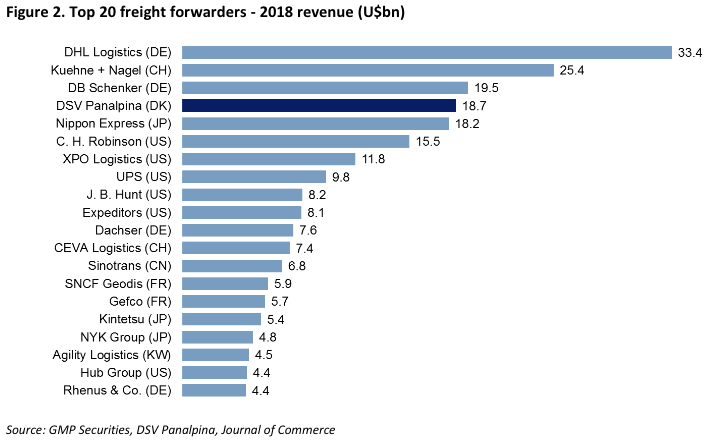

Six weeks ago when management announced its first customer, I feared it might take dozens of customers like Vision Profile Extrusions to generate meaningful revenue. DSV, on the other hand, is a top 10 global logistics (freight forwarder) company based in Denmark with over $20 billion in sales.

DSV’s Canadian segment sales are far less than $20 billion, but I imagine that DSV is looking (over time) to deploy drone logistics / delivery across its entire suite of operations. Furthermore, what better way to showcase DDC’s growing capabilities than with a giant logistics / freight / transportation company! And, DSV’s new Canadian warehouse, at over 1 million sq. ft., where DDC will operate from, is the largest in DSV’s global network.

DDC could grow 3x faster than top cannabis licensed producers…

Perhaps more important than DSV’s large sales figure is the fact that DSV has shown consistently positive earnings, albeit at an EBITDA margin in the mid-to-high single digits. This observation is key to DDC’s value proposition.

One hundred percent of each dollar saved by DSV from drone deliveries will fall to its bottom line. Drones might be the single best margin capture opportunity of the 2020s for logistics companies like DSV, and for a wide range of retailers, as well as other commercial users, and cost savings for government & military customers.

In disruptive, paradigm-shifting sectors — like drone delivery / logistics or, “the internet of things,” or electric vehicles (EVs), or cannabis / hemp — competition, pricing, costs (margins) and growth rates typically move against participating companies. Think about it; hundreds of new EV models promises to wreak havoc on carmakers.

Cannabis prices rarely move higher, over time they decline as growing methods and ever more experienced growers produce higher quality product. Combined, there are over 350 cannabis / hemp and related companies listed in the U.S. & Canada. North America would do just fine with far fewer players.

By contrast, Drone Delivery Canada could potentially enjoy margins that increase over time. I’m not talking about margin expansion from economies of scale — all companies benefit from that — I’m talking about DDC’s operating costs diminishing due to technology advancements in drone hardware.

Each and every year drones get lighter, stronger, faster, fly longer distances and cheaper to buy / lease and operate. The cost of using drones is declining, with no end in sight. Could that mean several percentage points of margin expansion per year? Perhaps. However, even if I’m wrong, DDC expects to have strong margins before consideration of technological improvements.

I mentioned there are > 350 cannabis / hemp companies. By contrast, DDC has very few, if any, direct competitors in the drone delivery software logistics space. Even fewer publicly-traded competitors. DDC is trading at ~14x next year’s analyst consensus revenue of $8.9 million.

Since there are so few direct peers to stack up against DDC, I will compare it to cannabis licensed producers. The average EV/2020 revenue multiple of the top four Canadian cannabis licensed producers (Canopy Growth, Aurora Cannabis, Tilray and Cronos Group) is ~13x, a bit lower than that of DDC at ~14x.

However, if investors look further out than just a year, the estimates tell an entirely different story. Analysts envision DDC having BOTH more rapid revenue growth, AND a much higher EBITDA margin. Consider this, the four cannabis companies mentioned above have an average EBITDA margin expectation of ~22.5% in 2022. That’s less than half the forecasted EBITDA margin of ~50% for DDC that year.

DDC trading at roughly 2x 2022 analyst forecasted revenue

On average, analysts forecast DDC’s annual revenue could increase from an estimated $8.9 million in 2020, to $57.2 million in 2022 (+ 543%). That would be a two-year Compound Annual Growth Rate (“CAGR“) of 154%. The four cannabis companies are expected to grow (on average) at a two-yr. CAGR of 49%.

Therefore, DDC has the potential to grow three times as fast, while ending up with more than twice the EBITDA margin in 2022. DDC is trading at ~2x analyst forecasted 2022 revenue. In a new research note, GMP Securities estimated 2020 revenue at nearly $13 million and reiterated a $4 price target. The share price is currently at $0.80.

Further, from potentially generating $57.2 million of revenue in 2022, the sky’s (still) the limit after that as DDC has given glimpses of possible revenue reaching into the hundreds of millions by the middle of next decade.

Readers may recall that two revenue streams have been outlined so far; remote northern Canadian communities & commercial business like DSV & Vision Profile. Each segment could contribute hundreds of millions in annual revenue within five years.

Readers may recall that multiple global revenue streams have been outlined so far; oil & gas, mining, medical, pharma, shore-to-ship logistics, ecommerce, last-mile courier, remote communities & commercial business. DDC also expects to license its system globally. And, given DDC’s patented FLYTE system is airframe agnostic, more drones with even greater capacities are likely on the company’s horizon, all adding further revenue and profit potential.

A risk to the DDC story is that revenue ramps up slower than expected. However, CEO Michael Zahra believes that the company could reach cash flow breakeven by the end of next year. Therefore, DDC’s cash balance of $17.5M as of June 30th (just $0.7M of debt) should go a long way, if not all the way, towards bridging the gap to positive free cash flow in 2021.

Conclusion

Modest to no equity dilution ahead, strong, sustainable EBITDA margins, rapid revenue growth, potential for expanding margins and a low cap-ex business model. An investment in Drone Delivery Canada [“DDC”] (TSX.V:FLT, OTCQX: TAKOF) should have relatively low correlation to broader markets. This is a company with dozens and dozens of prospective acquirers.

The company has positive catalysts as far as the eye can see… Additional customer wins, first commercial revenues, entry into new segments. As word of mouth spreads about the substantial benefits of drone delivery — [cost, speed, green (less polluting than trucks), reliable] — everyone will want it, which can only be good news for DDC.

Disclosures / disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Drone Delivery Canada, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Drone Delivery Canada are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned stock options in Drone Delivery Canada, and the Company was an advertiser on [ER].

While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover any specific events or news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.