Gold recently blasted through $2,000/oz. The spot price traded as high as $2,073/oz. on August 6th, ~$150/oz. above its 2011 all-time (nominal) high. Precious metals juniors have responded with big moves. Make no mistake, I realize that the gold price could move lower after such a robust run.

Modest, healthy pullback of 10% in gold price….

In fact it pulled back to ~$1,864/oz. on August 11th, down 10% from its high. Spot is now sitting at ~$1,946/oz. Still, I believe gold (and silver) will remain strong through the first quarter of next year due to U.S. presidential politics and ongoing uncertainties surrounding COVID-19.

I also believe M&A activity will continue to grow. As Major & mid-tier producers become more active, earlier-stage juniors will follow. I suspect we will see bidding wars on the best small companies, like Zijin Mining’s recent acquisition of Guyana Goldfields.

There’s also the fact that metals / mining is not well represented across investor classes. As investors expand their horizons to include metals / mining stocks, especially precious metal juniors — we could see a tsunami of investment capital flowing into the sector.

Portofino Resources has two promising gold projects in Ontario

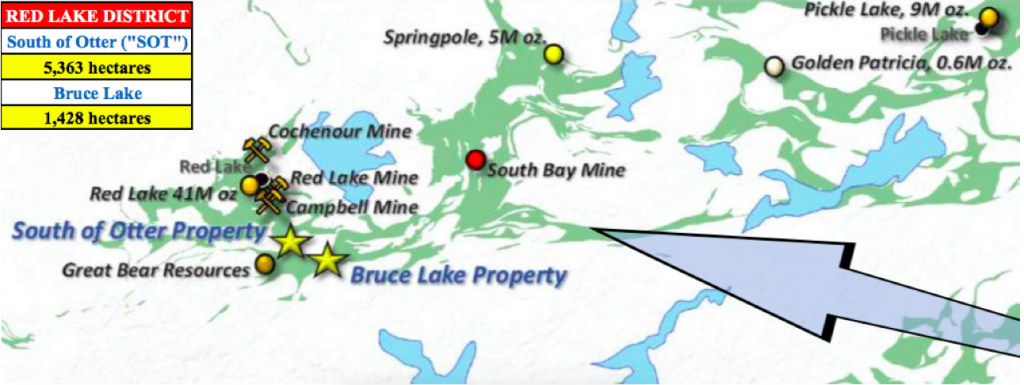

A company I’ve followed for years finds itself in the right place at the right time, yet has a market cap of just C$10.3M = US$7.8M (morning of 8/12/20, C$0.19/shr.). It has two properties in the world famous Red Lake mining district and three in the nearby, up-and-coming Atikokan camp.

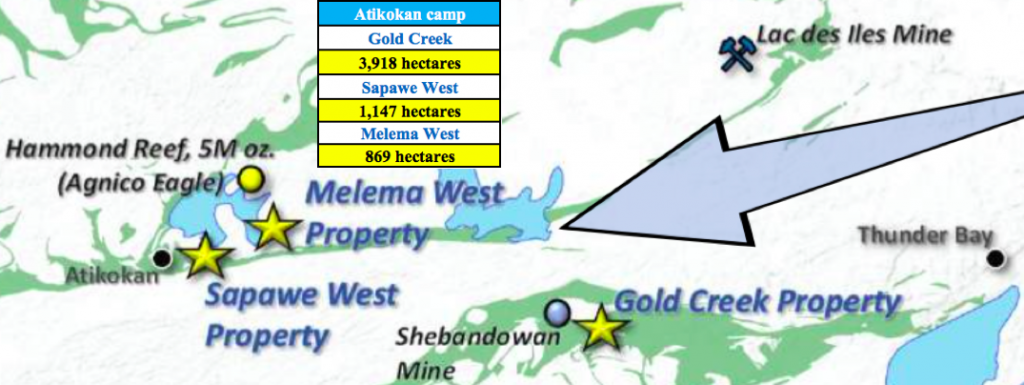

In Red Lake, Portofino Resources (TSX-V: POR) / (OTCQB: PFFOF) / (GERMANY: POTA) has the South of Otter (“SOT“) & Bruce Lake properties. In Atikokan, Portofino has three more, Gold Creek, Sapawe West & Melema West. All five properties, covering 12,725 hectares, are in northwestern Ontario. They’re controlled by low cost, multi-yr. options to acquire 100% interests.

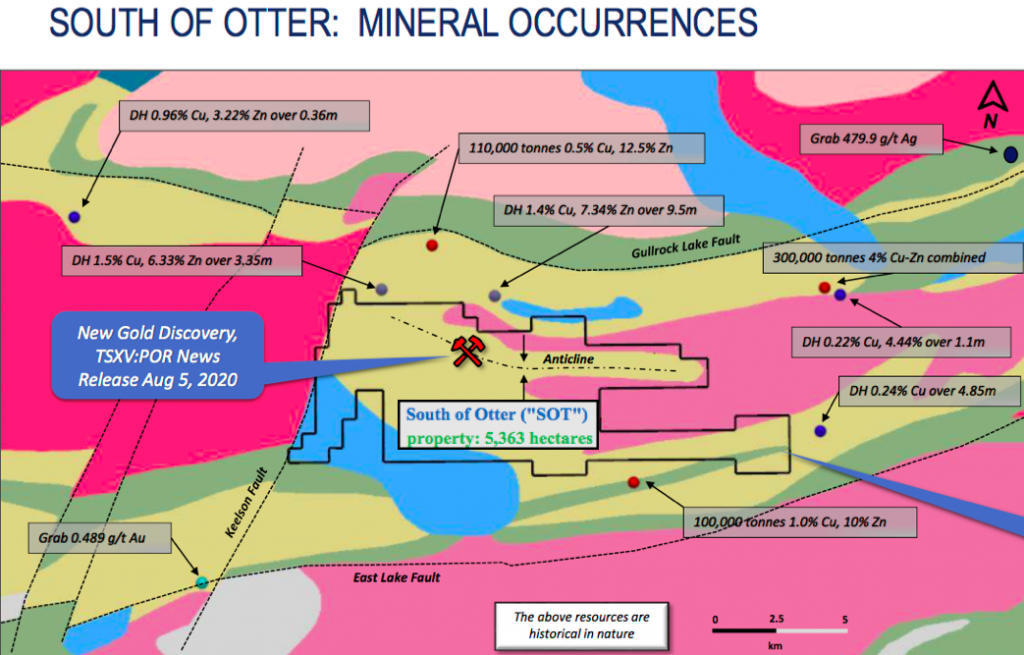

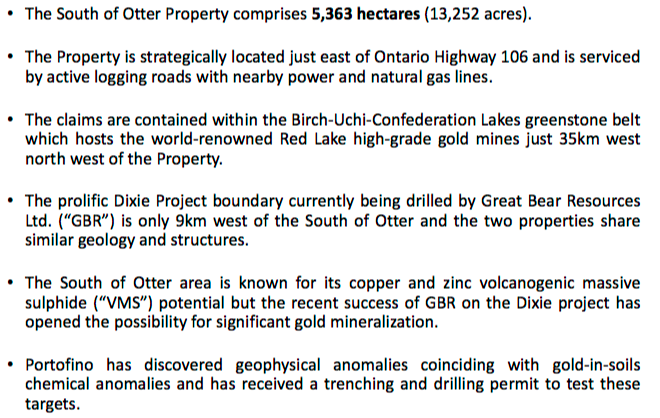

The 5,363-hectare SOT project is ~40 km southeast of Red Lake and ~9 km east of Great Bear Resources’ (“GBR“) very high-grade Dixie project. Importantly, the two projects share similar geology & structures.

Historically, SOT has been the subject of large-scale geophysical surveys targeting base metals. However, in 2001 Goldcorp completed a property-wide compilation & interpretation of prior data to assess the potential for gold.

Historical exploration indicates that significant mineralization extends across a 1.6-km long fault zone ~500 m south of previously identified gold soil anomalies & EM conductors. Twelve grab samples were collected along this (deformation) zone to test for gold, silver, copper & zinc.

New discovery at South of Otter, 18.0 & 8.2 g/t gold grab samples

Results from the 12 samples are in. Portofino hit pay dirt! Management is excited about this new discovery. Two samples returned 18.0 & 8.2 g/t gold, respectively. The Company is currently conducting a trenching program to determine potential strike length & mineralized widths.

CEO, David Tafel commented,

“This new discovery is extremely exciting news for Portofino. The new gold showings are approx. 400 metres south of Goldcorp Inc.’s 2001 gold in soil anomalies. Due to overburden and lack of outcrop, limited work has been completed in this area. We have mobilized a crew to follow-up on this noteworthy discovery.”

Portofino has obtained an exploration permit for SOT. As part of the permit process, management consulted with, and received support from, all local indigenous groups. The permit is valid for three years and allows trenching, diamond drilling & line cutting.

The crew is exploring the area to determine the extent of mineralization, and will determine the steps required to deliver a drill program later this year.

Less of a focus, but still attractive is the Bruce Lake property. From the new corporate presentation,

“The Bruce Lake Property contains gold-in-soil anomalies discovered as part of a reconnaissance soil sampling program completed by Laurentian Goldfields. Portofino has recognized the existence of regional magnetic high anomalies coincident with the gold-in-soils anomalies that it believes are significant. Gold associated with banded iron formations are excellent exploration targets especially when the property has gold in soils associated with a magnetic anomaly.”

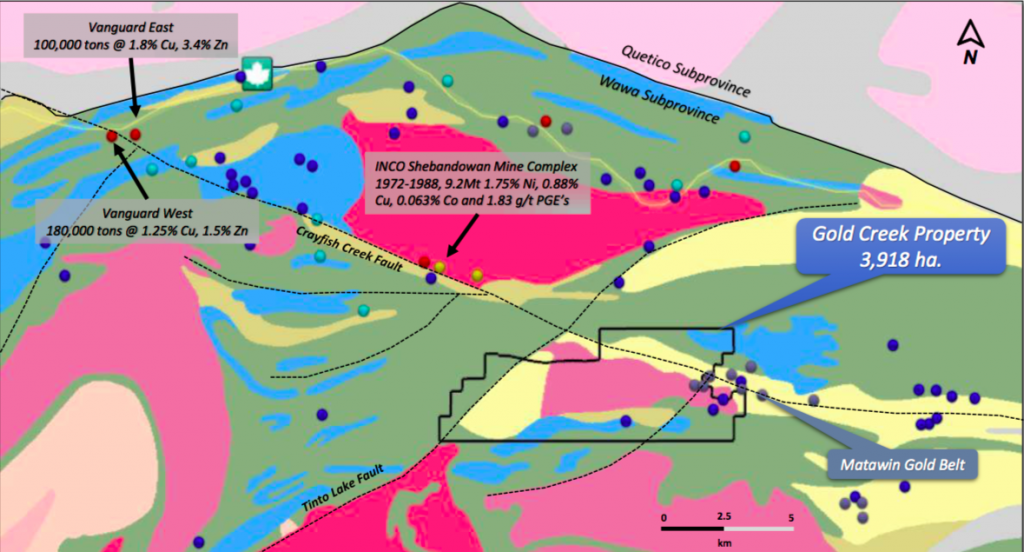

After SOT, Gold Creek could be a second company-maker

Management recently staked seven claims, nearly quadrupling the size of its Gold Creek property from 1,024 hectares (“ha“) to 3,918 ha. The new claims cover structural features that management believes are extensions of known gold-bearing horizons, and also cover part of the Tinto Lake Fault. Gold Creek hosts zones of significant high-grade gold mineralization.

The regional geology is comparable to world-class districts such as the Timmins & Kirkland Lake Camps in northeastern Ontario. Significant gold mineralization has been traced along a 1.5 km strike length.

Grab samples have returned values up to 759 g/t gold (Ontario Geological Survey (“OGS“) property visit). OGS reported another grab sample of 46.6 g/t. Diamond drilling in 2008 assayed up to 2.3 g/t gold over 8.3m (incl. visible gold). Other contiguous zones hosted grab samples of 86 g/t & 43 g/t gold.

Portofino commenced ground prospecting, mapping & sampling at Gold Creek on July 13th. Several occurrences, both historical and possibly new zones of mineralization, were examined & sampled. Samples have been submitted to the lab, results are expected this month.

CEO David Tafel commented,

“We are very pleased to have been able to expand our Gold Creek land package. The historical high-grade gold values, geological analogy to some of the more prominent gold camps in Northeastern Ontario and limited prior exploration equate to a high potential, value creating project. We look forward to receiving & reporting the sample results from our initial exploration program.”

Two nearby historical resources, < 2 km north & < 5 km south of the project, reported grades of 0.5%-1.0% Cu + 10.0%-12.5% Zn, about 5 g/t gold equivalent. Less than 5 km west is the past-producing INCO Shebandowan complex that mined 9.2M tonnes of high-value rock from 1972-1988.

Grades were reported to be 1.75% nickel, 0.88% copper + some cobalt & PGEs. The gold equivalent grade from the nickel & copper alone is 4.8 g/t.

Pipeline of properties also includes Melema West & Sapawe West

In June, Portofino announced the execution of a binding agreement to acquire six claims (869 ha) in the Atikokan district, also in northwestern Ontario. The Melema West property is ~5 km north of the Quetico Fault. Agnico Eagle Mines’s Hammond Reef gold deposit is ~19 km to the northwest. It hosts a large Measured & Indicated resource of > 4.5 million ounces gold.

Grab samples last year assayed up to 10 g/t gold. The vein-system is 1 to 15 m wide and was mapped over a strike length of 170 m. Positive gold values suggest an additional gold-bearing structure potentially exists at Melema West. Recent land acquisitions by Agnico contiguous to Melema West support the idea that Portofino is on the right track.

In May, Portofino executed a binding agreement to acquire three claims totaling 1,147 hectares. The Sapawe West property is ~9 km northeast of Atikokan, just north of the Quetico Fault, and 2.5 km west along strike of the past producing Sapawe Gold mine. Portofino has initiated the compilation & reinterpretation of all available historic data on the property and is proceeding to develop exploration targets for a summer field program.

Conclusion

With M&A on the rise, a potential takeout of Great Bear, Pure Gold or Premier Gold would generate even more excitement in the Red Lake / Atikokan areas. In addition to Agnico, Australia-listed, C$10B Evolution Mining and Canada’s C$8B Yamana Gold are active in the region and could comfortably afford to expand via acquisitions.

This would shine a bright light on the roughly dozen remaining juniors that have all, or substantially all, of their precious metals properties in northwestern Ontario. To recap, Portofino has two very promising properties South of Otter (with a new grab sample discovery) and Gold Creek.

Both could be company makers. Yet, the Company’s market cap of C$10.3M = US$7.8M seems awfully low compared to GBR with a market cap of > C$700M. GBR’s Dixie is obviously far more advanced than Portofino’s SOT & Gold Creek, but it’s still pre-maiden resource.

In a raging bull market, $10M companies that make meaningful discoveries can become $100M companies. Portofino Resources (TSX-V: POR) / (OTCQB: PFFOF) / (GERMANY: POTA) remains a highly speculative bet, but the reward could be spectacular.

Disclosures / Disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Portofino Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Portofino Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Portofino Resources was an advertiser on [ER] and Peter Epstein owned shares and warrants in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.