Five weeks ago, gold hit an all-time high of US$2,073/oz. Since then, it’s down 6.2% to US$1,944/oz. (still above 2011’s record level). Yet, based on the share price declines in some well known juniors, one would think gold was down 2-3 times as much.

Apollo Gold is down 52% from its recent high, Evergold Corp. is down 51%, Freegold Ventures; down 45%, Vizsla Resources; down 41%, Spanish Mountain; down 38% …. dozens of juniors are off > 35%.

Is now the time to give up on gold? Never in the past 15+ years that I’ve been following this sector have I been more bullish on gold fundamentals. However, my optimism is not predicated on the price soaring, it’s already quite high. I believe it will remain strong well into 2021.

In a world gone mad, gold junior stocks make sense as a safe haven

Elevated uncertainty in my home country, the U.S., due to economic, COVID-19, race relations, climate change & protracted political concerns, will not end soon. We have a Presidential election in seven weeks, but the next President is not sworn in until January 20, 2021.

If the election is contested, which seems increasingly likely, it could be months before things calm down. Or, the situation could spiral out of control, making 2021 worse than 2020. The chances of smooth sailing? Close to zero.

If a second wave of COVID-19, in concert with the typical Flu season, hits this Fall/Winter, the money printing exercise will be much larger & longer lasting. All roads lead to bullish backdrops for gold juniors

If gold was ever a safe haven asset, now might be a wise time to own gold stocks. Adding to the growing fear & uncertainty, on multiple fronts, is unprecedented money printing, deficit spending & debt issuance around the world.

In the U.S., 2020’s fiscal deficit will be nearly $4 trillion, ~18% of GDP. In 2009, the worst year of the Great Recession, the deficit was 9.8%. The last time it approached 20% was during WWII. Globally, deficits will be huge this year, and possibly quite large again in 2021.

FenixOro could deliver evidence of a major deposit within 2 months

A company I continue to be excited about, despite it being very speculative, is FenixOro Gold Corp. (CSE: FENX). Despite the correction in the junior space, FENX shares have been surprisingly resilient. If I’m mostly right on gold fundamentals, and if the drill bit delivers some high-grade intercepts, there could be a re-rating in FenixOro’s valuation before year end.

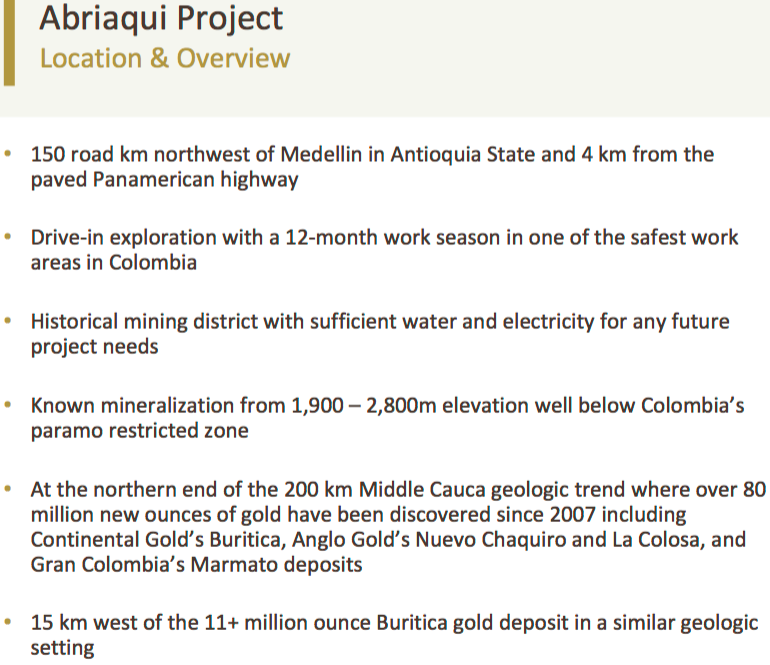

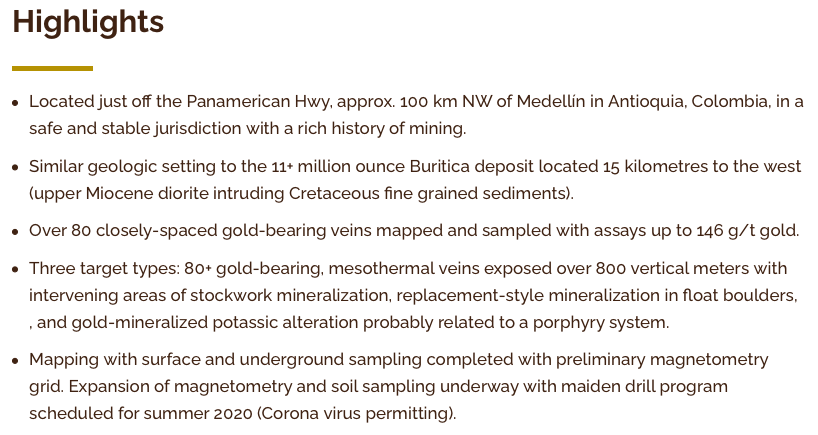

Make no mistake, FenixOro is a speculative low-cap play, but given the state of the world, investors might benefit from owning gold juniors. The big news this month is that the Company’s drill permits have been issued. This means we are a few weeks from starting a critically important drill program on the 100%-owned Abriaqui project in northwestern Colombia.

Readers may recall that earlier this year, evidence of porphyry-style gold mineralization was discovered in a mineralized surface outcrop. The alteration type & grade identified is typical of gold-bearing portions of mineralized porphyry systems around the world.

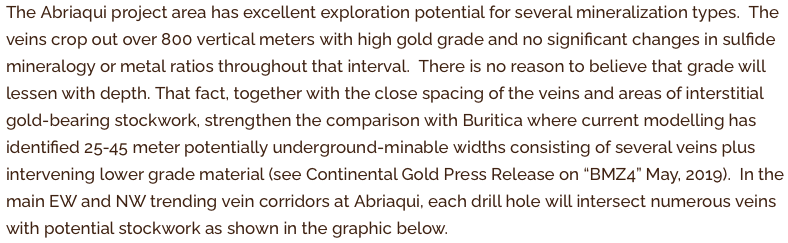

Ground magnetics defined a strong near-surface anomaly measuring about one sq. km. Analysis indicates that it continues on, at roughly the same diameter, to a depth of > 700 m. Already, 1 km length x 1 km width x 700+ m depth = a potentially attractive deposit. Large-tonnage porphyry deposits of > 1 g/t gold have the potential to be long-lived, low-cost, cash-generating machines.

Is FenixOro’s 100%-owned Abriaqui project the next C$2B Buriticá?

The primary target at Abriaqui is a sequence of > 80 closely-spaced, high-grade veins developed in 500m wide corridors, of which > 20 have assayed 20 g/t+ gold, and up to 146 g/t gold. They outcrop over 800+ vertical meters with areas of intervening lower grade mineralization.

Near-term catalysts like drilling, new discoveries & strong results are often well rewarded in bull markets. Management is optimistic about this particular drill program due in large part to the nearby, world-class C$2B Buriticá project’s geology, but also a recent ground magnetometry survey, promising soil sampling results & geo-chem studies.

Ten angled drill holes (4,500 meters) have been carefully planned, one searching for a large-tonnage gold porphyry target. Four drill pads and a core shack facility are being built right now.

A vertical depth of 300-350m is considered to be ideal for these first passes. If successful, management would likely do an additional 1,500-2,000 meters in this phase.

CEO John Carlesso commented,

“The preliminary exploration program has had a lot of success and we’ve generated multiple new target areas for the drilling that’s about to begin. We’re seeing potential for much more of the high-grade “Buriticá–style” vein mineralization throughout the full extent of the project, and we’ve identified a potential large-tonnage, gold porphyry target. With drills now being mobilized, our entire team is eager to uncover the full potential of the Abriaqui project.”

In speaking at length with FenixOro’s VP of Exploration Stuart Moller, who led the discovery team at Buriticá for Continental Gold (acquired by Zijin Mining) from 2007-2011, he explained that the COVID-19 situation in & around the project area is well contained. There have only been a few cases, and no new ones in the past month. Work is progressing without any restrictions.

Very serious 10-hole drill program (4,500m) testing new zones….

Next, we discussed the imminent drill program. He assured me it’s not going to be about twinning high-grade holes to generate a feel-good press release. No, the technical team has had months to develop optimal drill targets and they think they have nailed it.

The program will drill-test, for the first time, six or more families of stacked, high-grade vein systems. Each target is distinct, drilling will go after showings at different depths, angles & orientations, across multiple types of mineralization.

Many new veins will likely be identified. Management expects to gain valuable insights on grades, depths, continuity, vein spacing & widths. In addition, a better understanding of indicative grades / thicknesses between, above & below newly discovered & existing higher-grade zones is forthcoming.

If enough higher-grade vein material exists, interspersed with wider zones of 2+ g/t material, there could be one or more compelling deposit(s). In fact, management believes results from the recently completed soil sampling program point to this distinct possibility. Evidence of a potentially meaningful project will be shared within a few months.

Most juniors require multiple drill programs (and capital raises) over multiple seasons to get a decent glimpse of what their properties might hold. However, due to FenixOro’s project so near to the giant Buriticá project, and that the two projects share geological characteristics, and the considerable amount of exploration work done — drill results should give investors good visibility into the Company’s prospects.

That’s why I believe FenixOro has the potential to experience a re-rating in valuation upon the release of assays, expected to begin being received by November, that would tie Abriaqui ever closer to the nearby 12M+ ounce Buriticá project.

Readers please note, I don’t use the term “re-rating” lightly. Buriticá is not just an attractive analog deposit, it’s one of the world’s premiere advanced-stage, high-grade gold development projects. Commercial production is expected there within six months.

I asked Carlesso & Moller about the share price, which has enjoyed a nice move. Have investors missed the boat? While no one can predict the future, they indicated that some institutional investors are waiting for drill results before potentially initiating a position. This is common for small-cap exploration plays; passing on potential earlier-stage, higher-risk returns, and trying to capture smaller, but less risky gains.

This suggests FenixOro Gold Corp. (CSE: FENX) is not a go-go stock about to run out of steam. The best comparable project, which happens to be just 15 km away — is soon to be a world-class, high-grade mine — valued at roughly 60 times FenixOro’s C$33M valuation.

Near-term, very impactful investment catalysts are right around the corner. I strongly believe there’s room for the valuation gap to shrink upon further de-risking of the Abriaqui project.

Disclosures: The content of the above article is for information only. Readers fully understand & agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about FENIXORO GOLD CORP., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc., is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, professional trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of FENIXORO GOLD CORP. are highly speculative, not suitable for all investors. Readers understand & agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed & agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, FENIXORO GOLD CORP. was an advertiser on [ER] & Peter Epstein owned shares in the Company.

Readers understand & agree that they must conduct their own due diligence above & beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.