Nicola Mining (TSX-V: NIM) / (OTCQB: HUSIF) has methodically built a diversified mining enterprise in southern B.C., Canada. Today, it announced an exciting addition. Management signed a LOI with High Range Exploration to acquire 50% of the Dominion Creek property, ~110 km east-southeast of Prince George.

Nicola will have an effective 75% economic interest in the 1,950-acre project. The two companies will work towards a 10,000-tonne bulk sample next year. In 1992, eighty tonnes of concentrate was shipped to a smelter. The mill head grade was 14.1 g/t gold and the recovery was 93%.

Source: August, 2003 Dominion Creek Project Technical Report for XMP Mining Limited, David K. Makepeace, P.Eng. (Section 4.6: Page 18)

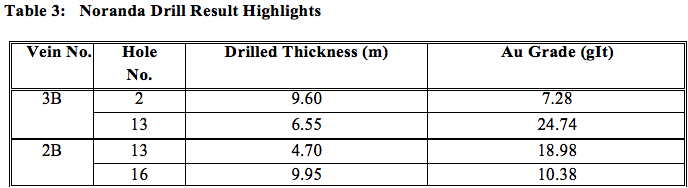

In the early 1990s, Noranda Exploration drilled 53 holes, totaling 3,484 meters (average depth ~66m). Results included 18 intercepts of 1 to 10 meters in thickness, with grades ranging from 4 to 40 (g/t) gold. There are two clear mineralized areas that include a small bulk sample pit and a mineralized outcrop containing multiple distinctive veins.

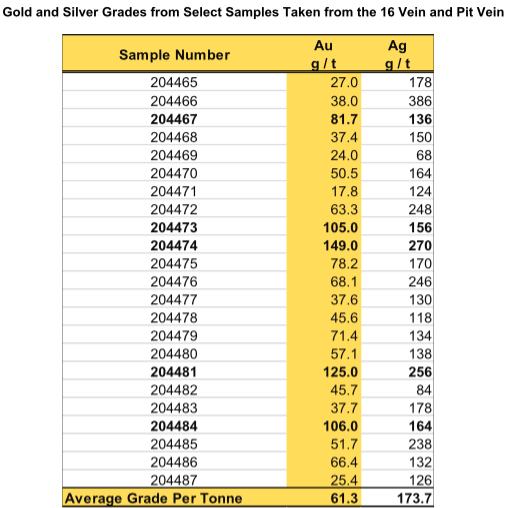

As impressive as the historical drill results are, even better might be the much more recent surface samples. As can be seen below, 23 select samples from July averaged 61.3 g/t gold. That’s ~2.0 ounces. The top five averaged 113.3 g/t gold (~3.6 ounces). These blockbuster grades are quite impressive, rarely seen anywhere in the world.

Note: {high-grade samples are nice, but the truth is in the drilling — grade + interval width + depth + continuity — will tell the tale}.

The Golden Triangle in northwestern B.C. has pockets of very high-grade gold / silver. However, management points out that all-in drilling costs in southern B.C. are typically half as much.

Earlier this month, Nicola & High Range announced a Strategic Mining & Milling Profit Share Agreement calling for 0.5 oz./tonne (15.55 g/t) gold equivalent material to be delivered to the Mill from High Range’s Dominion Creek property.

Note: Grab samples are selected samples and are not necessarily representative of the mineralization hosted on the property.

Typically, Nicola splits profits 50/50 with third-party miners that provide ore to feed the Merritt Mill. Since the Company will own half of this high-grade gold + silver deposit, total economics for Nicola increase to 75%.

This is a tremendously attractive deal. The exact deal terms are not terribly important because Nicola will be fully reimbursed for all partnership start-up costs, expected to be about $525k.

How profitable could this deal be? As a frame of reference, from an initial 10,000-tonne bulk sample, at the agreed upon 15.55 g/t gold minimum, about 4,500 ounces could be liberated (assuming a 90% recovery).

That would generate ~C$11.4M (at spot) in gross revenue and take 60 days to process at 166 tonnes/day throughput (nameplate capacity = 200 tpd). If the operating margin were 25%, that suggests annualized cash flow potential of ~C$17.1M, of which 75% (~C$12.8M) would belong to Nicola.

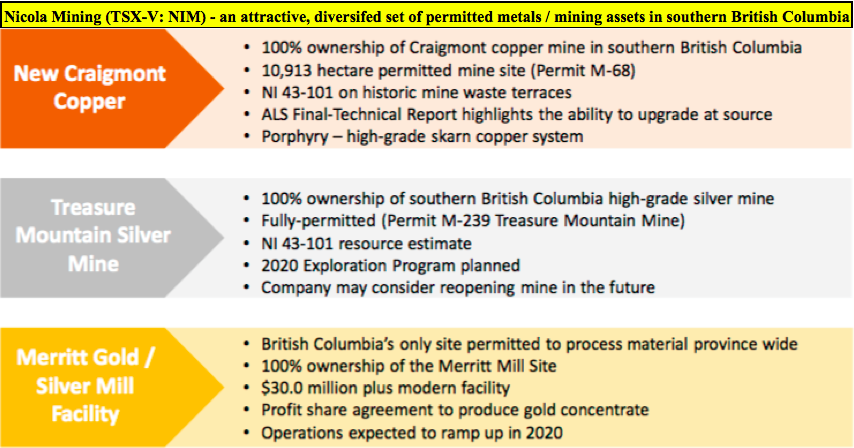

Three increasingly valuable mining assets in southern B.C.

Would it be an exaggeration, or overly aggressive, to say that Nicola Mining has three potential company-making assets? I think not. Consider the facts.

1] A modern, permitted gold / silver mill & lined tailings facility

One hundred percent ownership of a modern (2012) gold / silver mill facility in B.C. with a fully-lined tailings facility that has had $32M invested in it, and is the only mill in B.C. permitted to process feedstock material from anywhere in the province.

That’s a great provision to have in your back pocket as gold & silver prices rise (increasing the distance third-party ore can economically travel to Nicola’s Mill). The strategically important Merritt Mill is worth significantly more at $1,900 gold than it was at $1,261/oz. gold (the avg. price from 2014-2019).

With a larger universe of prospective customers AND higher gold prices, operations could be optimized (selecting higher grade feeds, less Mill downtime) like never before. The value of this scarce mining asset is probably twice Nicola’s entire market cap. It would be nearly impossible to get a new mill permitted in B.C. in under five years, if at all.

2] Craigmont Copper; host of former high-grade Craigmont Mine

The 100%-owned, 10,913 hectare permitted Craigmont copper project is a brownsfield site adjacent to Highland Valley Copper, North America’s largest copper mine. From 1961-1982, the Craigmont Mine produced 34 million tonnes, (nearly a billion pounds), averaging 1.3% copper from underground & open pit operations.

In recent years, both porphyry & skarn mineralization has been encountered. The best recent drill results at Craigmont are; 85.6m at 1.1% Cu in 2016, and 1) 150m at 0.54% Cu, including (5.0m @ 9.6% Cu), 2) 100.6m at 1.3% Cu and 3) 71.4m at 0.6% Cu, in 2018.

An estimated 53.5M pounds of copper are contained in above ground waste piles. Management has had success using ore sorting technology in trials, upgrading low-grade ore by a factor of five, with a modest loss of copper.

The outlook for copper is strong. It’s one of the very few metals that benefits from high-tech, green energy, renewables, new grid-scale power systems / electrification of transportation / 5G network buildout / trillion dollar infrastructure spending (boosted by debt-funded stimulus plans).

The copper price at $3.08/lb. has held up remarkably well given the ongoing global pandemic. Average copper grades at mines across the globe continue to fall. Some top copper-producing countries, like Chile, are experiencing (to varying degrees) rising costs, local community / NGO / environmental opposition, political trends towards populism & water concerns.

High-grade copper in southern B.C., where deep open pit mines are running on fumes, (grades of 0.25%-0.30% Cu), will be increasingly valuable, especially if/when copper rises above $4.00/lb. in coming years.

3] High-grade, permitted Treasure Mountain Silver mine project

The 7,000-acre Treasure Mountain Silver mine has near-term (2021) cash flow potential from reopening and mining Level 1, Stope 2 of this 100%-owned silver, lead, zinc project. However, the real blue-sky potential is in exploring. Some of the best historic soil samples range from 2,250 to 9,221 g/t silver (72.3 to 296.5 ozs./tonne), 0.30% to 1.02% copper, and 0.59 to 0.81 g/t gold.

In August, Nicola announced that it had completed the first phase of a soil sampling program, including 304 of a planned 530 samples collected over the MB zone and to the southwest. Five outcrops were identified hosting mineralized vein material which were grab sampled. Some shallow drilling was also done.

The locations of sampling indicate a potential strike length of ~1.2 km. This area had not been previously investigated by the Company. Soil samples are undergoing lab analysis. Westhaven’s nearby Shovelnose project has been reporting high-grade drill results since 2017.

Management believes that Treasure Mountain’s results are very encouraging as they identify the potential for other mineralized structures outside of Treasure Mountain’s underground mine workings, which were under-explored by prior operators.

Until just a few months ago, Treasure Mountain was an interesting out-of-the-money call option on the underlying price of silver. Above $20-22/oz. silver, it’s time to start thinking of the possibilities. Above $24-$26/oz., active exploration & the possible development of low hanging fruit is warranted. Six weeks ago, silver traded as high as $29.9, but has settled back to $24.45/oz.

CONCLUSION

Nicola Mining offers the relative safety of near-term cash flow and 100% ownership of a valuable hard asset (the Merritt Mill), plus substantial blue-sky exploration / development upside in copper at Craigmont & silver, lead, zinc at Treasure Mountain.

Near-term investment catalysts & news flow should be plentiful. I recognize that the Company has experienced delays in achieving meaningful cash flow from its Mill, but the world has changed this year. Gold at $1,900/oz. is 8.3% below its all-time high of $2,073/oz. and the silver price has doubled since mid-March, even after recently pulling back from $29 to $24/oz.

Yes, $1,900/oz. is a far cry from $1,200-$1,400/oz., the price in place for most of 2014-2019, where miners had difficulty funding start-up costs & working capital swings to mine and supply ore to the Merritt Mill.

There are dozens of larger companies that might want to partner on Craigmont or Treasure Mountain if Nicola Mining’s (TSX-V: NIM) / (OTCQB: HUSIF) management team wanted to move in that direction. Or, self-funding with operating cash flow could be the chosen path forward. Bull markets provide a multitude of options. Either way, the future looks bright.

Disclosures: The content of the above article is for information only. Readers fully understand & agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Nicola Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc., is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, professional trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Nicola Mining are highly speculative, not suitable for all investors. Readers understand & agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed & agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Nicola Mining was an advertiser on [ER].

Readers understand & agree that they must conduct their own due diligence above & beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.