I’ve been waiting for BIG NEWS from Cypress Development Corp. [CYP] (TSX-V: CYP) / (OTCQB: CYDVF), a lithium (“Li“) junior with 100% ownership of an unconventional, clay-hosted (sedimentary) Li project at Preliminary Feasibility Study (“PFS“) stage. {Please see PFS here}.

Slow but steady progress, de-risking the CVLP project

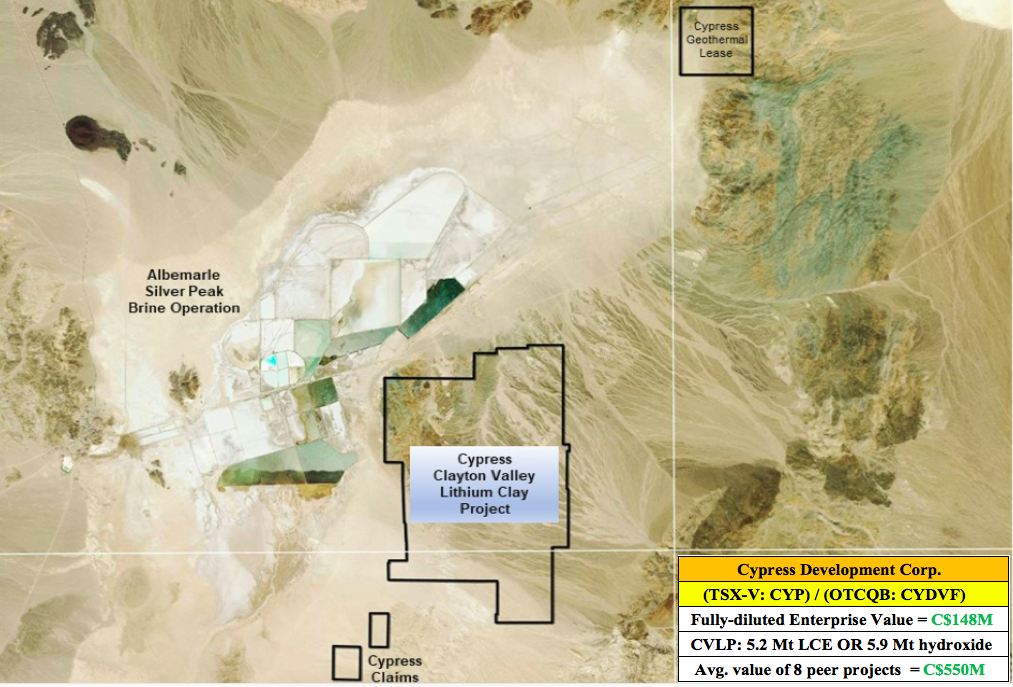

The Clayton Valley Lithium Project (“CVLP“) sits on 5,430 acres, hosting a Measured & Indicated resource containing enough Li to make EITHER 5.2M tonnes of Li carbonate, OR 5.9M tonnes of hydroxide. In the mid-2020s, management plans to begin ramping up to production of ~31.1k tonnes/yr. of battery-quality hydroxide.

On Jan. 28th, management put out a press release that, while not what some were hoping for, is still pretty damn important. {Please take a moment to see management’s February, 2021 Corporate Presentation}

Readers may recall that Cypress and a handful of Li juniors in Nevada, including the much larger [by market cap] Lithium Americas (“LAC“), are trying to exploit Li efficiently & responsibly from claystone deposits of varying grades, geologies & depths.

LAC has been trying to crack the clay code for > 10 years. Cypress CEO Bill Willoughby, Phd PE, and his technical team are benefiting by standing on the shoulders of expert geological, engineering & metallurgical consultant groups, plus work done for decades by various Nevada state & federal agencies. {Please see images in this article for consulting groups & CYP’s technical team}

Cypress, LAC and clay-hosted Li peers Bacanora & Australian-listed ioneer ltd., propose using sulfuric acid to leach Li into solution. While this has worked for some companies, in lab & pilot-plant settings, it has never been achieved at commercial-scale. There are many process steps and a number of materials handling challenges.

Cypress has a robust PFS using a sulfuric acid flow sheet….

For example, Cypress needs ~650 tonnes of sulfur (per day) delivered to site and burned in a custom-built acid plant to make sulfuric acid. Nevada peers — some of whom have reported much higher sulfuric acid consumption (per tonne/ore) — would need to move considerably more than 650 tonnes/day.

This presents logistical constraints on how much Li can efficiently, safely & cost-effectively be produced (in strict adherence to environmental protocols) at any given project site. This factor explains why Cypress is proposing a modest (relative to its > 5M tonne Measured & Indicated resource) operation delivering 27.4k tonnes LCE/yr., OR 31.1k tonnes Li hydroxide.

In re-reading these four press releases [Jan. 28th] [Dec. 16th] [Dec. 3rd] [Nov. 24th], it seems that management believes they may have found a better way to leach Li from their site-specific geological footprint. In February, the Company is finishing up a scoping-level study of chloride-based leaching (the subject of the above four press releases).

….but could show a strong DFS with hydrochloric acid+sodium chloride

This approach eliminates sulfur / sulfuric acid handling, replacing it with what could be a meaningfully less complex chloride leach-based flow sheet. Environmentally, the project’s CO2 emissions would decline without the need to truck sulfur.

Several positive indications suggest op-ex could be lowered, but tradeoffs between the two flow sheets need to be further analyzed.

In order for chloride-based leaching to be viable, a project needs to have long-term, reliable access to brine or a nearby source of geothermal fluids. And, the project’s geology has to be amenable to leaching Li without too much deleterious material remaining in the end product.

If further testing & pilot plant operations support this thesis, management could deliver an exciting Definitive Feasibility Study (“DFS“) (within about a year). Operationally, Cypress would gain the valuable option of being able to produce > 31.1k tonnes of hydroxide/yr., perhaps substantially more, when the market is strong.

It’s not an exaggeration to say that Cypress could have (depending on DFS results) the best clay-hosted Li project in the world, due to its uniquely favorable combination of 1) geology, 2) proximity to long-term, sustainable sources of brine / geothermal fluids, 3) relatively modest use of water, and 4) extremely low strip ratio, [< 0.15:1.0].

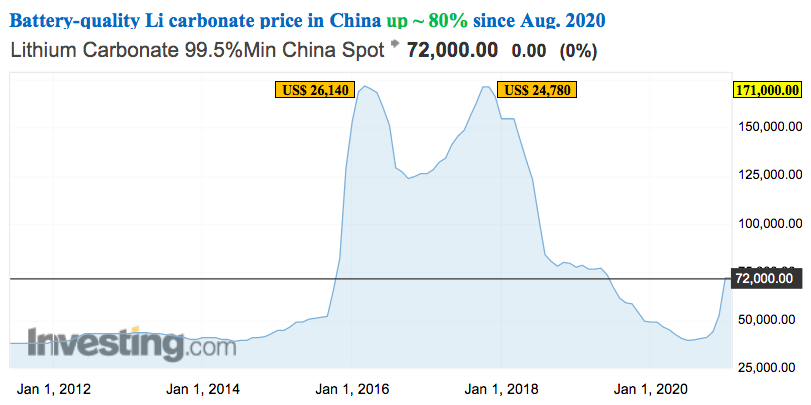

Lithium carbonate price in China up ~80% in past 5 months!

According to investing.com data, the battery-quality Li carbonate price in China peaked (twice) at 171,500 & 171,000 Chinese yuan/tonne in Jan. 2016 & Jan. 2017, respectively. Converted to US$ at prevailing exchange rates, that’s ~US$ 26,140 & ~US$ 24,780/tonne. Consider that in 2017 the global EV penetration rate was < 1.5%.

Imagine the tightness in the Li market if, as many forecasts suggest, EV penetration hits 10%-12% by 2026. Will we see US$20k/t again (periodically) this decade? To be clear, the China price is not the same as the much lower, much less volatile contract price into Asia, but it’s a closely-watched index driving investor sentiment.

2020 was a great year for Cypress and for many Li stocks, but few soared more than CYP! From a COVID-19 March low of $0.11, shares hit $2.45 on January 13th before pulling back dramatically to $1.34. CYP has a fully-diluted Enterprise Value (“EV“) {market cap – cash + debt} of $148M.

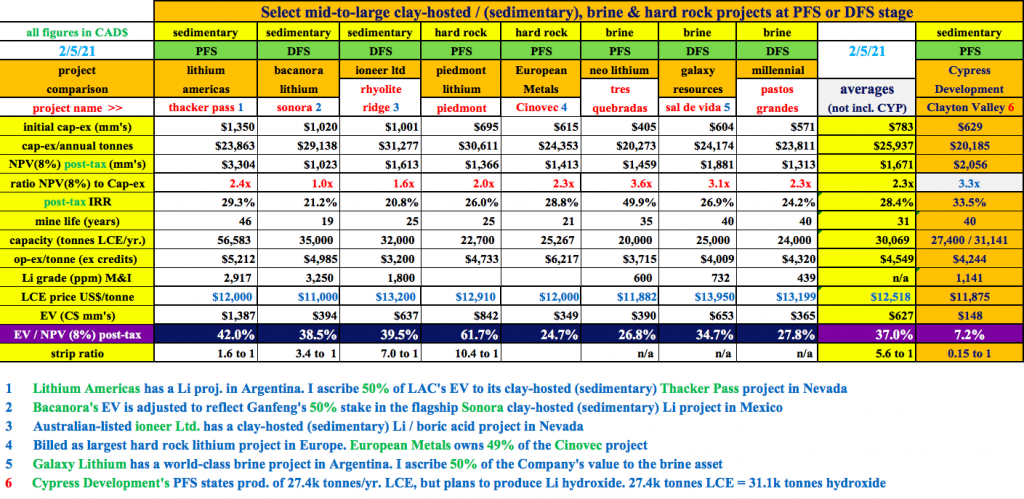

Cypress remains unusually cheap compared to the EVs of eight pre-construction Li companies at PFS or DFS stage. I compare CYP’s [EV divided by after-tax NPV(8%)] ratio — (assuming a LCE price of US$11,875/t) — to the same ratio of peer projects, that have an average LCE price of US$12,518/t.

Cypress valued at 80% discount to 8 peers at PFS or DFS stage

The eight projects have EV/NPV(8%) ratios ranging from 25% to 62%, with the average of the three clay-hosted projects and five conventional projects equal to 37.0%. So, why is CYP’s project trading at just 7.2% of its after-tax NPV(8%), a whopping 80.5% discount to peers?

Less advanced Li projects are valued at a premium to the CVLP as well. PEA-stage juniors {AVZ Minerals, Lake Resources, Galan Lithium, E3 Metals & Argosy Minerals} have projects valued at an average EV/NPV(8%) ratio of 30.7%. The CVLP is trading at a 76.5% discount to those five projects.

Much of the valuation gap might be due to Cypress being less well known than players like LAC & Neo Lithium. That, and being further away from initial production than peers. However, being under-followed & under-appreciated is a good thing for investors looking for attractive investment entry points.

Lithium brine projects; significant delays / long ramp up periods

After widespread multi-yr. delays, 4 or 5 Argentinean brine projects are now expected to achieve initial production by 2023. Every new brine project is critically important to quench the world’s thirst for Li-ion batteries, but each requires a 3-6-yr. ramp-up period. Some projects start with technical grade Li carbonate before moving to battery-quality, some grow in a staged approach.

With a potentially faster ramp-up period to battery-quality Li hydroxide, it’s entirely possible that Cypress could reach 20k+ tonnes/yr. around the same time that Neo Lithium, Galaxy Resources & Millennial Lithium hit their nameplate capacities.

CYP’s CVLP is among a group of ~20 significant new projects (not expansions by existing producers) of 20k+ tonnes LCE/yr. that could possibly start supplying the market by 2026. Of these, I’m guessing roughly five won’t make it. Fifteen new projects over the next five years is not nearly enough (remember the slow brine ramp-up periods).

The world needs 20+ new projects in the next five years and an additional 35+ projects (through 2030). Clearly, that’s not going to happen unless clay-hosted Li is a meaningful part of the equation.

Conclusion

Readers can choose safer Li names like Albemarle, Livent or SQM and probably do well, rising along with the Li price tide. Or, for those with bigger risk appetites, taking a closer look at Cypress Development Corp. (TSX-V: CYP) / (OTCQB: CYDVF) makes a lot of sense, especially after the recent share price decline of 45%.

In coming years, chemical / Li industry Majors, not to mention a few dozen giant auto & battery makers, will be pursuing crucial strategic investments in, and outright acquisitions of, battery metals companies to gain market share and/or ensure security of supply. Cypress offers a very compelling risk/reward proposition in a very compelling sector.

Disclosures / Disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Cypress Development Corp., including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Cypress Development Corp. are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Cypress Development Corp. was an advertiser on [ER] and Peter Epstein owned shares in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.