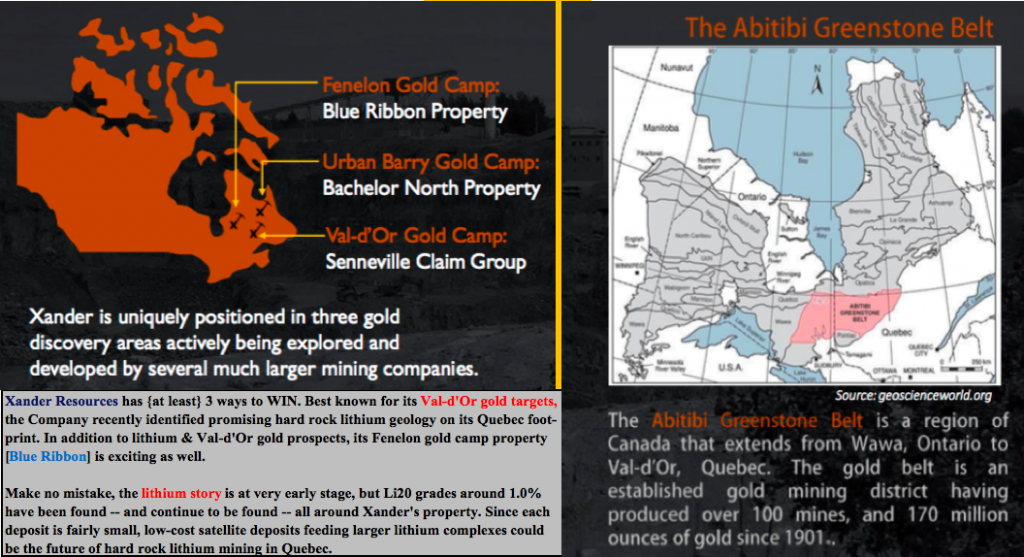

Xander Resources Inc. (TSX-V: XND) (Germany: 1XI) (OTCQB: XNDRF) came out with important news yesterday. In addition to its highly promising #gold portfolio (4 properties in two camps, described below), a portion of the Company’s geology has been interpreted to potentially host a lithium exploration target on the west side of the Senneville Group of claims, at the fringe of the LaCorne Bathoith, ~30 km north of Val-d’Or, Quebec.

Evidence of lithium observed, could it amount to a meaningful deposit?

The lithium geology in question is close to North American Lithium’s (“NAL”) project that has a Measured & Indicated resource of ~33M Metric tonnes (“Mt”) grading 1.19% Lithium Oxide (“Li2O”), and east of Sayona Mining’s BFS/DFS-stage, Authier project containing 25.1Mt @ 1.13% Li2O.

NAL & Nemaska Lithium have been two black eyes for investors & various stakeholders across Quebec. However, both projects are being revitalized with support by new investor groups, and significant tailwinds from a meaningful rebound in lithium prices.

The provincial governments of Ontario & Quebec and the federal government have demonstrated a strong, united commitment to establishing a robust EV manufacturing & development hub with grants, loans, research partnerships & streamlined permitting.

Xander’s prospects are also near Great Thunder Gold’s Chubb property, where historical drill hole intervals include; 1.33% Li2O over 5.3 m, and 1.68% Li2O over 3.7 m. A new drill program of 15 holes totaling 2,500 meters is underway there.

Lithium operations across Canada are coming, especially in Quebec

By the end of the decade, there will be multiple hard rock lithium operations in Quebec. If Xander can delineate a NI 43-101 resource of a few, or several million Mt Li2O, there should be a home for that ore.

How much could a satellite lithium deposit be worth? Hard to say, but Rock Tech Lithium (in Ontario) has 144,350 Mt of Li2O grading 1.1% that’s currently valued by the market at ~$1,800/tonne. If Xander could delineate 2.167M Mt [a sixth the size of Rock Teck’s deposit] grading 1.0%, that would be a resource of 22,167 Mt Li2O.

Assuming this hypothetical 22,167 Mt Li2O is worth a sixth of Rock Tech’s valuation [per tonne], that would be 22,167 x $300/Mt = ~$6.7M. Xander’s enterprise value {market cap + debt – cash} = ~C$4M.

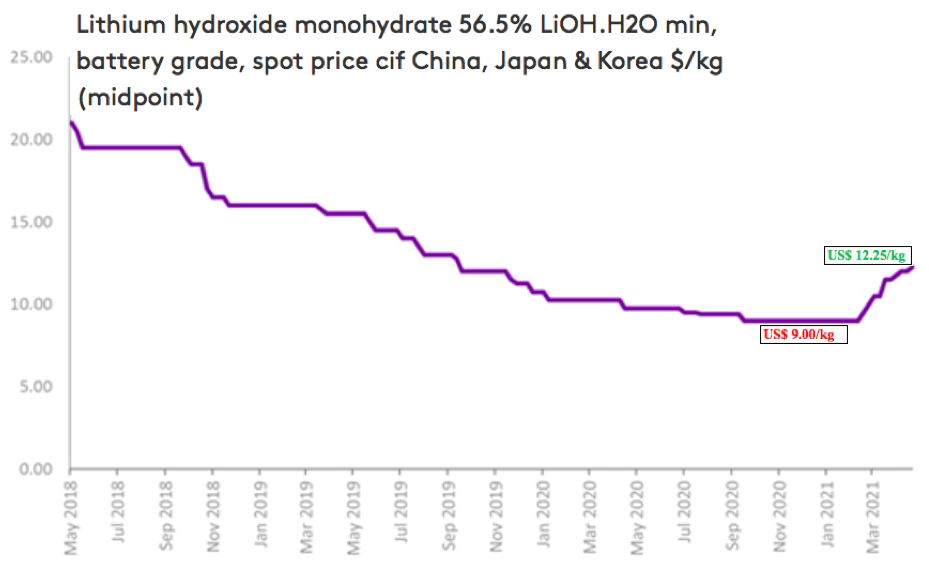

If, as I expect, we’re experiencing a strong lithium market in 2022 / 2023, Li2O in the ground could be worth a lot more than $300/tonne. A single tonne of Li2O has enough lithium content to produce 2.473 tonnes of lithium hydroxide. Hydroxide is currently valued by Fastmarkets at US$12,250/Mt.

Each third-party sourced tonne of Li2O (from a satellite deposit) run through an operator’s mill could potentially be sold for [$12,250 x 2.473= US$30,294 (gross revenue / assuming 100% recoveries).

There are about a dozen small hard rock lithium hopefuls in Quebec alone. For instance, First Energy has lithium prospects near Xander. It had recent channel samples assayed, returning attractive grades — that company’s market cap is C$18M. Larger plays in Quebec include Australian-listed Galaxy Resources’ James Bay and Critical Elements’ ($232M market cap) Rose Lithium projects.

Low-cost satellite deposits could become valuable to nearby operators

To be clear, there are a number of significant expense items tied to transporting, storing, handling & processing the 1% Li2O ore, and disposing of the tailings — but there’s plenty of room for substantial profit.

A knock on hard rock projects in Canada is that they’re quite small compared to most brine & clay-hosted lithium projects. Therefore, in my opinion, not only are satellite hard rock lithium deposits in Quebec potentially viable, they could be in high demand. Multiple operators could compete to control the best deposits.

Moreover, if Xander could book a larger resource of say 5M tonnes at ~1.0% Li2O, it could find itself in a similar place as some of the above-listed Li juniors. It could warrant a market cap in the tens of millions of dollars (not including the value of Xander’s four gold properties).

Make no mistake, it’s still early days for this lithium opportunity. Hopefully management will be able to get boots on the ground soon to learn more. In the meantime, any good news for lithium projects in Quebec is good news for Xander Resources.

While this lithium news is exciting, that’s just one part of the Xander Resources story. The Company also has three gold properties in Quebec and another in the Fenelon Camp. The Senneville claim group is located in the eastern part of the Abitibi Greenstone Belt, ~25 km north of the gold mining centre of Val-d’Or. {please see April 2021 corporate presentation}

The claim group comprises a total of ~10,522 hectares (~26,000 acres) in three groups, Senneville East, West & South. Modest prospecting & geophysical programs was done last year.

3 promising gold prospects in Val-d’Or Quebec with blue-sky potential

In April, Xander agreed to acquire a 100% interest in 20 mineral claims contiguous to the eastern boundary of its Senneville East Claims, north of Monarch Mining’s ($62M mcap) recently acquired claims, contiguous to Probe Metals’ ($206M mcap) new discovery to the south, and close to a producing mine owned by Eldorado Gold to the southwest.

Regarding the recently acquired gold claims, CEO James Hirst stated,

“We’re excited to acquire further mineral claims on the contact area of the Pascalis Batholith in our East group of claims that are contiguous to Probe Metals. Monarch Mining recently added mineral claims adjacent to the east of our claim group signaling greater interest in the immediate vicinity. We’re pleased to be surrounded by such first-rate companies.”

This year, Eldorado’s Lamaque operation is expected to mine & process > 750,000 Mt of ore @ 6.6 g/t Au. Small mid-tier producer Wesdome Gold Mines is actively exploring its brownfields asset — the Kiena Complex — a fully permitted former mine with a 2,000 tonne-per-day mill. O3 Mining’s ($172M mcap) Cadillac Break Properties are early-stage, with recent drilling only to ~150 m depth.

The first three of a nine-hole drill program on the Senneville South/Senneville East properties was completed about two weeks ago. Assays are expected in June. The initial three holes identified favorable host structures.

Management completed the logging & splitting of core totaling 980 meters. So far, the holes confirm that gold mineralization extends greater than 361 meters along strike.

Based on the outcome of the initial three holes, at least six more will be drilled. The former operator of the 2012 drill program was onsite, he confirmed that the holes encountered the same gold-bearing mineralization as was found in a number of previous holes, two of which returned 9.8 g/t Au & 11.0 g/t Au over 1-meter intervals.

Blue Ribbon property in exciting, highly prospective Fenelon gold camp

The 1,855 hectare Blue Ribbon property is 11 km southwest of Wallbridge Mining’s Fenelon Mine project and contiguous with Probe Metals, Midland Exploration & Great Thunder Gold. Management believes Blue Ribbon is the only property with gold found at surface. There’s been virtually no subsurface exploration.

In 1969 a geologist located an old trench that contained a few specks of native gold. In 1986 a value of 8.5 g/t gold over 0.76 m was obtained. In September 2020, Xander conducted an exploration program on the property that included four trenches 3 x 7 metres wide by 20 x 30 meters long. A total of 40 samples were obtained, assays are pending.

Conclusion

Xander Resources (TSX-V: XND) / (OTCQB: XNDRF) / (Germany: 1XI) has four gold properties, each with active, ongoing exploration being done. Plus, a potential hard rock lithium prospect, all located in mining friendly Quebec, Canada. I could go on and on about how bullish I am on lithium market fundamentals (due to the surge in EV sales around the world, with no end in sight).

Suffice it to say that at US$10-$12,000/Mt pricing, a lot of lithium hydroxide supporting deposits in Quebec will be in-the-money. And, I believe hydroxide prices will be US$16-$18,000+/Mt later this decade, for years at a time. The lithium land rush is on.

Readers are reminded that it’s way too early to say that anything (at all) will come from the lithium opportunity, and the gold prospects are, likewise, early stage. However, with an enterprise value of just C$4M, and multiple ways to win, what do readers have to lose?

Disclosures / Disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Xander Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Xander Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Xander Resources was not an advertiser on [ER] and Peter Epstein did not own shares, options or warrants in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.