16.06.2021 – 12:40 by Profiteer

The following CEO Interview of Cypress Development’s Bill Willoughby, PhD was done by German group Profiteer. They did a great job on the interview, so, I thought I would extend its viewership with a Guest Post on Epstein Research. Note, Cypress Development Corp. is a current advertiser on Epstein Research. Without further ado, here’s the interview….

The environment for our top pick in the Li sector, Cypress Development Corp. [TSX-V: CYP] / [OTCQB: CYDVF] / (WKN: A14L95), could hardly be better. The Cypress share price hasn’t really come out of the crease yet, but it’s only a matter of time.

The current market cap of our top pick is just US$97.6M. By comparison, the after-tax NPV(8%) of the Company’s project, based on a price of US$12,000/metric tonne Li carbonate, is over US$1.6 billion. This undervaluation is striking. That’s why we did the following interview of Cypress’ CEO. Bill Willoughby, Phd.

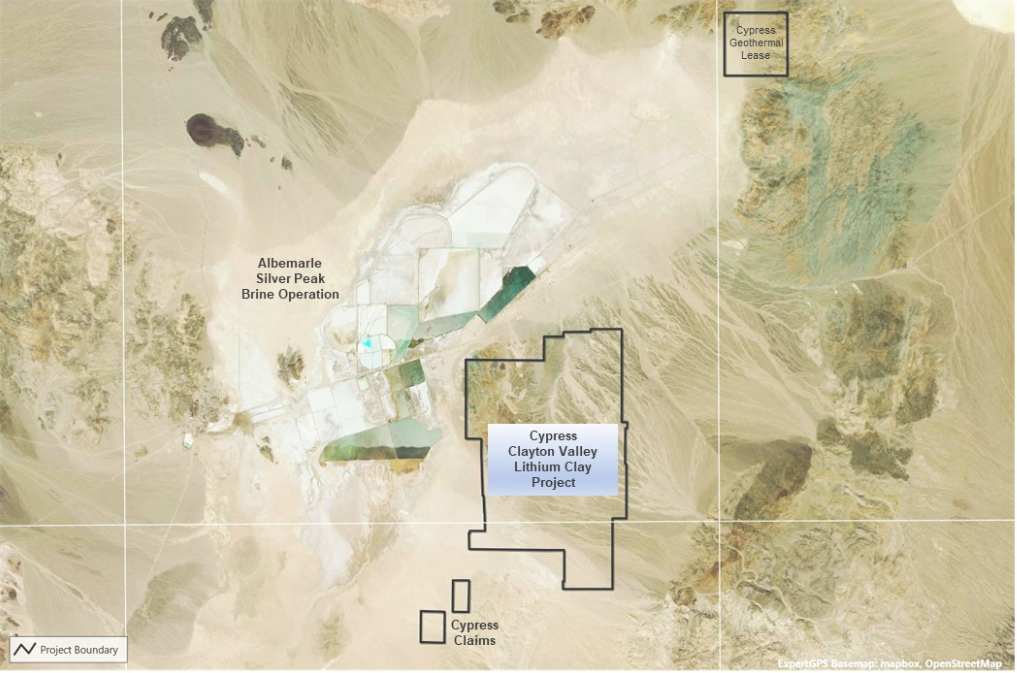

Profiteer: Dr. Willoughby, Cypress is developing a large Li clay deposit in Nevada, next to Albemarle, not far from Tesla’s Gigafactory. Can you please explain the next steps on the way to production?

Dr. Bill Willoughby: Our next actions are those of a project at Pre-Feasibility Study (“PFS”) level. We’re working on processing, permitting, and other areas necessary to advance the project to a [Bankable/Definitive] Feasibility Study (“FS”), which we hope to finish in the first quarter of next year.

The key portion of the FS is the pilot plant, which is under construction now. This part of the process is different from the typical development of a mineral project, as there are not any Li clay deposits in commercial production. We’re doing the work at a metallurgical facility in Amargosa Valley, south of our project in Clayton Valley, Nevada.

With respect to permitting & financing, we’re fortunate to have added two excellent people to the Company, new CFO Braam Jonker and Board member Cassandra Joseph. Both are highly experienced with the permitting & operating environment in Nevada and in guiding companies at our level forward.

Profiteer: How far along is the pilot-plant? When will we know if the chloride leaching process is successfully working? Will you go into off-take agreement talks as soon as you have battery-quality Li samples in hand?

Dr. Bill Willoughby: We’re making excellent progress assembling the pilot plant, almost all equipment is on site or due to arrive this month. We’re leasing space in a gold metallurgical & refining facility. The staff at the del Sol Refinery are highly-skilled and great to work with, allowing the set-up to go quickly & smoothly.

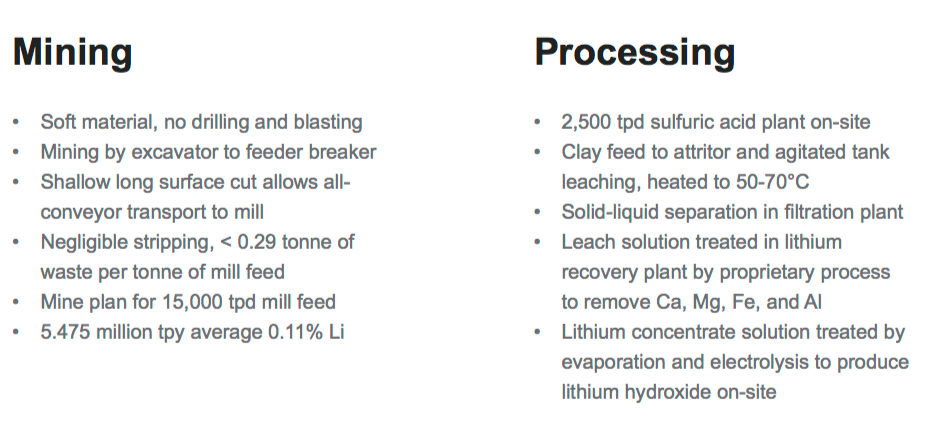

The pilot plant consists of four main areas; leaching, tailings handling, solution treatment / filtration, and Direct Lithium Extraction (“DLE”). Once these areas are assembled & operating, we will know within weeks how each is performing and if we’re on the right path with chloride leaching. All of our initial investigations suggest that it should work, it’s more a case of how well it will work at pilot-scale.

Two additional steps will be completed off-site, first is the treatment of the concentrated Li solution to make Li hydroxide, and second — the recycling of stripped leach solution. These steps will be performed by NORMAM Engineering, using fluids produced by the pilot plant.

At this point we can’t predict when, or with whom, we engage to sell Li products. Our first orders of business are to produce a saleable product and ascertain its potential market for the FS. No doubt that will mean sending samples to prospective buyers & strategic partners.

Profiteer: Are you planning more drilling to increase the Li resource for the FS? If yes, how many holes / meters? Are there Rare Earth Elements on your property?

Dr. Bill Willoughby: We have no plans for additional drilling at this time. We have ample reserves derived from the model in the PFS, at a level of confidence necessary to carry a mine plan in a FS. We do have consultants in mind for the FS, so we will see where we end up on additional work which might include some drilling for condemnation or confirmation.

There are REEs present in the claystone and in the resulting leach solutions from our project. Our focus right now, however, is on perfecting the production of lithium. Here we have engaged Chemionex and are working to license their Lionex process for DLE. Chemionex is finishing the assembly of their equipment, which we expect to be in Amargosa Valley later this month. This is a key part of the pilot plant and we have high expectations for its success.

Profiteer: In the PFS, battery-grade Li carbonate was estimated at US$9,500/tonne, but is now trading around US$13,500/tonne. What are your expectations on pricing over the next 5-10 years?

Dr. Bill Willoughby: I leave Li price forecasting to the Li price forecasters. We know Li demand is growing, led by the electrification of the auto industry, and Li consumption is expected to increase by three times from last year to 2025.

While there is an apparent supply gap, I know from years of experience working in metals that gaps tend to get filled, often by existing producers, and through innovations in processing & recycling. DLE, using membranes or ion exchange resins could be the disruptive technology.

What I want for Cypress is to be at the forefront technology, with a project that’s sustainable, has a low operating cost, is environmentally friendly, with strong economics & investors returns.

Profiteer: If we use US$12,000/tonne of Li carbonate and an 8% discount rate, we arrive at an after-tax NPV of US$1.6 billion for Cypress’ Clayton Valley project. Your market cap is currently at around US$98M. Do you think that you will be able to close the valuation gap to LI peers?

Dr. Bill Willoughby: When you say ‘peer group’, I think of three advanced Li clay projects, two in Nevada, one in Mexico. These projects have had tens of millions of dollars spent on them. By comparison, Cypress is just getting started. That said, I don’t think of the group as true peers.

Each project has its own physical & geopolitical setting to contend with. One has better grades, another a boron co-product, and the third a wholly different process. Our project is unique in its deposit-type, deposition & location, I don’t anticipate the same nature of challenges these others are facing.

As I mentioned earlier, I prefer not to comment on the price of lithium, other then to say there’s a fundamental difference between the way marketers & major companies look at pricing & NPVs. Our focus is to build a project that will provide both institutional & retail investors with a strong investment case based on long-term sustainable pricing, rather than focusing on short-term price fluctuations.

As to closing the gap with peers, and here I think it’s okay to mean market cap, we will do this on fundamentals. If our pilot plant has success and we navigate our permitting & financing goals, I expect Cypress to do exceptionally well and be a leader in U.S. lithium.

However, we should appreciate that building a $500M (upfront cap-ex only) 40-year project from the ground up takes time & diligence, so while we’re moving forward as quickly as we can, a degree of patience is required.

I’m confident as we continue to advance our FS and de-risk our project through processing & infrastructure solutions, permitting, value accretive funding structures, etc., that the market will recognize the investment value of Cypress. With this will come long-term value investors which will certainly reflect positively on our stock price.

Profiteer: Ganfeng Lithium recently offered to buy the shares it does not already own in Mexico-focused Bacanora Lithium for up to US$264.5M. Does this transaction, for a similar-sized Li clay project at ~94% of its NPV, set a new valuation standard moving forward?

Dr. Bill Willoughby: An interesting question. I do not think that one should look at a specific transaction and infer that its pricing parameters sets a new industry standard. Each transaction should be judged on its own merits and within the strategic considerations of the parties involved. The fact that a company paid 94% of a stated NPV could mean a variety of things.

It’s possible they found something that would improve the economics of the project, or they value their capital differently and are willing to take greater risk to control a supply chain. It’s also possible they see greater value coming in Li markets than what’s reflected in the current NPV, and this would bode well for companies like Cypress.

Profiteer: In April, President Biden was proposing a US$174 billion investment into the EV market as part of a US$2 trillion infrastructure plan. Do you see an opportunity for Cypress to tap into that pool of money for project financing?

Dr. Bill Willoughby: The Biden Administration has stated that they want to see the lithium for EVs to be mined ‘in a responsible way’. (see AP comments from Secretary of Energy Jennifer Granholm). I believe Cypress’ project can and will meet those standards. As to tapping a government pool for financing, that’s something we would welcome.

Profiteer: Do you have plans to obtain a senior exchange listing in the U.S. in 2022? This would make perfect sense because your project is in Nevada and there’s a strong investor appetite for advanced Li exploration companies, i.e. Piedmont Lithium & Lithium Americas.

Dr. Bill Willoughby: I agree that a U.S. listing could make sense in the future, but our immediate focus is our FS. However, a possible U.S. listing will certainly form part of our strategic considerations when we decide on the most value-accretive way to take Cypress to the next level.

Profiteer: Can you please elaborate a bit regarding Cpyress’ corporate structure? Are you planning to swallow a poison pill to avoid a hostile takeover? What is your exit strategy?

Dr. Bill Willoughby: My exit strategy is and has been this; Cypress is on the path to production. Assuming we successfully complete the processing steps required, we are quite capable of adding the people & financial resources needed to take Cypress to the next level.

Our shareholders are generally retail with a minor component of institutional money. We adopted a shareholders’ rights plan last year to afford our shareholders some protection from an undesirable offer. Cypress is in a different place now than we were a year ago. We’re well financed thanks to the capital we raised in March with PI, and we have a project that’s more exciting the further we go with it.

Profiteer: Thanks for the interview and we wish you a lot of success for the future!

Dr. Bill Willoughby: Thank you.