Soon after COVID-19 slammed into N. America in mid-March, 2020 a strange thing happened. Instead of stock markets continuing to plummet, they bottomed just as massive lockdowns began. That was an eye-opener for me.

Another surprise was the incredible strength of Electric Vehicle [EV] sales in 2020, 2021, 2022… If a highly destabilizing, once-in-a-century global pandemic couldn’t slow EV sales, what will? Every major automaker has gone all-in on EVs powered by Li-ion batteries.

Demand for Lithium to be extremely strong…

Lithium (“Li”), cobalt, nickel, manganese & graphite will be in various stages of undersupply for years to come. Some investors think today’s ultra-high Li prices will spur a robust supply response, causing prices to fall substantially.

Many industry experts, analysts, management teams (and me) disagree. In my view Li is more like a specialty chemical than a commodity and demand is growing too fast.

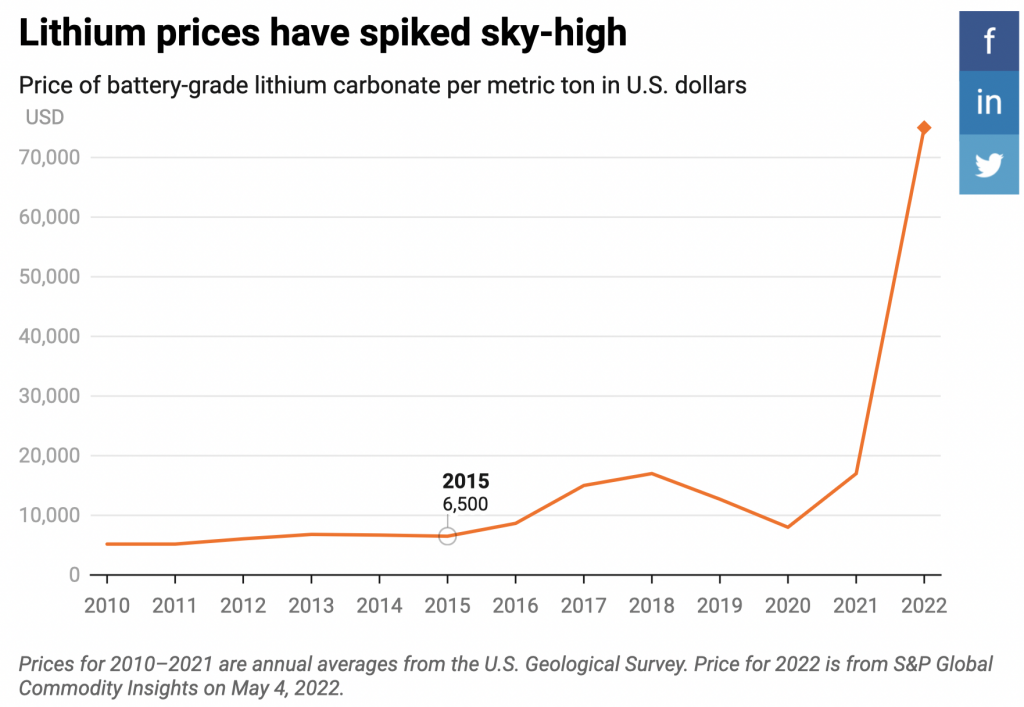

October is the 15th month in a row of very strong pricing with no end in sight. The spot price for battery-quality (99.5% pure) Li carbonate in China at ~US$71,000 (as per investing.com) is triple the twin peaks of 1q 2016 & 4q 2017!

If prices 3x prior peaks — and still at all-time highs — haven’t brought on enough new supply, who knows when prices will decline or by how much.

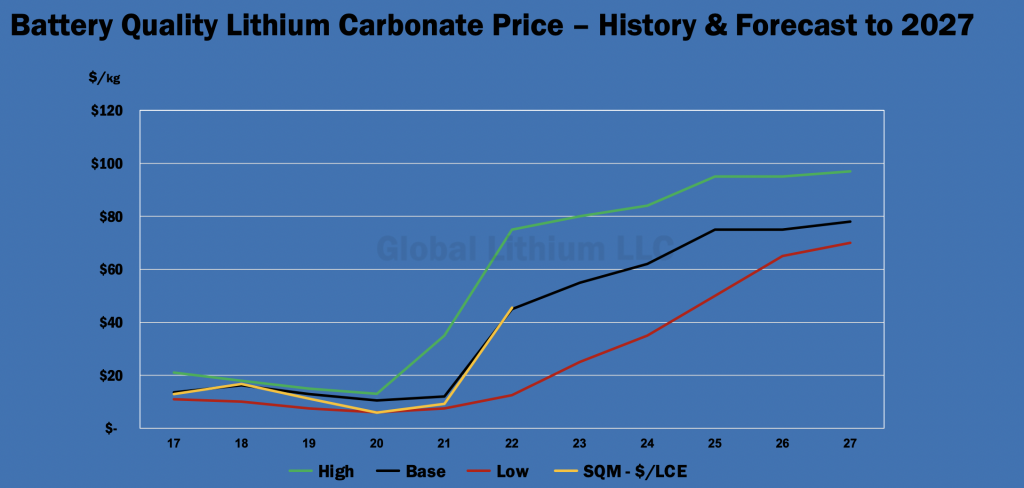

One of the world’s leading Li experts, Joe Lowry of Global Lithium LLC has the following 5-yr price forecast and linked commentary. I believe most sell-side analysts will be increasing their price forecasts to be more in line with Mr. Lowry’s.

Why supply won’t catch up to demand anytime soon…

At a time when Li demand is growing 16%-20%/yr., environmental & water use concerns are lengthening the time it takes a new discovery to become a mine. Visual Capitalist has an excellent infographic showing that it typically takes ~10-12 years from discovery to commercial production.

Some of the driest places on earth host the largest & highest-grade Li brines, but ecosystems in Chile & Argentina can’t sustain decades of increases in water consumption.

Continuing to evaporate brines in S. America, with roughly 50% recovery of Li, is not a long-term solution to Li shortfalls. Can Western Australia’s (WA) prolific hard rock mines and blockbuster new projects save the day? No.

WA is already experiencing worrisome mining cost inflation & labor scarcity as Li competes with iron ore, petroleum & LNG for workers, equipment & services. Seaport & rail capacity could be in short supply as well.

The industry is turning to Direct Lithium Extraction (“DLE”) technologies, promising to meaningfully increase recoveries. The problem is, DLE is not a single technology, and virtually no DLE approaches are proven at full commercial scale.

Although higher recoveries are advertised, most proposed DLE methods still consume a lot of water and require substantially more power than solar evaporation ponds.

In the end, each Li deposit has to be tailor-fitted to the right DLE solution, approved in each jurisdiction and embraced by surrounding communities. That means early-stage DLE projects (post-discovery of a resource) are likely still 6-10 years from commercial production.

What can be done to increase the rate of supply additions?

Li deposits will be tapped via DLE, but unconventional sources also need to be aggressively exploited. Based on known projects in the U.S. & Mexico, sedimentary Li formations, most notably Li-bearing clay deposits in Nevada, could be delivering 100,000’s of tonnes LCE/yr. by the 2030s.

Unlike most DLE methods, extracting Li from sedimentary (non hard rock) deposits has been studied since at least the 1970s. Very substantial progress was made, especially on Nevada deposits, but with Li prices under $7K/t until mid-2015, operating & capital expenses were prohibitive.

Today Li (spot) prices are 10x what they were eight years ago, making Nevada’s Li-bearing clay “science projects” look incredibly more attractive.

Decades of work done liberating Li from various clay settings is being eagerly revisited by companies including Lithium Americas [LAC], ioneer Ltd [IONR], Ganfeng (Bacanora’s Mexican project) & Cypress Development Corp. [“CYP”] (TSX-v: CYP) / (OTCQX: CYDVF).

Those are the most advanced of roughly 30 Li-bearing clay/sedimentary properties/projects around the world. All four have either a Pre-Feasibility (“PFS”) or Feasibility Study (“FS”) completed. IONR has secured a strong strategic partner in Sibayne Stillwater and binding off-take agreements with Ford & Toyota.

LAC has raised half a billion dollars, largely funding a Phase 1, 40,000 tonne/yr. Li carbonate (“Li2CO3”) operation at Thacker Pass [“TP”] in Nevada. In the next 6-12 months LAC expects to deliver a FS, land a strategic partner, begin construction & start signing off-take deals.

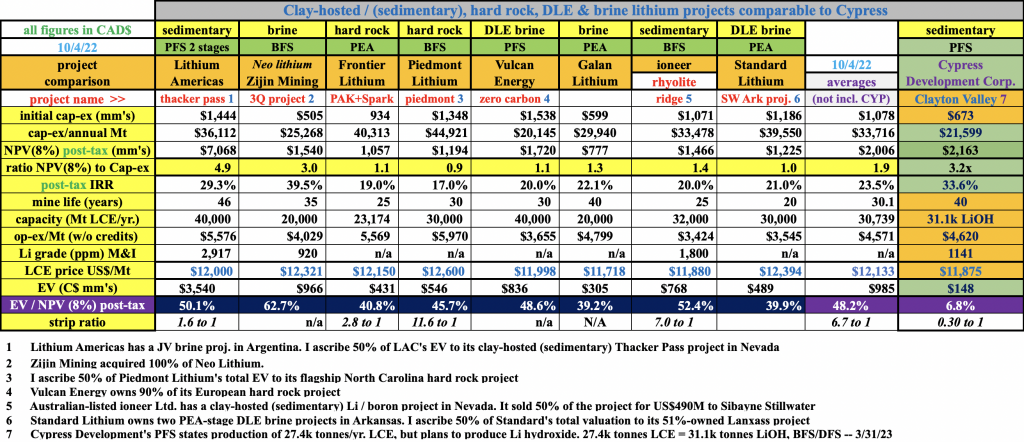

Lithium junior Cypress Development Corp. appears extraordinarily cheap vs. peers

CYP is comfortably funded through delivery of a FS, but won’t reach production before IONR, Ganfeng or LAC. Arguably, that’s not a bad thing. CEO Dr. Bill Willoughby and team will gain valuable insights by watching those players navigate the permitting, ESG & operational steps ahead.

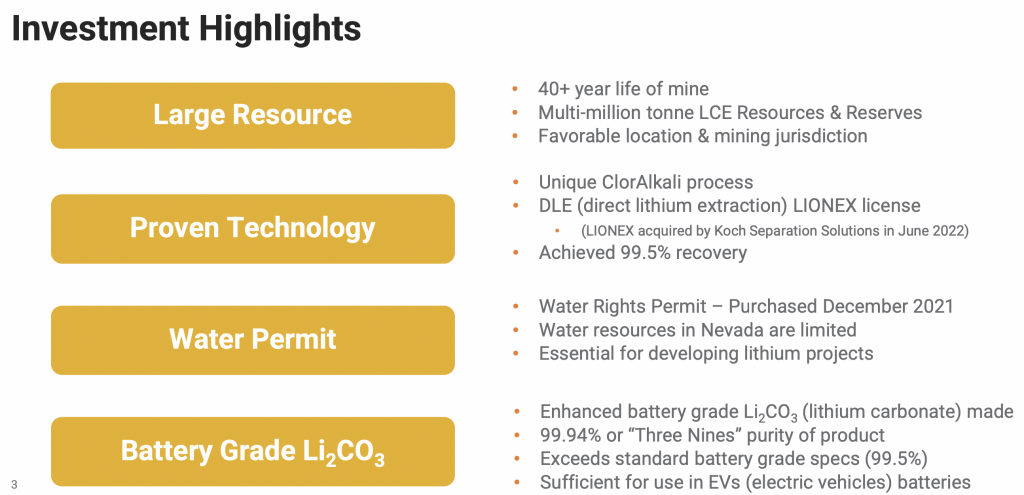

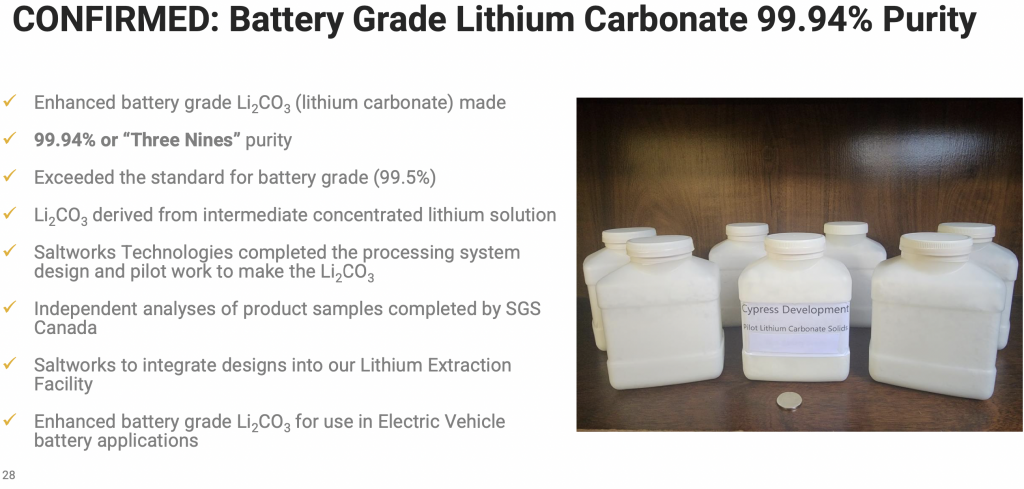

Major de-risking is right around the corner for CYP. On Sept. 19th management announced production by a third-party lab of 99.94% pure Li2CO3 from Li-bearing clay-stone from its 100%-owned Clayton Valley Lithium Project [“CVLP“].

The Li2CO3 sample was derived from concentrated Li solution produced at the Company’s pilot plant, which before long could be producing small [multiple-kg] samples for prospective customers to evaluate.

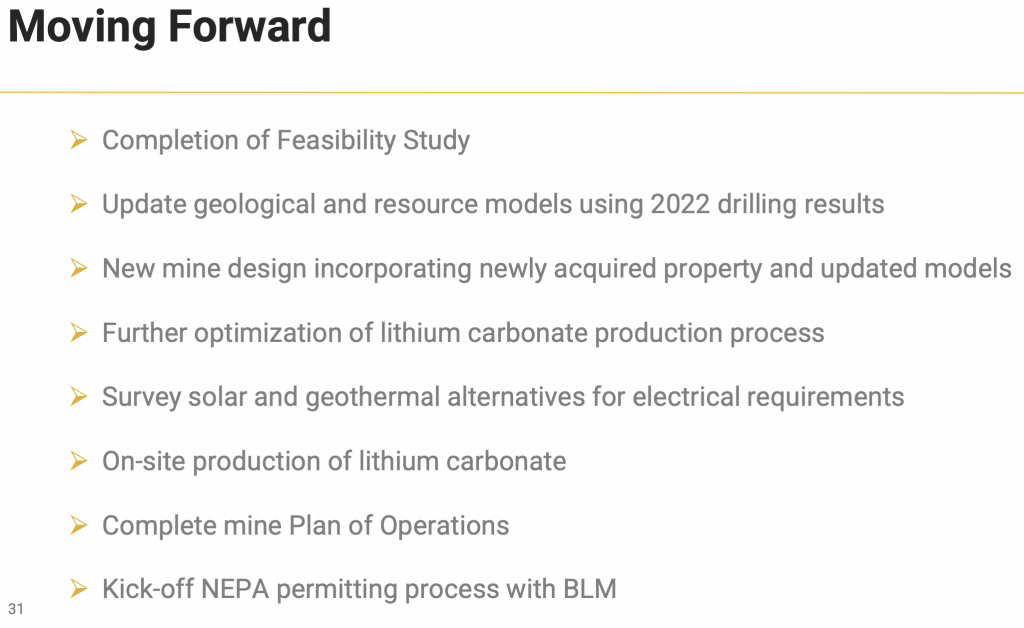

Key objectives coming up include listing on the NYSE American or NASDAQ, submitting a mine Plan of Operations to the BLM, kicking off an Environmental Impact Statement [EIS] and applying for U.S. gov’t [DoE and/or DoD] funding assistance programs.

Then, securing bankable off-take agreements & landing a strategic partner (+ lining up debt/equity funding). CYP owns 100% of the CVLP, affording it the opportunity to potentially sell a portion of the Project to help fund [its share] of cap-ex.

The Board is also working on other permitting & environmental initiatives, green power alternatives [geothermal and/or solar] pilot plant operations (studying how to lower water & acid use, recycle more water & acid, increase recoveries, reduce waste & emissions & lower power use).

I strongly believe that Li projects will have to be fast-tracked with funding [and possibly logistics / permitting assistance] from governments, OEMs, battery makers & large Li companies. Other groups that could facilitate Li project development include diversified miners like Teck & BHP & commodity trading firms.

OEMs, battery makers & Lithium companies desperately need security of supply...

I mention trading firms because Mitsui & Co., Hanwa Co., & Traxys are already investing in and/or trading Li assets, while Glencore & Trafigura have plans to enter the space.

So far we’ve seen relatively little direct investment into Li projects, or meaningful off-take agreements. That leaves dozens of parties fighting over a handful of large-scale (20k+ tonnes LCE/yr. for 20+ years) projects.

Importantly, on a recent investor call CEO Willoughby noted that subject to improvements in water, acid & power use, paths are being studied to make the project capable of delivering as much as 40 to 60k tonnes LCE/yr.

I count 7 or 8 world-class projects [held by N. American, European & ASX-listed juniors] that have not allocated production or secured a partner. That’s 7-8 non-Asian companies that could commence commercial operations by the end of 2027.

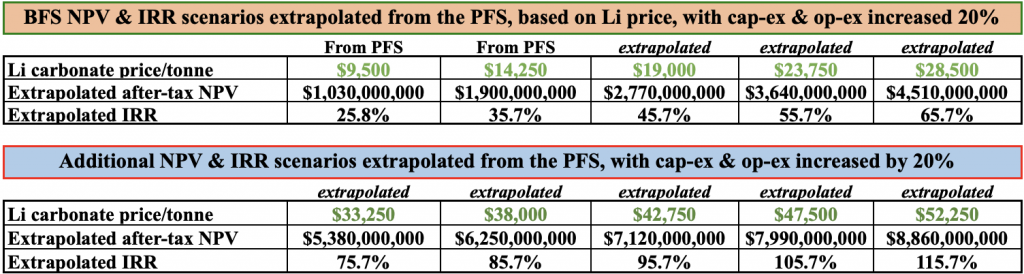

At spot Li prices, and adding 20% to both op-ex & cap-ex estimates from CYP’s CVLP PFS, the linear approximation of the after-tax NPV(8%) is roughly $15 billion for a project with an upfront capital requirement of perhaps ~$600M (PFS cap-ex figure +20%).

Assuming 1/3 of today’s spot price, the NPV would still be ~$5 billion. I recognize these are crazy numbers, but the math (extrapolated from “sensitivities” tables in the PFS, page #168) is straightforward.

Consider the annual EBITDA from 30k tonnes LCE/yr. at one-third of spot; [$71,130 / 3 = $23,710/t].

If op-ex comes in at ~$4,000/t in the upcoming BFS [PFS +20%], EBITDA at a sales price of $23,710/t would be nearly $600 million/yr.! Compare that to Cypress’ Enterprise Value [market cap + debt – cash] of ~$110M. Albemarle (ALB) is valued at an EV/2023e EBITDA multiple of 8.4x [marketscreener.com].

If ALB were to acquire Cypress for one third of its 8.4x forward EV/EBITDA multiple, 2.8 x $600M is $1.68 billion. Subtracting roughly $600M in upfront cap-ex gets us to $1.08 billion.

Discounting that figure back five years at 10%/yr. represents a valuation, [~$670M], that I believe ALB could pay and still generate a spectacular return.

So, why is CYP valued at just $108M? My guess is it’s the uncertainty regarding Li-bearing clay projects & management’s ability to bring a globally-significant project online by itself. There are concerns over the ability to raise $600M in cap-ex without too much equity dilution.

Some investors believe that since Cypress has not yet partnered up or locked in any off-take agreements, there might be red flags around the project. I disagree.

CEO Willoughby and the Board have been consistent in advancing the CVLP in a prudent & methodical manner. I don’t believe the team is actively looking for strategic partners or off-take parties until after their BFS/DFS is filed on sedar.

That’s where ALB, an OEM or a battery maker comes in. LAC’s & IONR’s projects are valued at an average EV/project (after-tax) NPV of 51%. {see chart above}. By contrast, CYP’s CVLP is valued at ~7% of its NPV.

Admittedly, Cypress is a few years behind the other two and its project is largely unfunded, but fast forward 12-24 months when Cypress has its BFS, a strategic partner & off-take agreements in hand. Will it still be valued at 7% of NPV? No!

Assuming continued achievements of critical de-risking events, access to development capital & proof of concept from Li-bearing projects by LAC, IONR & Ganfeng, Cypress should be valued at a higher percentage of the much higher NPV that will be found in the upcoming FS.

The following chart shows linear extrapolations of the PFS economics based on higher Li price assumptions and an assumed 20% escalation in both cap-ex & op-ex.

I strongly believe that many Li stocks are going to soar as the market recognizes that Li prices will remain extremely strong for 5-10 years, not just several more quarters. If true, then undervalued Cypress Development Corp. could soar even higher than peers.

Disclosures: Cypress Development Corp. is a former advertiser on Epstein Research [ER]. Peter Epstein owns shares of Cypress.