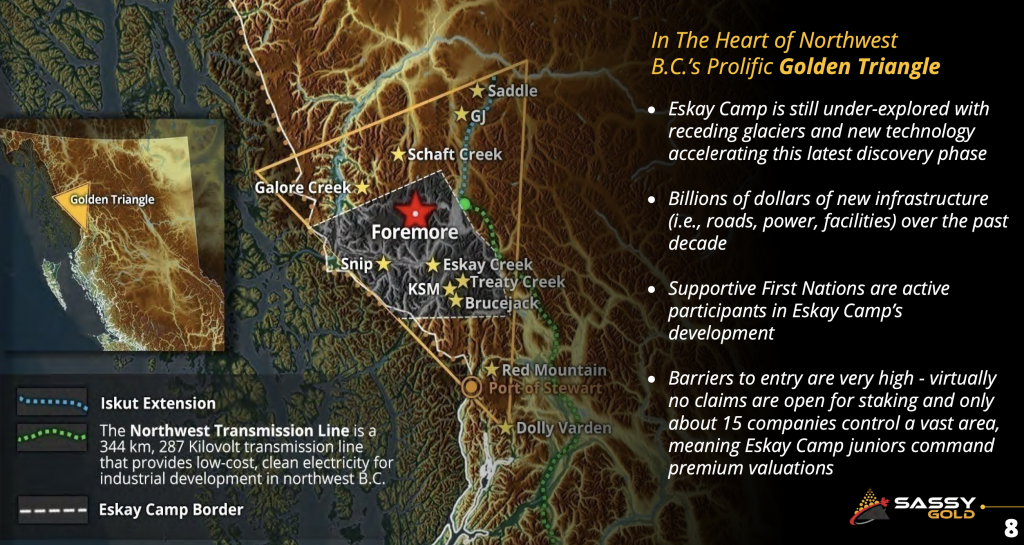

Sassy Gold (CSE: SASY) / (OTCQX: SSRRF) has a superb combination of attributes; 1] its location in the heart of the Golden Triangle nearby Skeena’s Eskay Creek, Newmont’s Galore Creek & Teck’s Schaft Creek, 2] a prime takeover target, 3] tremendous exploration upside, 4] high-grade gold, and 5] very cheap valuation.

B.C. is one of the best mining locations in N. America. It hosts companies like Newcrest, Newmont, Barrick, Teck, BHP, Agnico Eagle, Freeport McMoRan, Boliden AB, Pan American Silver (partnering with Agnico to acquire Yamana), Kinross, Seabridge & Centerra Gold.

After next year’s drilling, (if not sooner) Sassy could be of keen interest to the above-named players, not to mention Alamos, B2Gold, SSR Mining, K92 Mining, IAMGOLD, Osisko Mining, NovaGold, Coeur Mining, New Gold, Skeena Resources, Ascot Resources — I could name a dozen more.

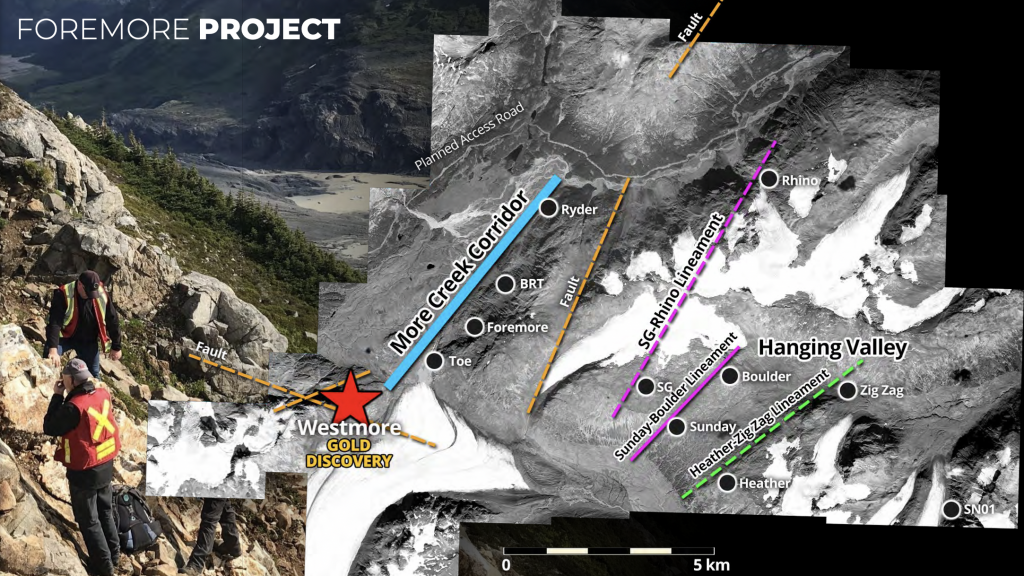

Exploration at Sassy’s 100%-owned Foremore (“FM“) project dates back 30+ years and includes prospecting, mapping, sampling, airborne & ground geophysical surveys + 71 drill holes. Mineralization is classified into three main types, VMS, Cu-Au skarn & orogenic vein.

FM is near major infrastructure incl. highways, power, labor, mining services, airstrips, an ocean port & future milling operations. Less than 20 km away, PFS-stage Galore Creek hosts ~12.5B pounds of copper + 12.8M ounces of gold.

The 14,585-hectare FM project offers three zones with significant discovery potential, most notably Westmore (“WM“), but also the More Creek Corridor (“MCC“) and Hanging Valley (“HV“) targets.

14,585 hectares is a nice-sized land package for the Golden Triangle. Tudor Gold, Ascot Resources, Dolley Varden, Benchmark Metals & Doubleview Gold have flagship projects with an average size of 16,748 ha.

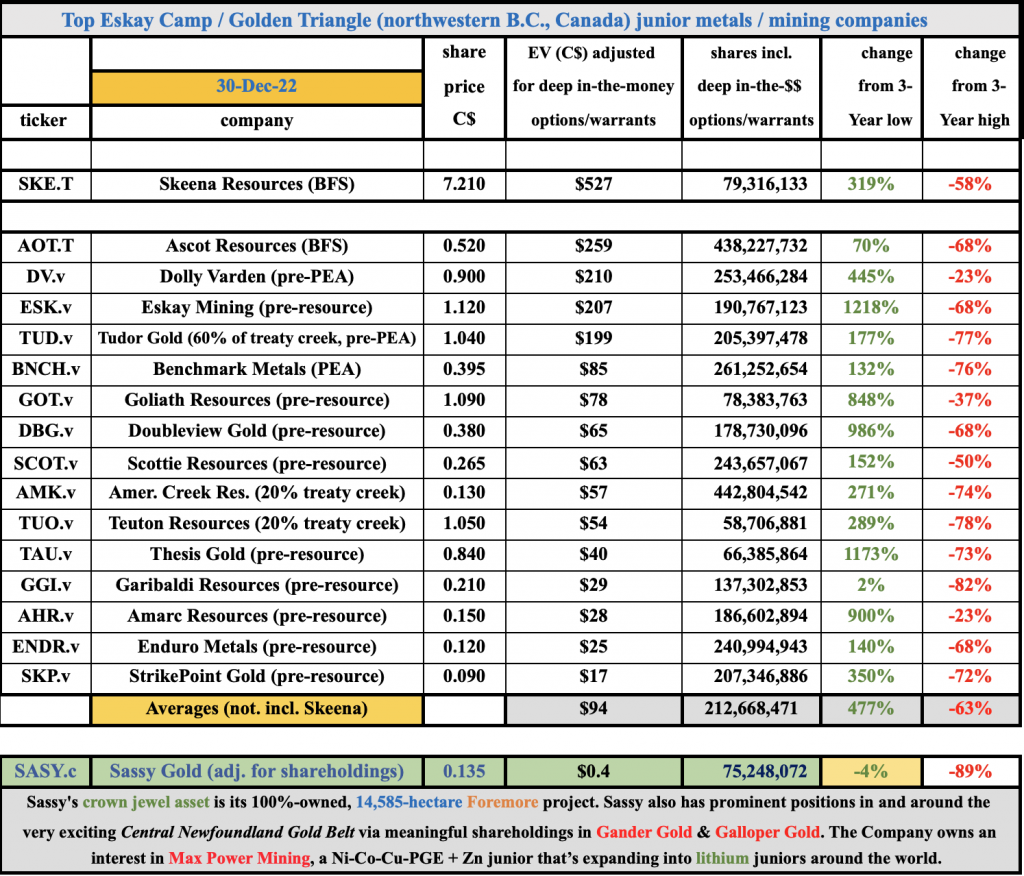

Adjusted for Sassy’s shareholdings in Gander Gold, Galloper Gold & Max Power Mining, the Company’s Enterprise Value {market cap + debt – cash} = C$1.4M. That’s right, close to zero! And, that includes a 1/3 liquidity haircut to the market values of the three portfolio positions.

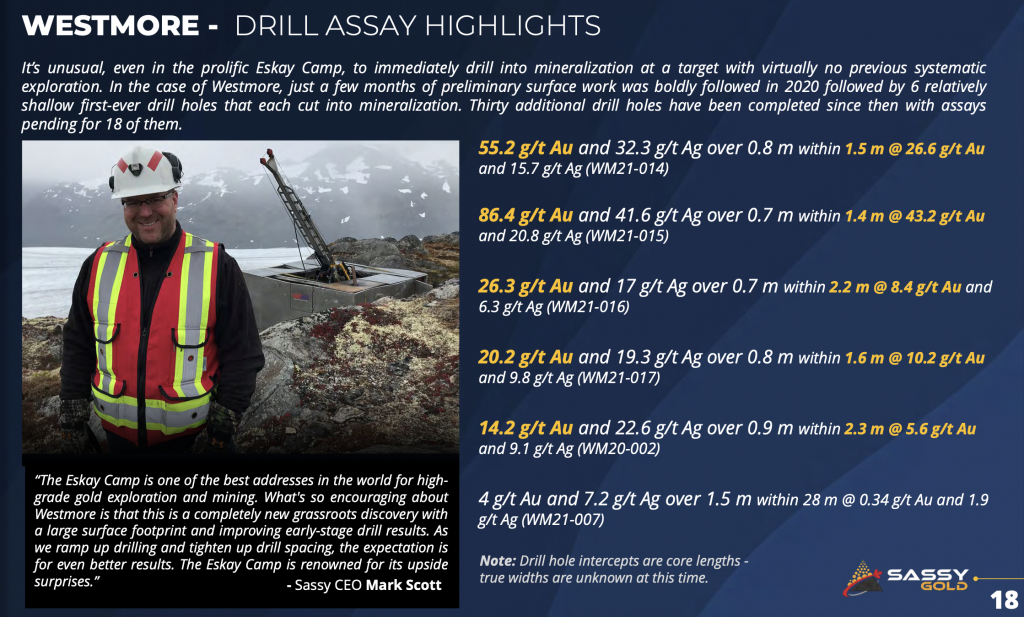

WM is the most advanced target with 36 drill holes into it and assays from 18 holes pending. In 2020-21, the top-50 of 1,026 surface samples averaged ~47 g/t Au Equiv. (includes silver).

This past Summer’s drill program focused on the 4-Amigos vein (named after four rock stars on Sassy’s technical team), with 160 m of strike length exposed and open to depth & along strike.

Examples from the 4-Amigos vein include,

Multiple vein structures have been mapped covering an area of at least 1,000 sq. meters and > 400 m deep. Receding ice & snow is revealing growing evidence, subject to further drilling, of a meaningful orogenic gold deposit.

As can be seen in the chart above, Sassy has real potential to be re-rated higher. I believe strong drill results and/or a higher gold price in 2023 could add C$10’s of millions to Sassy’s valuation.

Readers should note that Sassy shares were as much as 3.5x higher, peaking at C$0.48 about six months ago (vs. C$0.135 Dec. 30th). When Sassy hit that high level on July 20th, gold was at US$1,696/oz. vs. ~US$1,845/oz. now!

Today’s valuation could offer an attractive entry point for risk-tolerant investors.

Sassy has 36 drill holes under its belt at WM, ~8,000 m of drilling, revealing what appears to be a structurally controlled, gold-rich system with multiple vein structures.

High-grade, vein-hosted gold-silver mineralization — in combination with zones of precious metal-enriched base metals — span a distance of 7 km along the northeast-trending MCC, beginning immediately north of WM.

The MCC is at least 5 km long, but has had very limited drilling. One hole delivered an attractive 8.0 m of 4.35 g/t gold. A thinner interval (0.8 m) returned 26.5 g/t Au, 8.6% Zn + 2.2% Cu.

The HV target is on the eastern side of FM, defined by multiple precious & base metal showings across multiple mineralization styles. Very limited mapping, sampling or historic drilling has been done. Select surface samples include; 48.8, 36.4, 24.6 & 20.9 g/t Au.

Two km north of the Boulder target, grab samples assayed a combined 19.7% Zn + Pb, while a 21.4% Cu sample was collected 2 km south of Boulder at the Heather showing.

Let’s take a closer look at Gander Gold, of which Sassy owns ~35.3 million shares. Gander is laser-focused on the exciting province of Newfoundland & Labrador.

At 226,300 hectares, Gander is a Top-6 gold claims holder on the Island. Importantly, ~3/4’s (176,300 ha) are contained in three claims blocks; Mt. Peyton, Gander North & BLT.

Mt. Peyton’s land package alone is larger than most other juniors’ entire footprints. Not just a giant contiguous land package, but in a strategically important location near New Found Gold’s world-class deposits.

Regarding Gander North, the western edge of this large block straddles the famous GRUB Line. Historical exploration at Gander North has returned, “very high gold-in-till anomalies.”

Finally, BLT sits on the same fault system that hosts Marathon Gold’s 5.1M oz. advanced-stage Valentine Gold project.

Sassy’ has an investment in Galloper Gold, a well-funded private B.C.-registered junior gold company, also in Newfoundland, with 213,500 hectares, including strategic claims near New Found Gold’s Queensway Project.

Galloper plans to list on a Canadian exchange in 1H 2023. Sassy holds eight million shares.

Sassy’s 3rd portfolio holding is five million shares in Max Power Mining, owner of the promising Nickel-Copper-Cobalt-PGE Nicobat Project in Northwestern Ontario. Importantly, the nickel price is up nearly 65% in the past six months.

Max’s share price has outperformed most juniors in part due to it being in advanced discussions to acquire some (as yet announced) lithium properties.

As I write this sentence on January 3rd the combined value of Sassy’s holdings in Gander, Galloper & Max Power = C$11.6M. Given the realities of trading junior miners, I take a “liquidity haircut” to that figure, so call it C$7.7M (a 1/3 haircut). That pegs Sassy’s (adjusted) EV at ~C$1.4M.

Management has an option to acquire 100% of the drill-ready Highrock uranium project near the world-famous Athabasca basin in Saskatchewan, south of Cameco’s past-producing (1983-1997) Key Lake mine, which extracted > 200M open-pit pounds at an average grade of 2.3% U3O8.

In addition to the considerable value of Sassy’s three portfolio holdings, the Highrock project is arguably worth several million dollars and can be explored year-round.

Admittedly a lot’s riding on drill results from WM this quarter, but with the Company’s EV near zero and potential upside from meaningful share holdings in Gander Gold, Max Power, Galloper Gold — and the Highrock uranium project — company-wide risk/reward seems quite compelling.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Sassy Gold, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Sassy Gold are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Sassy Gold was an advertiser on [ER] and Peter Epstein owned shares & warrants in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.