Is this an epic buying opportunity for Colonial Coal (TSX-v: CAD) / (OTCQX: CCARF), or are shareholders going to be bagholders for another year or two?

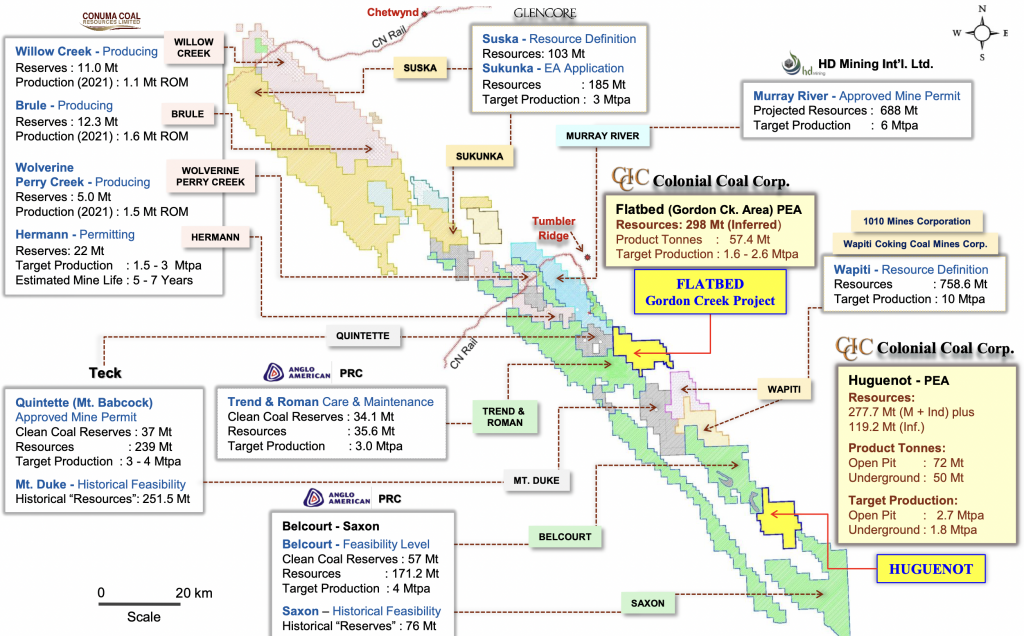

Colonial is a steel-making [coking or metallurgical (met) coal] development company with two 100%-owned projects in one of the world’s premier coking coal regions, the Peace River Coalfield (“PRC“) of B.C. Canada.

Both projects have Preliminary Economic Assessments (“PEAs“) on them. There’s a combined 695 million metric tonnes (“mt“) of high-quality (hard coking coal & PCI) Measured + Indicated & inferred resources (not reserves). {see risk factors at bottom of article}.

The projects have been for sale via an investment bank process since 1H 2019. Management maintains that COVID-19 has been a major contributor to the slowness in finding buyers. I believe them.

However, some question the ability of a buyer to get permits, maintain strong First Nation relations, fund regional infrastructure buildouts, etc. Others fear that geopolitics will prevent the Chinese, or companies from other countries, from bidding.

A prominent concern; will “green” hydrogen replace the need for coking coal in the blast furnace phase of the steelmaking process.

NOTE: {Hydrogen’s use in steelmaking remains at pilot scale. It would take a long time to switch to hydrogen on ~1.3 billion tonnes/yr. of blast furnace-derived steel. Also, leakage of hydrogen from exploration, transport, storage & end-use is a serious, unresolved issue}.

If/when demand for seaborne coking coal starts to wane, the best quality coals, (like those from the PRC basin), will be the last to go as they burn cleaner & more efficiently.

For several logistical & transportation-related reasons, high-quality seaborne coking coals will remain in demand longer than other coals. Virtually all of the growth in blast furnace demand is coming via the seaborne market, mostly into Asia from Canada, Australia & the U.S.

Please continue reading — 10 reasons to care about coking coal, and especially Colonial Coal.

#10 — Consuming coking coal is a necessary evil. There are no medium-term substitutes that can be deployed on a widespread basis, at a reasonable cost.

After decades of trying to reduce the use of coking coal, centuries-old blast furnaces account for more than two-thirds of global steel production.

#9 — Colonial’s valuation is quite attractive. Investors have been waiting years for the Company’s projects to be sold, and investor fatigue has set in.

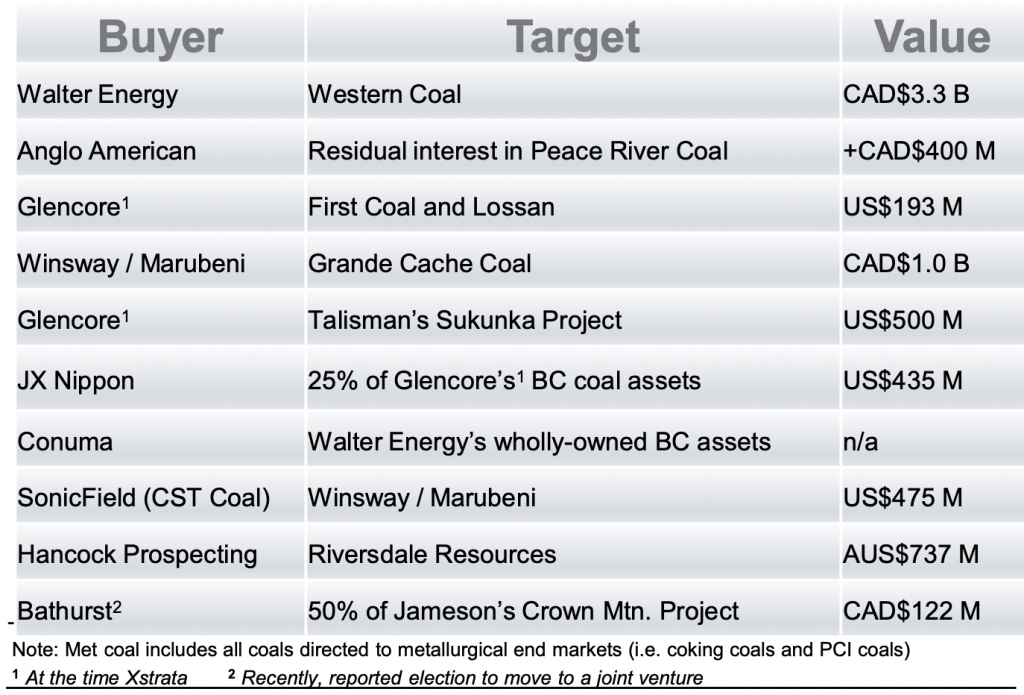

On an EV/resource tonne in the ground basis, Colonial is valued at just US$0.30/tonne. This compares to historical M&A deals done at US$2.00+/t.

Inflation this year is the highest since the early 1980s, AND coking coal prices are as strong as they were for most of the previous bull market in 2010-11. These two factors support the potential for a robust EV/tonne valuation.

Chatters on CEO.ca {a Canadian stock dashboard/online community} debate the takeover price, saying it should be US$2-$3+/mt, but even US$1.00/mt would be a very large premium over the current price of C$1.65/shr. {Mar. 27th}.

At US$1.00/t, I think there would be several eager bidders if only to keep the assets out of the hands of competitors. For instance, Teck Resources, Anglo American, Glencore & privately-held Conuma Coal should care as they all have projects and/or existing mines surrounding Colonial.

#8 — Dozens of financially strong companies — mostly steel & coal companies from the U.S., India, China, Brazil, Canada, Korea, Japan & Australia — with valuations well into the US$10’s of billions — can afford to buy Colonial’s assets AND fund development to lock-in decades of low-cost supply.

Importantly, potential bidders have dramatically cut debt levels and improved their finances. For example, Teck Resources’ net debt / EBITDA ratio on a trailing 12-month basis is <1.0x, and Steelmaker ArcelorMittal’s leverage is <0.5x.

Australian coal producer Whitehaven Resources is expected to generate a total of C$7.85 billion in EBITDA in 2022-2023, slightly less than its Enterprise Value (“EV“) {market cap + debt – cash} of C$8.3 billion.

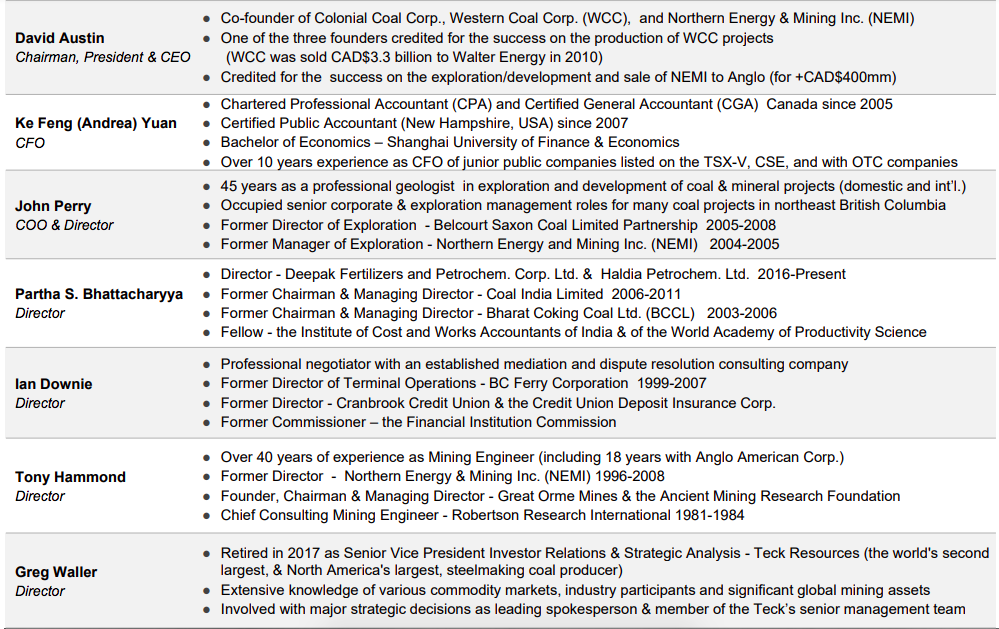

#7 — Strong management team, board & advisors. Not only do senior execs & advisors have coal & steel industry expertise and an operations background, but they have also been active in coking coal M&A. The team has strong contacts in China, India, the U.S. & Australia, and ties with (at least) Anglo, Teck & Glencore.

CEO/Chairman David Austin sold both Western Coal & NEMI at the top of the market in 2010-11. Yet coking coal fundamentals today appear just as strong. Mr. Austin has stated that there are over ten active NDAs in place.

#6 — Coking coal is a tangible, hard asset. Real assets, especially critically important industrial commodities, offer inflation protection. Metals & Mining companies often outperform in inflationary environments and in periods when value investing becomes favored over growth.

#5 — Unlike producing coal companies, Colonial is NOT saddled with; debt, legacy liabilities, elevated pension/healthcare obligations, high reclamation costs, etc. An acquirer of Colonial’s assets should be able to avoid — or better manage — coal-specific issues that existing producers are stuck with.

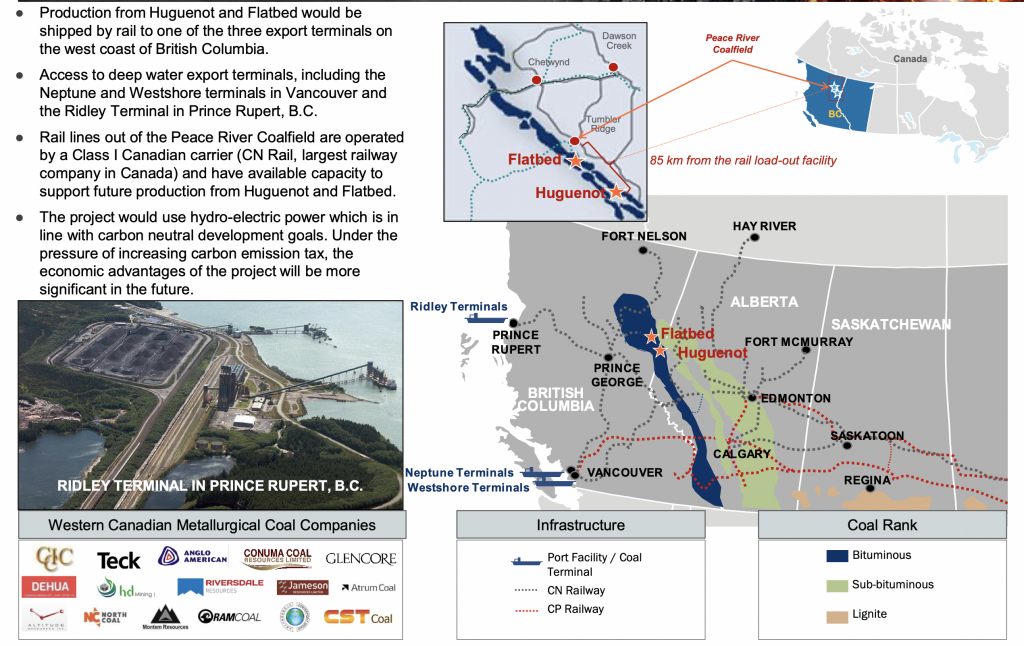

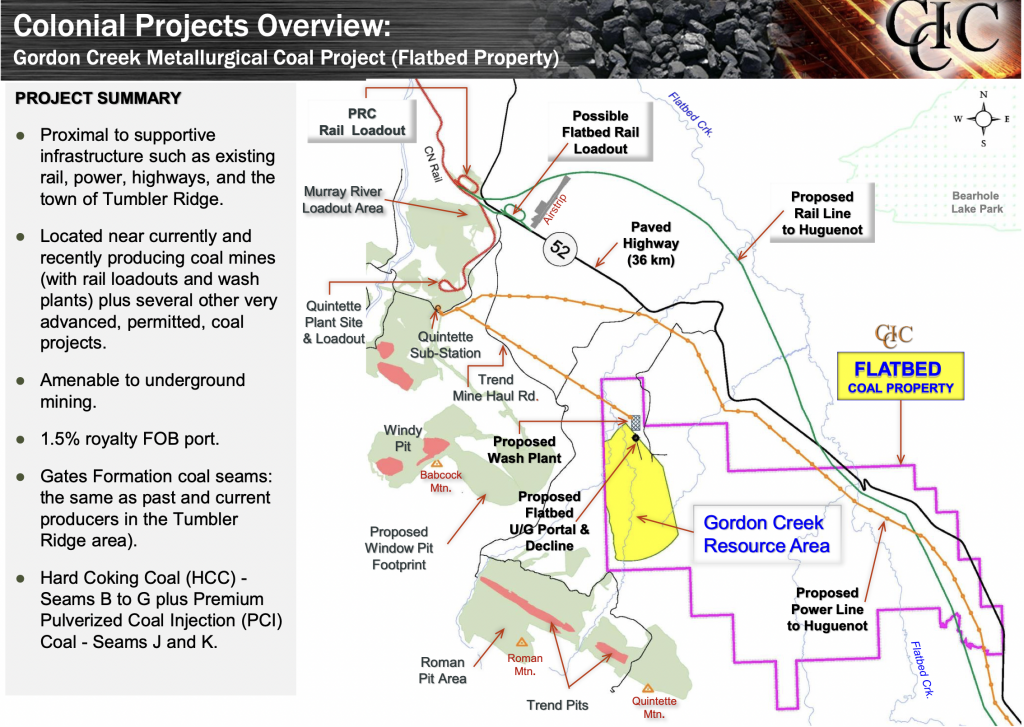

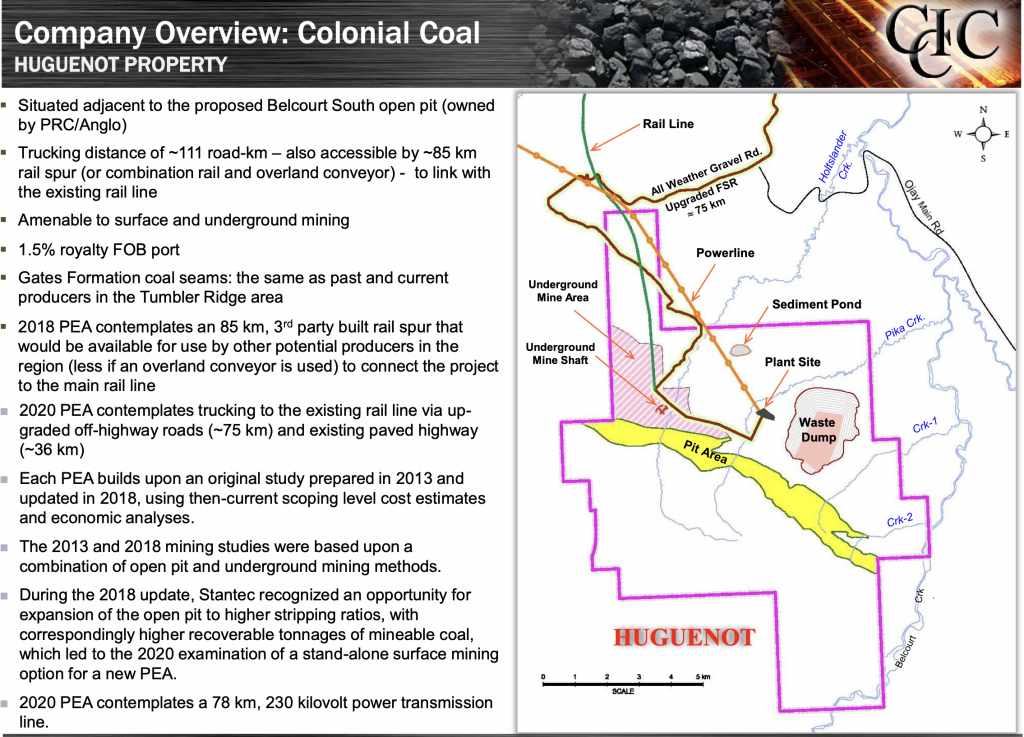

#4 — Location, location, location. There’s ample regional infrastructure [power, water, rail, roads, west coast ports]. Some infrastructure buildouts will be necessary, but not a huge deal in the overall picture.

Moreover, an acquirer of Colonial’s assets will be able to partner with producers & developers to advance regional infrastructure. Importantly, CEO Austin has agreed to remain involved post-sale to help commercialize the projects.

The PRC is one of the two best coking coal basins on the planet. Only Australia’s Bowen Basin is as good or better. Colonial’s projects are surrounded by Teck, Anglo, Glencore & Conuma.

Conuma could more than double its 4 million tonne/yr. operating rate by acquiring Colonial’s two projects. As of 2020, Conuma’s three mines + one project had a combined 50 million tonnes of proven & probable reserves.

#3 — Colonial’s projects totaling 695 million Measured + Indicated & Inferred tonnes of resources (not reserves) represent a globally-significant endowment. The specs in the PRC region are well understood. PRC coking coal has been shipped to Asia, most notably Japan, for half a century.

#2 — Significant global supply concerns. Russian production of seaborne coking coal will be in decline due to a lack of growth & maintenance capital investment.

Increases in Australian supply is at risk from ongoing weather challenges [climate change], labor shortages, ESG concerns & uncertainty over Chinese/Australian relations.

The U.S. shares some of Australia’s supply challenges (+ railway bottlenecks) and is viewed as a swing producer. Given very high thermal prices due in large part to Russia’s war on Ukraine, a portion of U.S. coking coals are crossing over to the thermal market.

Clearly, Asian blast furnace operators would benefit from locking in security of supply (and a very low long-term price) by diversifying across as many reliable, long-term sources as possible.

#1 — The economics of Colonial’s projects, as seen in their PEAs, has greatly improved with the substantial increase in coking coal prices from US$160-174/(C$209-$224)/mt in the studies [2010-11], to significantly higher levels today.

By my rough calculations, the combined after-tax NPVs are > C$4 billion on higher prices, even allowing for meaningful increases in op-ex & upfront cap-ex.

A buyer at US$1.50/t would be investing a total (including cap-ex) of < C$3 billion spread over the next several years to own over C$4 billion in today’s (after-tax) NPV(5%).

RISK FACTORS — Viable coking coal substitutes like green hydrogen could become available at large-scale & reasonable cost sooner than expected. Perceived permitting/environmental hurdles & geopolitical challenges could preempt bids from key prospective buyers. Currently, solid First Nation relationships could diminish. The fact that it’s been > 3.5 years without a reasonable bid means there could certainly be red flags that I’m missing.

CEO Austin and/or his team, advisors/bankers could be overly optimistic [groupthink] on the prospects of selling Colonial’s projects. Colonial stock could be halted for weeks at a time if/when bid(s) come in. Coking coal prices could fall back under US$175/t for an extended period. Trading liquidity in Colonial’s shares is very poor. Even after material delays, the sale or one or both projects could still take many more months. The Company has ~12 months of cash before needing to raise a few million dollars.

Although not currently or formerly a client, Mr. Epstein is pursuing Colonial Coal to become an advertising client on Epstein Research. Mr. Epstein owns shares in Colonial Coal. Both of these factors make Mr. Epstein biased in favor of Colonial Coal.