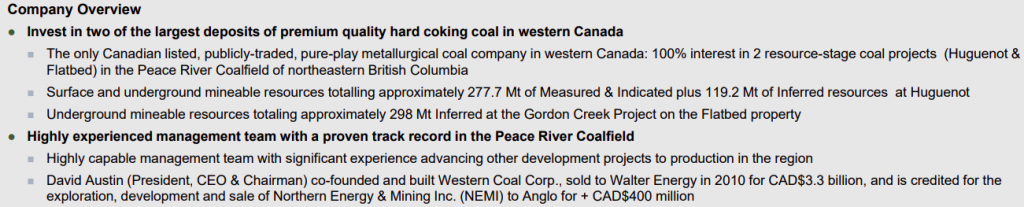

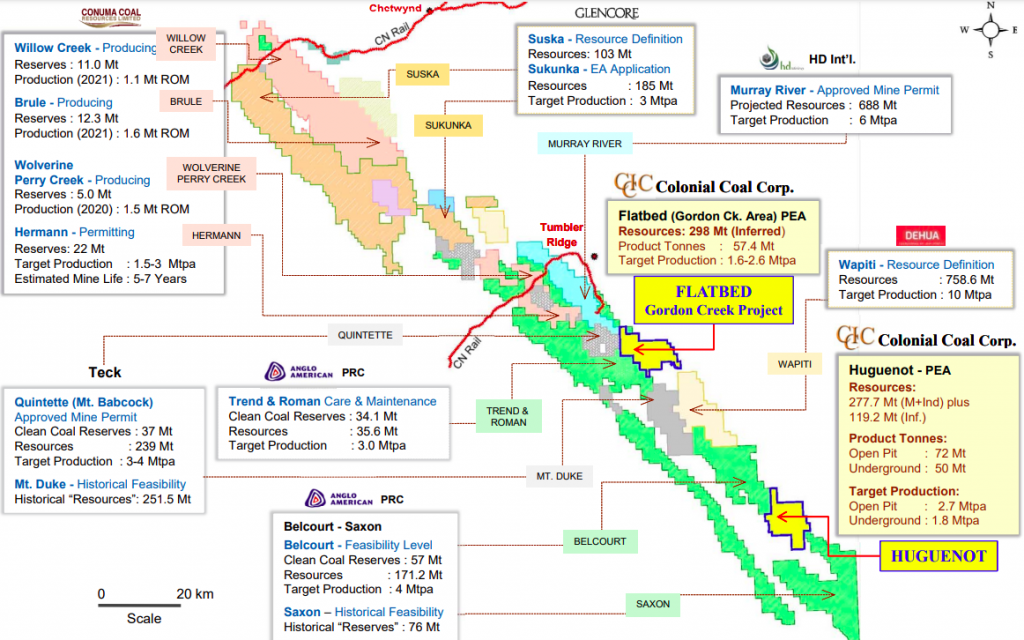

Colonial Coal Intl. Corp. (TSX-V: CAD) / (OTCQB: CCARF) is a coking/metallurgical (met) coal company with two 100%-owned projects, each with Preliminary Economic Assessments (“PEAs”) on them. Both have been up for sale for nearly four years. Colonial’s projects are in B.C. Canada’s Peace River Coalfield (“PRC”).

Huguenot sits between Anglo American’s Belcourt & Saxon projects. Flatbed is adjacent to Anglo’s Trend mine (on care & maint.) & Teck Resources’ proposed Window mine (Quintette); also near Conuma’s operating Perry Creek and proposed Hermann mines (Wolverine) + HD Mining’s Murray River underground project.

Several public & private coal companies/projects in the PRC are in development. The buyer(s) of Colonial’s projects could share rail spur, powerline & road infrastructure costs with third-party developers. What has changed in the past several months and why the frustrating lack of results from the multi-year sales process?

It’s impossible to say why this is taking so long. However, I believe management when they say COVID-19 has slowed things to a crawl several times over the past few years.

Whenever China, India, the U.S. or Canada is sidelined, Colonial’s team steps back (somewhat) from the process. It’s hard to extract a premium valuation when key bidders, investment bankers, lawyers, financial advisors, etc. are absent.

Another factor has been Colonial’s seeming lack of urgency. Having cash in the bank, and no debt or near-term deadlines enables management to hold out for a stronger outcome.

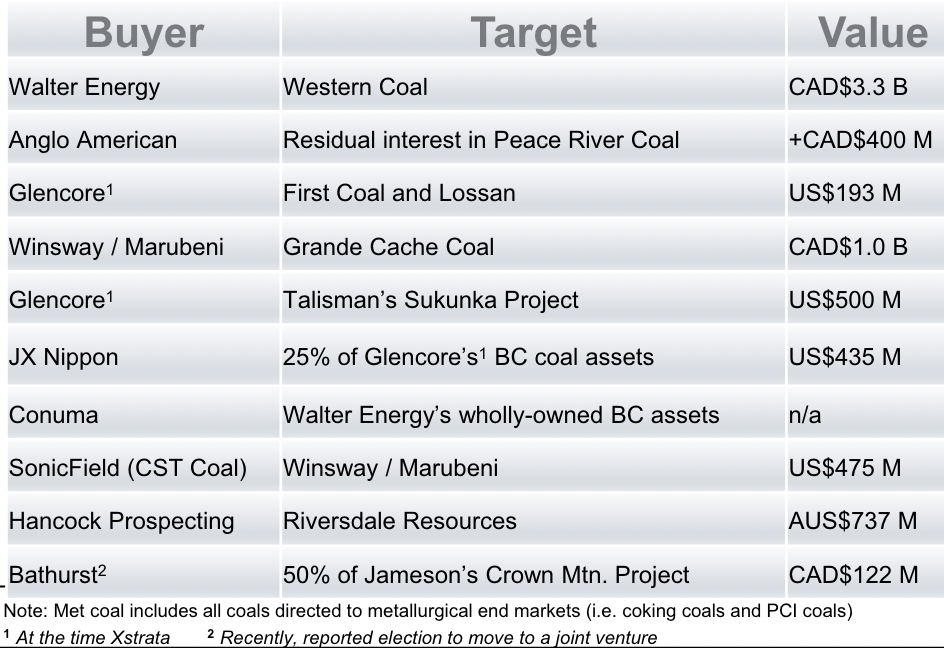

In the last M&A cycle of 2010-11, coking coal in the ground traded at ~US$2.0/Mt. Today, adjusted for inflation, that would be ~US$2.75/Mt. Moreover, inflation this year is > twice the 3.2% rate for 2011. Hard assets like industrial commodities can offer a compelling hedge in inflationary periods.

Another thing that’s twice as high vs. a decade ago? Coking coal prices! Given inflation, all-time high coal prices, and ever-growing global steel demand — some shareholders are hoping for US$3.0+/Mt.

CEO David Austin’s team is fighting for every US$0.25/Mt, equal to ~C$1.16/share. The current share price implies the Company’s 695 million Mt are worth just US$0.45 each. Even at US$1.50/Mt, the implied share price would be ~3x higher.

Readers are reminded that selling the projects at US$2.00+/Mt is far from a sure thing. India is (kind of) backing Russia’s war on Ukraine, making an acquisition by an Indian group less likely, but not impossible.

Still, countries with large steel and/or coal companies that remain in good standing with Canada include; the U.S., Australia, Korea, Japan, S. Africa, Germany & Brazil.

As long as coking coal prices remain strong and we avoid a global recession, I don’t see Colonial’s assets transacting at < US$1.50/Mt. If there is a recession, that could slow the sale process [yet again!], but I believe management would hold out for US$1.50/Mt. And, at that valuation, I think Anglo or Teck might step in as a backstop bid.

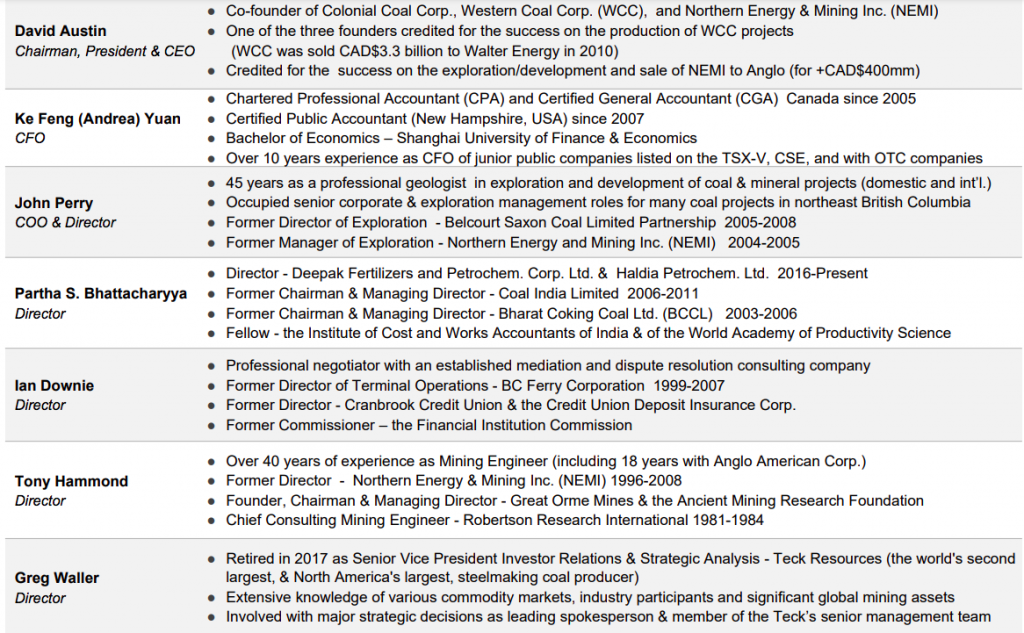

Betting against this team may prove to be a mistake. In addition to Mr. Austin, there are several other impressive coal & mining experts. COO & Dir. John Perry has 45 years’ experience in coal & mining projects, incl. senior roles in northeastern B.C. coal projects.

Dir. Partha Bhattacharyya is a former Chairman & MD at Coal India & (prior) Bharat Coking Coal. There aren’t many bigger jobs than Chairman at Coal India, the largest coal company on the planet. Partha has contacts in most of India’s largest coal & steelmaking companies.

Dir. Ian Downie is a professional negotiator & mediation/dispute expert. He was a former Dir. of Terminal Operations for BC Ferry Corp. Dir. Tony Hammond has > 40 years’ experience as a Mine Engineer, incl. 18 years at Anglo American + 12 years as a Dir. at Northern Energy & Mining (NEMI).

Dir. Greg Waller retired as SVP of IR at Teck, N. America’s largest coking coal producer. In that role, and after 33 years at Teck, Greg is very well-versed in key aspects of that company’s steelmaking coal division.

From time to time I speak with Mr. Austin and a few prominent shareholders. One thing I’m confident about is that no one knows WHEN a bid might surface, but all believe bids are coming. Why do they remain optimistic after years of waiting?

First, the list of actively interested parties is said to be strong, I’m guessing 8-10 groups. All we need is 2-3 parties for a bidding war.

Second, coking coal prices are strong, the past year’s ATH (> US$650/Mt) is twice the last cycle’s high and well more than double the level at the time the sales process began in 2019.

Third, there’s only a handful of world-class, large, seaborne-accessible coking coal assets in well-established, safe mining jurisdictions. Energy (thermal) coal is found everywhere, but high-quality hard coking coals are almost exclusively in Canada, Australia & the U.S.

Fourth, the financial strength of publicly-listed groups contemplating bids has improved, in some cases dramatically.

In prior articles, I speculated that global steelmakers have great interest in Colonial’s projects, even if just to keep them out of the hands of competitors. In this update, I suggest that coking coal producers might be even more compelled to act.

Coking coal companies should be more inclined to acquire new supply because if one or more steelmakers gain control of Colonial’s assets, they would no longer need as much (or any) third-party coal.

And, if a steelmaker buys Colonial’s projects, other steelmakers might look to follow that strategy. Therefore, coking coal producers risk losing their best customers to vertical integration.

Coal producers outside of China & India that are large enough to bid for Colonial’s assets include Sasol Ltd., Yancoal Australia, Exxaro Resources, Peabody Energy, private Peace River Coalfield producer Conuma Coal, private Australian producer Hancock Prospecting & Whitehaven Coal.

In addition, two or three smaller companies like Alpha Metallurgical Resources, Coronado, Arch, Alliance Resource Partners, Consol Energy, New Hope & Warrior Met Coal could team up to bid.

There could be other companies in the hunt; mining giants (Teck, BHP, Anglo), iron ore players (Vale, Rio Tinto, Fortescue Metals) & commodity-trading firms (Glencore, Vitol, Itochu, Mitsubishi, Mitsui).

Steelmakers highly reliant on premium (seaborne) coking coal are increasingly anxious to obtain security of supply. Some are more concerned with being able to get coal at all, than about the price paid.

Some readers have asked how long before production might start on Colonial’s two projects, are they permitted, when will resources be upgraded to reserves, etc.

Colonial delivered PEAs on both of its projects and then largely stopped advancing them. Management believes the greatest bang-for-the-buck comes from developing globally-significant projects to PEA-stage. Why is that?

For coking coals in world-class basins like B.C.’s PRC, production dates back > 50 years. The resources that Colonial is trying to monetize are well understood by end-users. Still, most acquirers will perform their own Pre-Feasibility & Bank-Feasibility studies geared specifically to their needs.

About permitting & environmental risk factors, these will be borne by the buyer(s). So far, a substantial amount of due diligence — by several groups — over several years, has failed to turn up any meaningful red flags that I’m aware of.

Trading liquidity is low, (~100k shares/day) making it an ideal opportunity for retail investors to take advantage of. Not many companies have as much upside potential as Colonial Coal Intl. Corp. (TSX-V: CAD) / (OTCQX: CCARF), with what I believe to be only modest fundamental downside.

Disclaimers/Disclosures: Peter Epstein of Epstein Research [ER] has no current or prior relationship with any management team or board member, and no current or prior dealings with Colonial Coal the Company. This is the third article written by [ER] on Colonial Coal. The views contained herein are solely those of [ER] and are based 100% on publicly available information such as sedar filings, and Colonial’s new corp. presentation, conversations with shareholders & peer company analysis. Teck Resources shares a considerable amount of data on the coking coal market in its corp. presentations, data that [ER] incorporates into its articles. Since September 2021, Peter Epstein has owned shares of Colonial Coal acquired in the open market.

Mr. Epstein is pursuing Colonial Coal as an advertising client and should be considered biased in favor of the Company.

Although [ER] is very bullish on the prospects of Colonial Coal, it’s possible that [ER] is wrong about the Company in one or more of several key respects. [ER] could be wrong about environmental or permitting challenges. Some prospective bidders might have concluded that Colonial’s projects would be too difficult to get into production. [ER] could be wrong about the ongoing strong demand for coking coal in blast furnaces. [ER] could be wrong in its view that coking coal prices will remain stronger for longer. If prices were to fall by a substantial amount in the coming months, that could negatively impact the valuation of Colonial’s projects.