I recently spoke to a big-shot hedge fund manager who told me investment banks will soon be updating 2025 targets on gold (“Au”) & silver (“Ag”). She assured me none are lowering their estimates…

Where are we in this bull market? Some believe we’re still in inning 2 or 3, others 5 or 6, but no one thinks we’re in inning 8 or 9. Look at this 12-year chart, $2,760/oz. is 8% below $3,000!

An Au junior (with an Ag kicker) that I like is Tocvan Ventures (CSE: TOC) / (OTCQB: TCVNF). It has done well this year, but nothing like the top decile performers who are up on average of > 400%.

The difference between many of the top 10% names and Tocvan is that it has not yet delivered big news. I say “yet,” because I think big news is coming, like securing a strategic partner to (possibly) get free-carried for several years at its Gran Pilar project. That would keep shares outstanding at a very low level.

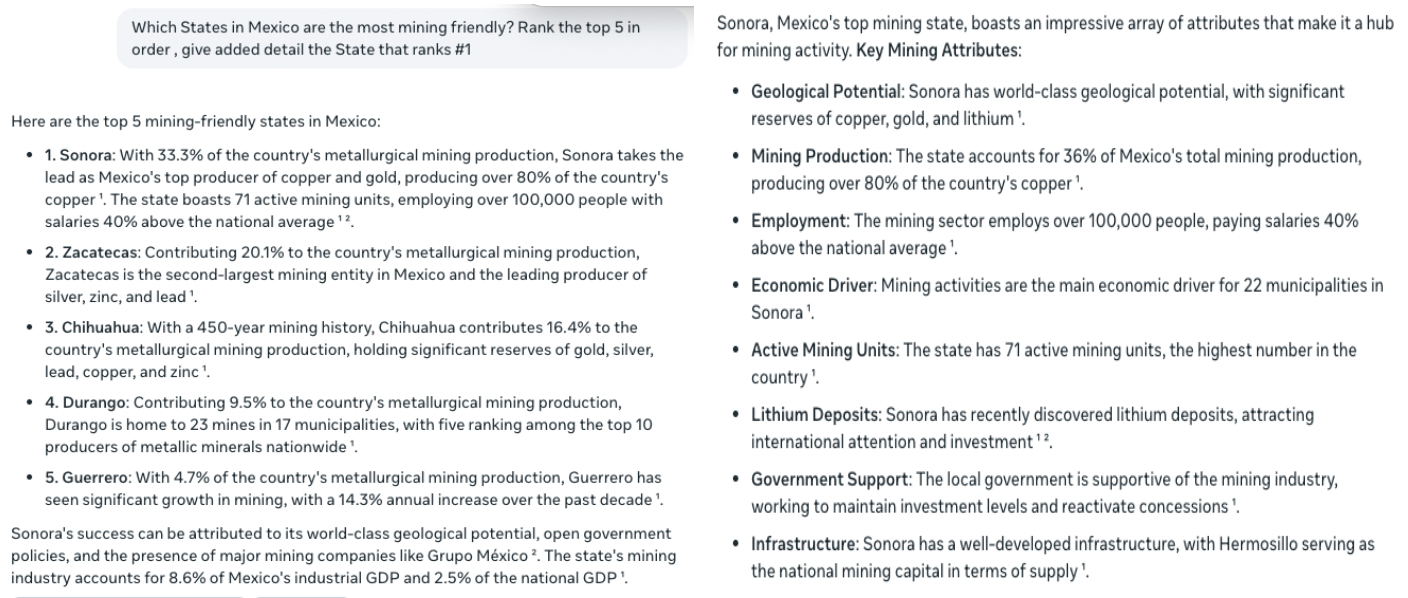

Other big news could be lots of high-grade assays (results pending on > 700 surface samples, and counting) or strong drill results in the next phase of drilling starting in November. Make no mistake, this is a risky story, but the upside potential is substantial. Tocvan’s assets are in Sonora, ranked #1 mining-friendly State in Mexico by Meta.ai, Chatgpt & Gemini.

Rankings #2-5 change across AI platforms, but Sonora is always #1. Sonora has excellent mining infrastructure, (roads, power, water, skilled workforce, mining services & equipment). Below is the Meta.ai commentary.

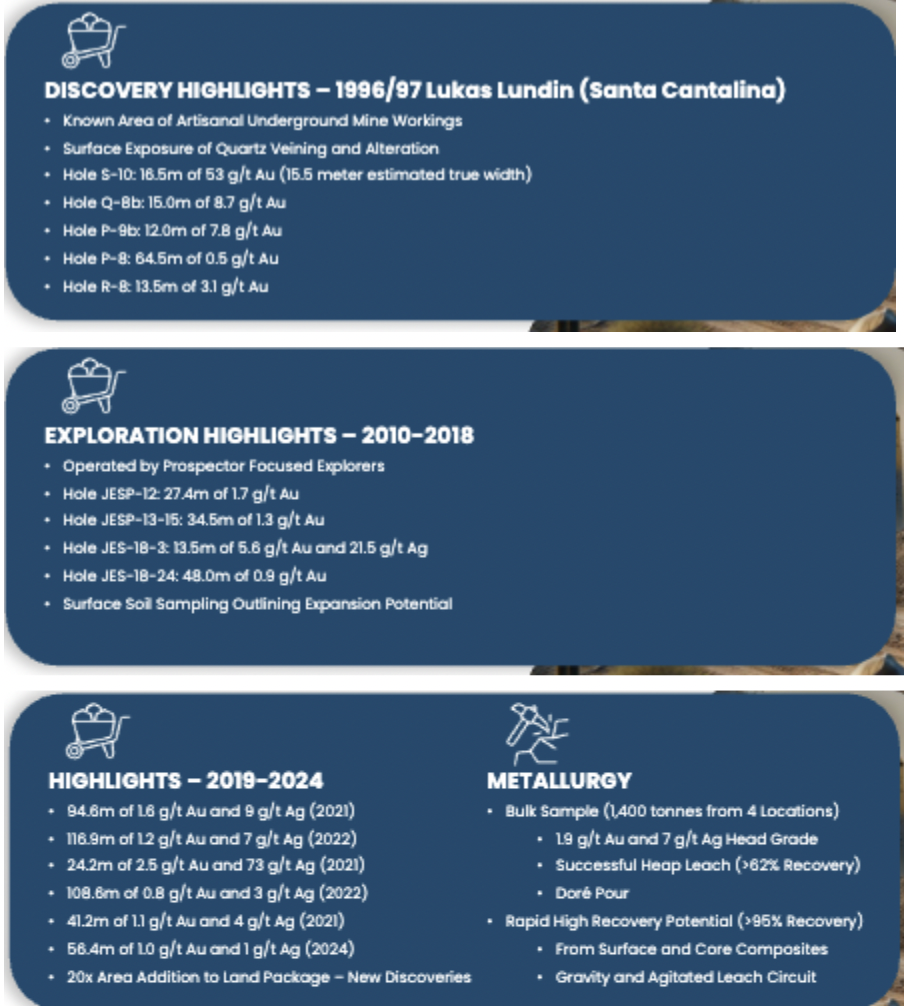

Tocvan has two main projects, the most important being Gran Pilar, the subject of two historical exploration programs. Both included significant surface exploration + reverse circulation (RC) drilling.

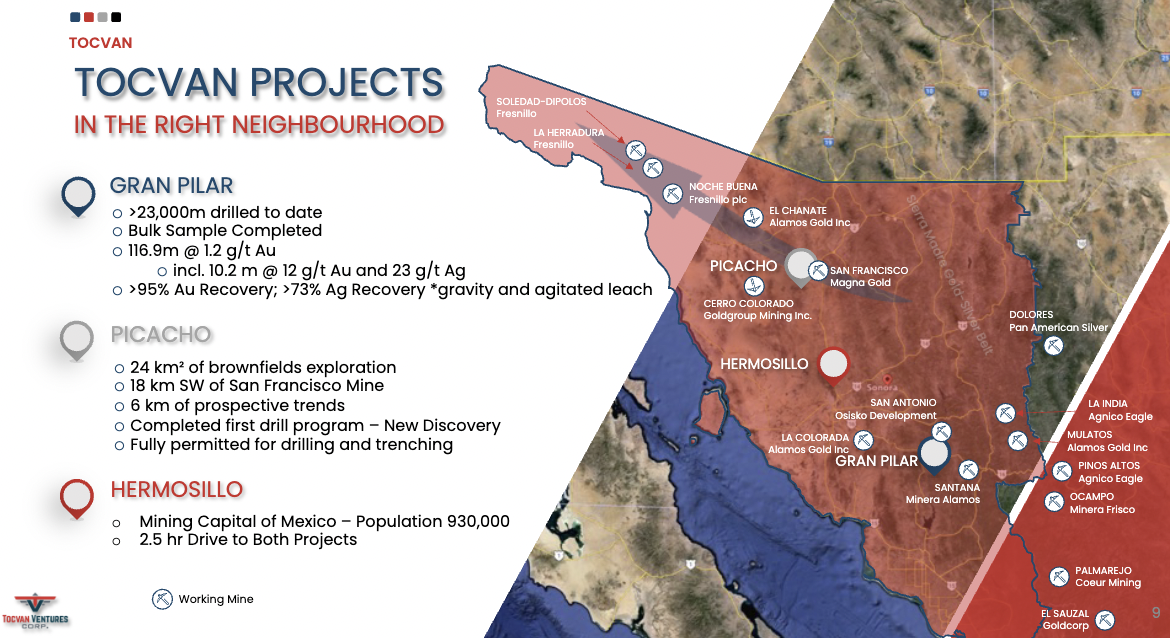

Given the many mines & projects surrounding Gran Pilar, and the fairly extensive historical work done to date, management is optimistic a sizable resource can be delineated. A large regional producer seemingly agrees. It’s in discussions with management after six months of onsite + offsite due diligence.

Producers including Grupo Mexico, Newmont, Industrias Penoles, BHP, Agnico Eagle, Fresnillo plc, Franco-Nevada, Alamos Gold, Equinox Gold, Coeur Mining, Fortuna Mining, Orla Mining, Minera Alamos & Minera Frisco have assets in Sonora or elsewhere in Mexico and could be interested in partnering with Tocvan.

Decades of history on Gran Pilar coming to fruition in the 2020s!

These players are attracted to low-technical risk, low-cap-ex projects that can reach production this decade. Tocvan traded as high as $1.67 in mid-2021, a year in which Au averaged $1,798/oz. Today’s share price of $0.59 is 64% lower, despite Au being +53% higher!

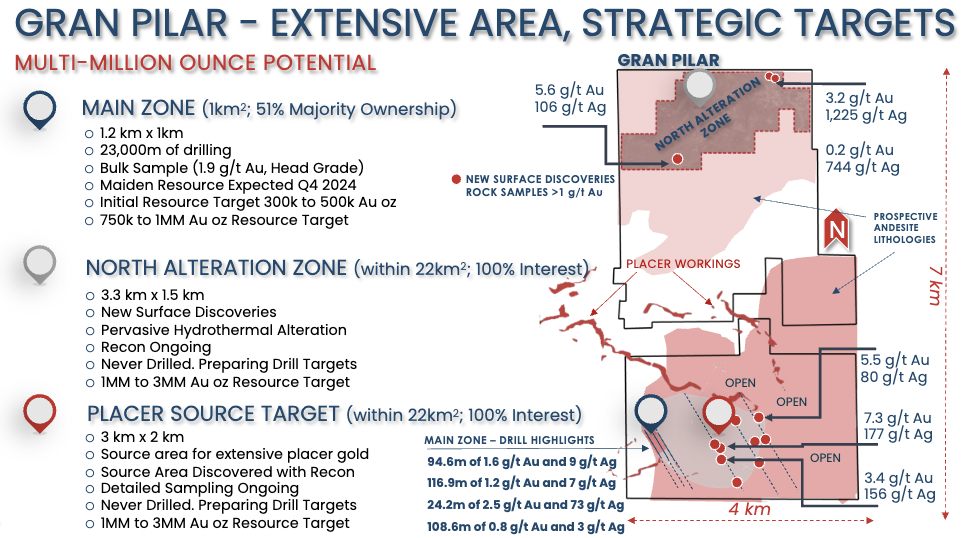

Astute readers are thinking… “yes, but what about equity dilution since mid-2021?” No, that’s not it, the Company has just 51.5M shares. Note: The Company will need to raise cash in the coming months. In the following image, notice the tiny darker pink rectangle labeled “Main Zone,” [MZ], marked by a blue circle.

That area is where historical drilling was done, yet it represents < 3% of the 45 sq. km land package. If the technical team can establish continuity across much of the southern half of that 45 sq. km, it would be transformative.

The North Alteration Zone (“NAZ“) is 4x bigger than the MZ, but far less explored. It has a nice 3.2 g/t Au + 1,225 g/t Ag sample, equal to ~18 g/t Au Eq. Between the NAZ and the MZ are placer workings (“Placer“) pointing to additional evidence of feeder zones. The area around Placer at 3 x 2 km is 5x the size of the MZ.

As mentioned, there are > 700 grab samples from the southern area (see map above) awaiting press release, and drilling will start again in November (4,000 meters planned). Sample results will not be announced until they’re all in. That way management can more carefully analyze them and provide insightful commentary.

It sounds like the results will be out next week or the week after. A maiden mineral resource estimate (“MRE“) in 1H 2025 for the initial Main Zone + adjacent trends will provide a good indication of blue-sky potential.

Timing of the MRE will depend on how well drilling is going. If well, the team might press on to get extra high-impact meters in. Management is outlining a permitting & operations strategy for a pilot plant facility underpinning a robust test mining scenario processing up to 50,000 tonnes.

Permitting is expected to be done this quarter, with a start of the pilot possibly in Q1/25. The Company will target surface material averaging ~1.3 g/t Au, with a base case heap leach recovery of 62%. CEO Sutherland thinks that with tweaking recoveries could improve to 65%-70%.

Management will be testing agitated leach + gravity to see if 90%+ recoveries are achievable. Roughly speaking, the payback period on a full-scale heap leach operation might be a year, and under two years for agitated leach + gravity.

With Au at US$2,760/oz., an efficient, low-cost operation should be capable of delivering profits of > $1,400/oz. On 50k ounces/yr. later this decade, that would be C$97M/yr. in operating income. Compare that to Tocvan’s enterprise value of ~C30M at $0.59/shr.

Catching up with CEO Brodie Sutherland is not easy. He’s just back from a major mining conference in Mexico where he reports that interest in Tocvan was strong, politicians made upbeat speeches, and attendance was high.

Brodie, please give us the latest snapshot of Gran Pilar and how it compares to the original Pilar property.

Gran Pilar is over 20x the size of the original land package. No modern exploration was done until we arrived. There are two target areas thought to be separate mineralized systems.

The Placer area is an extension of the original Pilar Main zone, and the North Alteration zone is a sizable area of untapped potential. Both provide Tocvan with ample targeting for million-ounce potential.

On Tocvan’s website is a detailed list of drill highlights. There are wide intervals of low-to-medium grades, but also [10.2 m at 12 g/t Au] & [9.2 m at 10.8 g/t]… And, a blockbuster [21 m at 31.2 g/t Au], incl. [6.0 m at 131.1 g/t]. What can we make of this?

Good question. Gran Pilar is made up of high-grade Au & Ag along fault structures with adjacent breccia veins also with excellent grade. The surrounding host rock has a low-grade halo that allows for a bulk tonnage target. When drilling we hit attractive high-grade zones but sometimes only see the low-grade.

Even the Lower grades tell us the system continues. We’re just starting to understand where the outer extents might be. It looks like it continues several kilometers to the east. All undrilled to date. Upcoming sample results will deliver important clues to a much broader system.

A large (unnamed) regional producer has expressed interest in Gran Pilar, what can you tell readers?

Yes, we‘re in continuous talks. From both sides, a full understanding of Gran Pilar’s potential is still developing. We feel there’s a tremendous upside. The interested party spent six weeks on site this summer, we will see how things play out, but we know there’s interest.

From our perspective, we don’t want to sell ourselves short. It’s better to keep exploring to better outline Gran Pilar’s potential.

Tocvan’s last press release stated, “Multiple Artisanal Underground Workings Found Tied to Broader Mineralized System” Please explain.

Exploration has been focused on an area immediately north & east of the original Pilar concessions, a place where no modern exploration had been done. We quickly identified new mineralized structures with historic workings dating back over a century.

We feel that finding workings across a broad area is a clear sign that more high-grade mineralization can be found. As we explore, identifying adjacent low-grade mineralization would greatly expand the resource potential. We plan to advance those target areas toward drilling as quickly as possible.

Thank you Brodie. Very promising developments at Gran Pilar. I can’t wait for sample results, followed by 4,000 m of drilling, a maiden resource estimate, and a pilot mining operation of 50,000 tonnes. That’s a lot of news and a lot of de-risking.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Tocvan Ventures, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of Tocvan Ventures are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Tocvan Ventures was an advertiser on [ER] and Peter Epstein owned shares in the company, purchased in the open market.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, or reported facts.

Leave a Reply