CoTec Holdings (TSXV: CTH; OTCQB: CTHCF) has done it again, another important move in cleantech, signing a binding long-term exclusivity & collaboration agreement with Salter Cyclones Limited for its Multi-Gravity Separators (“MGS“) technology to recover critical materials like iron ore & manganese from primary mining & tailings material.

MGS tech has been used for years to recover (tin, chromium, copper, zinc, etc.). Yet, its application to bulk commodities such as iron & manganese has been limited. CoTec believes the technology could be a step change in the handling of iron & manganese tailings.

MGS enables CoTec to produce high-grade iron & manganese concentrates from ultra-fine tailings, which are otherwise sent directly into tailings facilities. This is not a science project, it’s successfully being used at a commercial scale. CoTec CEO Julian Treger commented,

“…Our initial due diligence of the MGS tech produced exciting results from our Lac Jeannine Project in Québec, Canada. We plan to build on these results, supporting CoTec’s strategy to become a leading supplier of high-grade, low-carbon, iron concentrates.

This opportunity also offers CoTec the ability to become a supplier of high-grade manganese concentrate to the steel industry and producers in the high-purity manganese sulfate monohydrate (HPMSM) industry”.

Manganese (“Mn“) use in Li-ion batteries is soaring as lithium-iron phosphate (“LFP“) batteries have taken the world by storm, and Mn is being added to LFP to make LMFP batteries offering higher energy density + other attributes.

Each new tech & process innovation CoTec can deploy that increases recoveries by even just 1% is impactful at the bulk tonnage scale. MGS has the potential to boost recoveries by several percent, which at Lac Jeannine could (subject to further testing) materially improve project economics.

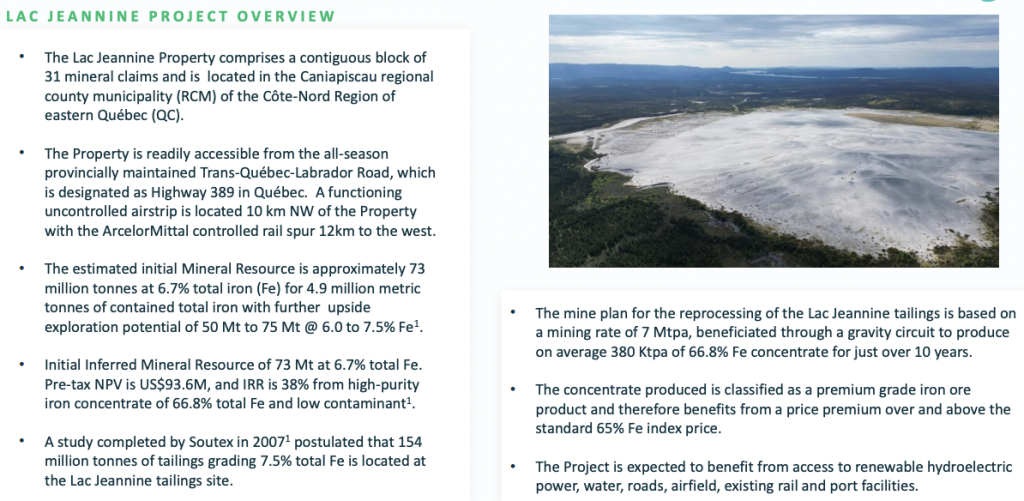

Management reported robust PEA results on the Lac Jeannine iron tailings project in Quebec, one of what will be tens of projects spanning several critical metals, technologies & jurisdictions, mostly in remediation/recycling settings.

Energy savings of up to 90% drive operating costs lower than conventional processes. It’s not just CoTec that sees BSL as disruptive, both Japan’s Mitsui & Co. and Australia’s Mineral Resources are invested in BSL.

The after-tax NPV & IRR of US$59.5M & 30% are strong but they fail to tell the whole story. In the press release, the following quote from CEO Julian Treger is important,

“The inclusion of the adjacent tailings has the potential to almost double the life of mine [its resource size] with virtually no additional cap-ex. We will focus on this strategy and several other optimization opportunities to further enhance the exciting results in the PEA.”

The surveyed area has a total estimated tonnage of 145M to 154M tonnes vs. the 73M tonnes included in the PEA. I estimate the NPV could grow to US$100M+ in this year’s Bankable Feasibility Study, or even higher if MGS technology is included.

Also reported was a promising, earlier-stage collaboration with WaveCrackerTM, that could be deployed alongside CoTec’s use of Ceibo technology.

CEO Treger commented “… CoTec is focused on technologies to leach low-grade primary copper sulfides & waste using a proprietary high throughput inorganic leaching technology Ceibo. We see the potential for using microwaves to pre-condition the rock before leaching. Pre-conditioning causes stresses & micro-fractures, potentially increasing permeability & recoveries”.

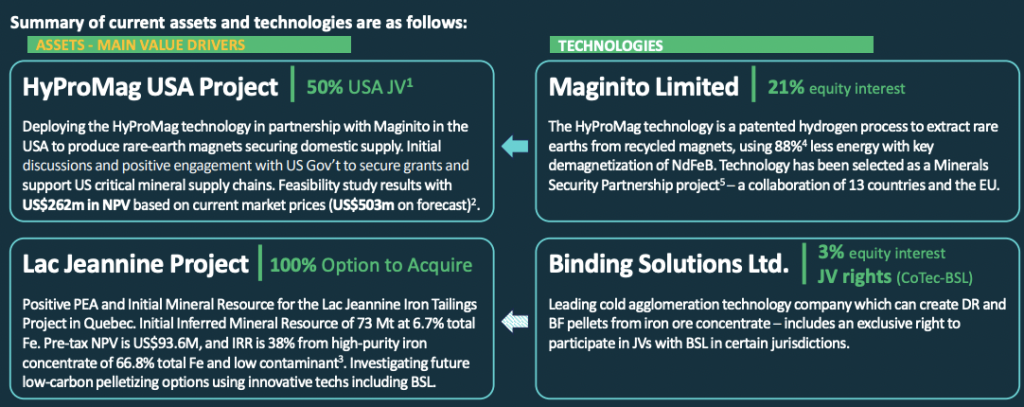

In November CoTec Holdings (TSXV: CTH; OTCQB: CTHCF) & JV partner Mkango Resources delivered a Feasibility Study (“FS”) for HyProMag USA, a state-of-the-art rare earth element (“REE“) magnet recycling & manufacturing operation, a game-changer for the long-term security of domestic supply of neodymium iron boron (“NdFeB”) magnets and REE powders.

CoTec will earn 60.3% of the economics from U.S. operations, plus 20.6% of HyProMag profits in the UK, Europe, Japan, and elsewhere.

Last quarter China banned the export of antimony to the U.S., sending the price up > 100%. The odds of critical REEs like neodymium & dysprosium being banned have soared. Even the export of NdFeB permanent magnets could be impacted.

That’s a huge problem as NdFeB magnets are crucial for national defense & homeland security. Magnets are used in the electric motors, generators, and actuators required by military applications including guided missiles, drones & vehicles.

HyProMag USA is a low-cost, low-energy, low-carbon footprint, sustainable business segment utilizing technology developed at the Univ. of Birmingham in the UK, underpinned by US$100M of R&D funding to date.

NdFeB magnets also support the automotive, aerospace, medical science, data center, robotics, AI & energy transition industries. Project economics are favorable with a post-tax NPV(7% real) of $262M and a real IRR of 23%.

NdFeB magnets are being produced & successfully tested by prospective investors & customers. The magnets will be made with materials sourced domestically, contributing to the security of magnet supply and enabling economical, traceable, U.S. production of recycled REE magnets.

The low all-in-sustaining cost (“AISC”) of $19.6/kg compares favorably to current prices. Upfront cap-ex is manageable at $125M. For HyProMag USA, production of 750 tonnes/yr. of recycled NdFeB magnets, + 291 tonnes of NdFeB co-products, results in total payable production of 1,041 tonnes/yr. over 40 years.

Later this decade a third HPMS vessel could be added in Texas. If included in the FS it would have added $10s of millions in post-tax NPV for an incremental $7M in cap-ex. B the early 2030s, HyProMag USA hopes to have up to 10% market share of domestically-produced NdFeB magnets.

Several high-tech/green energy innovations are coming to the south-central U.S., most notably semiconductors & EV/battery plants. Tesla’s gigafactory is ~220 miles away.

Also in the south-central U.S. are aerospace & defense industry facilities, and renewable energy/cleantech manufacturing hubs. Texas is an important area for the AI/Machine Learning efforts of Google, Microsoft & IBM.

HyProMag Ltd. is collaborating with Areera Ltd. on the recovery & recycling of REE magnets embedded within speaker assemblies, representing a major market opportunity for recycling speaker motors as minimal quantities are currently recovered.

While not a sure thing, being awarded grant(s) totaling $10s of millions, and financing 65%+ of upfront cap-ex with debt, would substantially reduce the equity component.

In total, those avenues of funding could be substantial. Government support will likely be available, in various forms, for other CoTec projects.

The Dept. of Defense [“DoD“] awarded $45M to MP Materials and MP received a $60M tax credit through the Inflation Reduction Act [“IRA”] Section 48C. The DoD granted $288M to Lynas USA and $94M to E-VAC Magnetics, which also received a $112M IRA tax credit.

Assuming that HyProMag USA accounts for 40% of CoTec’s enterprise value (market cap + debt – cash), it’s valued at less than 10% of its [60% share of post-tax NPV].

In addition to HyProMag USA and Lac Jeannine, CoTec is pursuing opportunities to leverage its access to Binding Solutions (“BSL“) where fine materials from mines/waste dumps will be converted into iron pellets or briquettes for use in the production of green steel (steel with ~70% less carbon dioxide emissions).

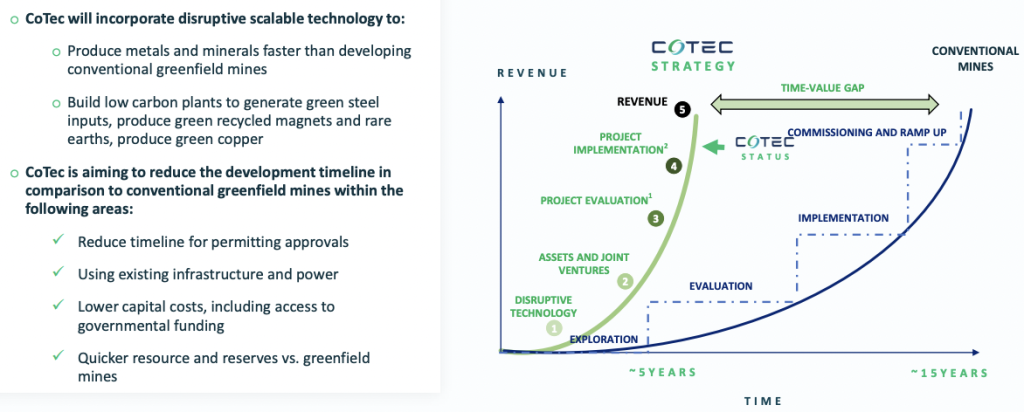

Readers are encouraged to look beyond just HyProMag USA & Lac Jeannine, which should be generating cash flow in 1H 2027. Most junior miners have one flagship asset where operating improvements are possible, but overall flexibility is low.

By contrast, CoTec will have multiple shots on goal by deploying technologies more cheaply, (lower capital intensity), faster, more sustainably (greener), and at a greater scale.

Optimization of equipment & materials + economies of scale will drive margins. Lac Jeannine alone is not a Company-maker, but that’s kind of the point. No single project or technology will MAKE, OR BREAK, this Company.

As management adds low-cost iron ore tailings projects like Lac Jeannine to its portfolio, logistical/operational synergies, incl. leveraging BLS, could make this segment a Company-maker alongside HyProMag USA + HyProMag (rest of world).

Numerous projects running concurrently over decades will provide strong revenue growth, margins & diversification. This won’t happen overnight, we’re two years from initial cash flows. However, the 2030s could see over a dozen projects up and running.

CoTec Holdings (TSXV: CTH; OTCQB: CTHCF) is one of the lowest-risk cleantech plays that also has very considerable blue-sky potential due to investments in, and access to, truly disruptive technologies and a very talented management team, board & slate of advisors.

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER] ) about CoTec Holdings, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of CoTec Holdings are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, CoTec Holdings was an advertiser on [ER] and Peter Epstein owned no shares in the company.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector, or investment topic.

Leave a Reply