U.S. stock markets have (more than) bounced back from April’s lows, giving the impression that China/U.S. relations are on the mend. Yet, evidence to the contrary is everywhere.

The U.S. Commerce Department warned American businesses to avoid Chinese-made microchips. Will China provide the West with Rare Earth Elements & permanent magnets if the U.S. prohibits China’s use of Nvidia’s semiconductors?

This is more than just a trade war… It’s a Cold War spanning military, economic, technological, cultural & ideological realms. Other grave geopolitical risks: China/Taiwan, Russia/Ukraine, India/Pakistan, the Middle East, the U.S./Europe (50% tariffs?!?), etc., should place a floor under the Au price.

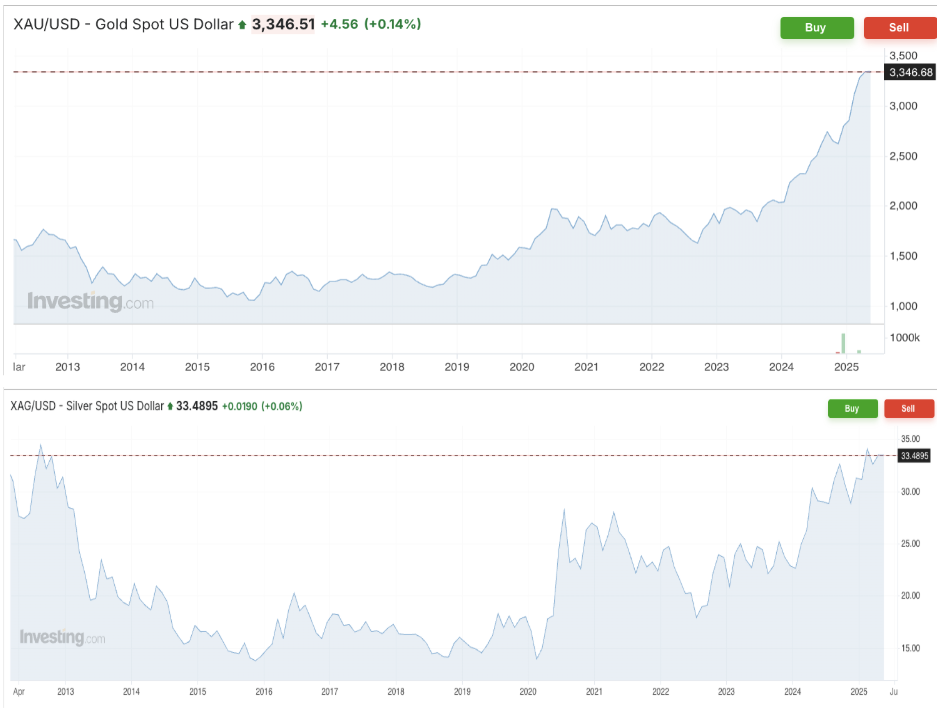

Gold (“Au“) is up +40%!! in the past year, and on April 21st, it touched an all-time high of $3,500/oz. Silver (“Ag“) has lagged behind, but is +15% YTD. Although Au has eased back to $3,308, geopolitical events could pop up (again) at any time.

And then there’s Ag. I make the same arguments again & again not because I’m lazy, but because the fundamental outlook is so bright. Au is ~5% from its all-time inflation-adjusted high, yet Ag is ~64% below its high.

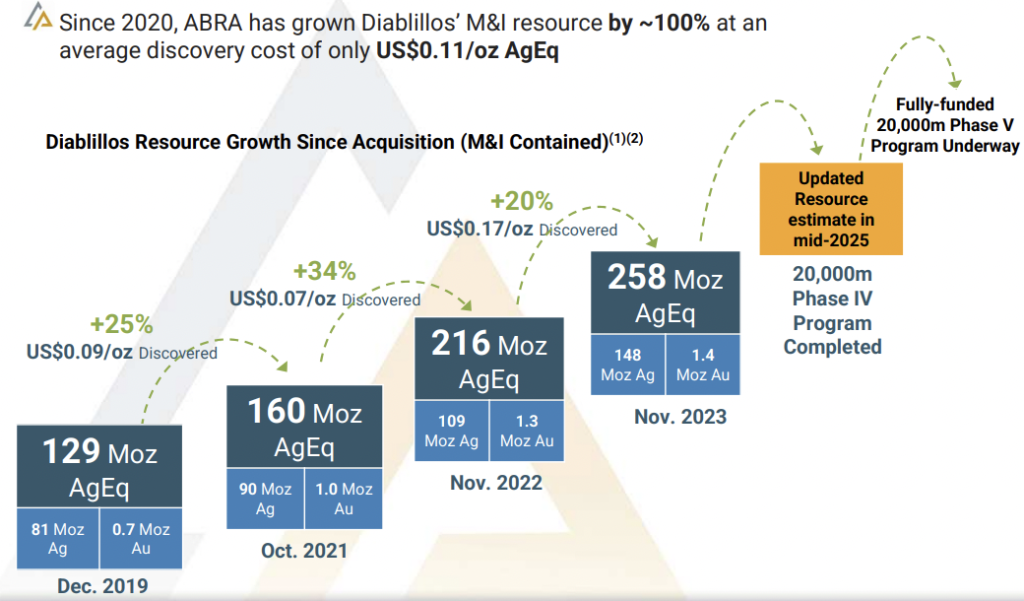

The long-term average Au: Ag ratio is roughly 61:1 vs. today’s 100:1. It was 73:1 a year ago. At 80:1, the Ag price would be ~$41.35/oz. This year will be the 5th in a row of meaningful Ag deficits. The total mined Ag shortfall from 2021–2025 is estimated to be ~800 MILLION OUNCES — a full year’s production.

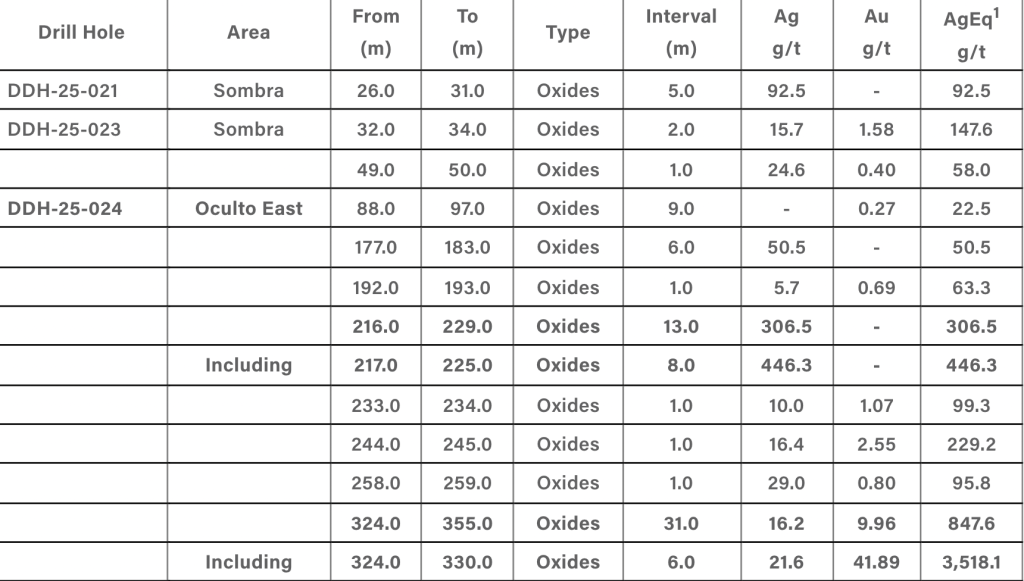

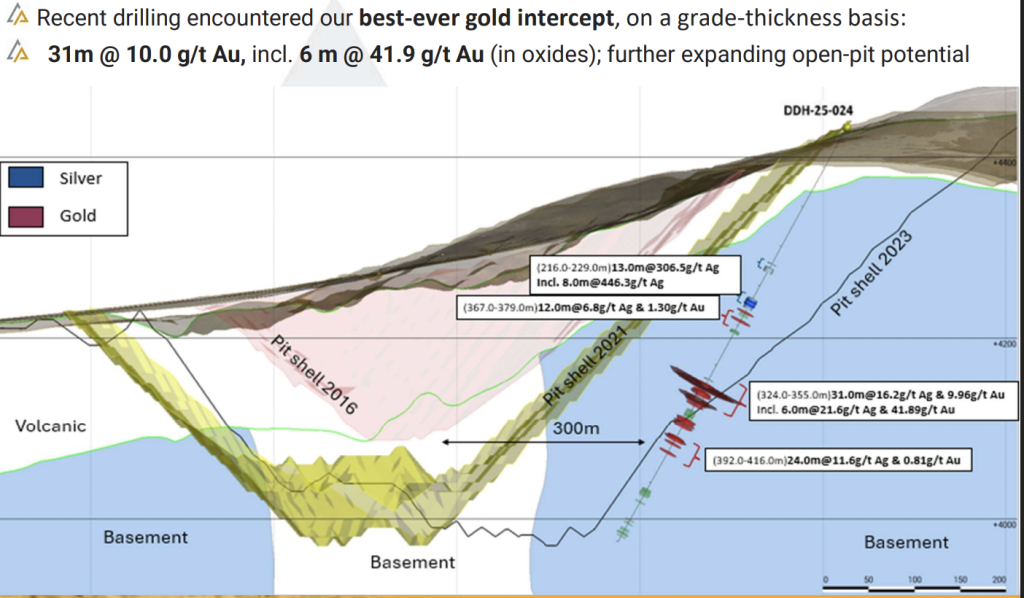

On May 20th, AbraSilver Resource Corp. (TSX: ABRA) / (OTCQX: ABBRF) reported its best drill interval ever (for Au) at the 100%-owned Diablillos primary Ag project. The headline intercept was 31.0 m of 10 g/t Au(in oxides), incl. 6.0 m of 41.9 g/t Au(~4,152 g/t Ag Eq.)

The latest blockbuster interval is from step-out drilling just beyond the eastern margin of the conceptual Oculto open pit. Chief Geologist Dave O’Connor believes high-grade mineralization could extend another km to the east. He also said,

“This extremely impressive hole confirms that the deeper gold zone extends beyond the known boundary at Oculto and the upper silver zone may extend farther than previously defined. Our team will immediately commence a systematic drill program to follow-up on these robust initial results and better define the extent of the high-grade extension.”

If this is a game-changer — as some suggest — the current Measured + Indicated + Inferred resource of ~294 Ag Eq. ounces (at spot pricing) could grow substantially.

The OE target is highly promising as results are confirming a degree of continuity at both the Ag-enriched horizon plus the deeper, higher-grade Au zone.

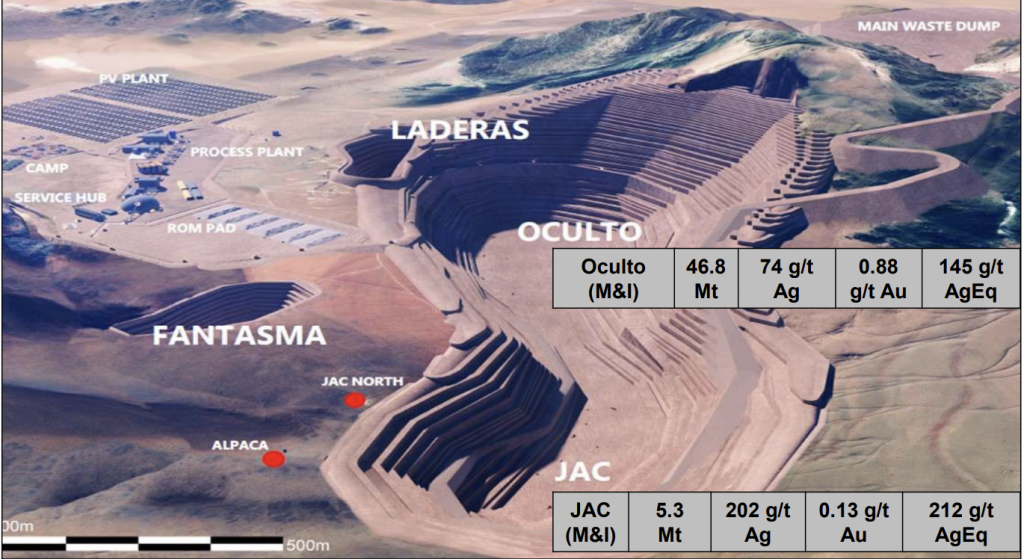

There remains good potential to find additional mineralization to the east & NE of the existing Oculto open pit area. High-grade Au starts at a down-hole depth of 324 m, but is only ~200 m vertically from the surface, making it amenable to open pit mining.

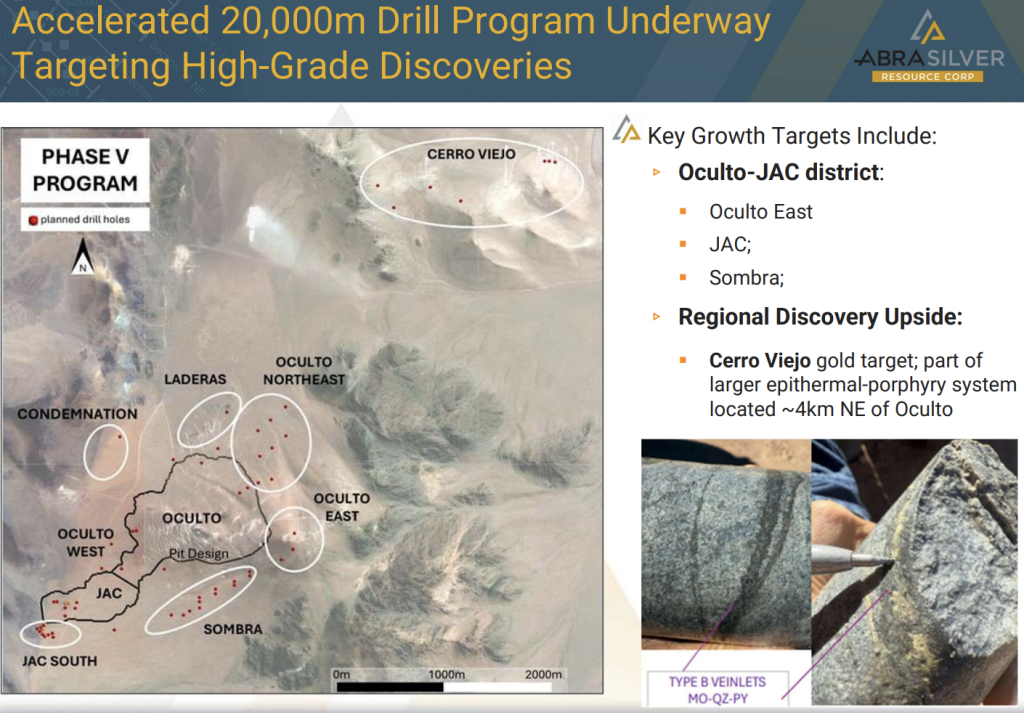

I won’t guess how large Diablillos could be, but the possibilities are vast. In addition to drilling out JAC, Oculto, OE/NE, at least two other zones of increasing interest are Sombra, which is quite close to JAC & Oculto, and Cerro Viejo, 4 km to the NE, see map below.

Oculto & OE are known to be quite promising, but focus had moved to the high-grade JAC zone. Now, management has several exciting areas open at depth and in multiple directions. CEO John Miniotis commented,

“These spectacular intercepts clearly demonstrate strong potential to expand high-grade mineralization well beyond the existing Oculto deposit. With three drill rigs now active across the broader Diablillos land package, we are entering another exciting phase of exploration aimed at unlocking substantial value for shareholders, working in parallel with our ongoing Definitive Feasibility Study.”

Other major high-sulphidation epithermal deposits in S. America include: Kinross Gold’s La Coipa (Chile); Newmont’s Yanacocha (Peru); Barrick’s El Indio (Chile); and Barrick’s / Shandong Gold’s Veladero (Argentina).

Besides Barrick, other significant producers in Argentina include: Rio Tinto, AngloGold Ashanti, Hochschild Mining, First Quantum, SSR Mining, Pan American Silver, Fortuna Mining, and Mineros S.A.

Fantasma & Laderas are mineralized, but little work has been done. Cerro Viejo is prospective as it already has a discovery hole (36 m at 1.9 g/t Au, incl. 5 m of 7.2 g/t).

Management is considering adding a fourth drill rig as the Company has “too many targets.” Imagine how much drilling could be done by a strategic partner or acquirer at half a dozen existing targets and in search of more discoveries.

Last week’s blockbuster hole came early in Phase 5… So, there *could be* even better intercepts to follow. If Sombra, Cerro Viejo, Fantasma, and/or Laderas are well mineralized, and if new discoveries are made, the Company-wide resource size could soar.

Line-of-sight to a larger resource & Definitive Feasibility Study has many groups watching Diablillos. Three recent acquisitions –> Gatos Silver acquired by First Majestic, SilverCrest by Coeur Mining, and MAG Silver by Pan American, leave AbraSilver at or near the top of producers’ takeover lists.

AbraSilver is valued at a 17% discount (see chart below) to the average of Outcrop Silver, Vizsla Silver, Sierra Madre, Dolly Varden, Prime Mining, Andean Silver, and New Pacific Metals, and a 32% discount to Vizsla, even though it’s more advanced at PFS-stage and has 82% more Ag Eq. ounces than the peer average.

I believe AbraSilver has greater resource growth potential than most of its peers, and given recent drill results, a good opportunity to increase its resource grade –> Thirty-one meters @ 10 g/t Au is ~1,000 Ag Eq.

Majority of oz @ Oculto (145 g/t), but upside potential at higher-grade JAC & OE

Notice that 5 of 7 names are at the pre-PEA stage, showing the dearth of advanced, undeveloped primary Ag projects. To make the comps more equal to PFS-stage AbraSilver, I added 33.33% equity dilution to the five pre-PEA companies.

At the bottom of the chart is mid-tier producer Endeavour Silver, valued at $10.92/oz(on 140M Measured, Indicated + Inferred Ag Eq. oz). It could triple its resource & lower its per-oz valuation to $5.43/oz by acquiring AbraSilver at a 50% premium.

AbraSilver & Vizsla are clearly front-runners to be acquired, two prime takeover candidates with excellent projects in Western-friendly countries, and over a dozen prospective suitors.

Readers are reminded that Mexico is by far the largest Ag-producing country. Many potential acquirers of AbraSilver are overexposed to Mexico and stand to benefit by diversifying into a strong province (Salta) in Argentina.

AbraSilver’s team has enough cash and a great team to continue drilling & developing Diablillos into next year. Therefore, management is in no rush to be acquired anywhere near the current share price.

As mentioned, Pan American, Coeur & First Majestic have bought meaningful Ag-heavy companies in the past year, but Hecla, Endeavour Silver, Fresnilo, Industrias Peñoles, South32, and others have not.

There are few high-quality, primary Ag projects in the world not owned by producers. The best comp for Diablillos is Vizsla Silver’s Panuco project in Mexico (PEA-stage, 55% Measured & Indicated), vs. Diablillos (PFS-stage, 94% Measured & Indicated).

Diablillos has a low AISC ($12.67/Ag Eq. oz) in its PFS, making it poised to benefit from current or rising Au/Ag prices. AbraSilver has ~C$50M in cash, funding it to a construction decision next year. A new resource estimate remains on track for July.

I think there’s compelling capital gain potential (with relatively low risk vs. pre-PEA peers), especially upon higher Au/Ag prices and/or heated M&A activity — perhaps including bidding wars.

All else equal, each +10% in Au/Ag prices boosts post-tax NPV(5%) by about +30%. Diablillos has everything needed to be a substantial Ag/Au mine. It has a solid grade (that’s improving), a large resource (that’s growing), in a safe, prolific jurisdiction (Salta Province, Argentina).

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about AbraSilver Resource, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of AbraSilver Resource are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, AbraSilver Resource was an advertiser on [ER] and Peter Epstein owned shares in the company.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.

Leave a Reply