Junior miners are an incredibly diverse group spread across dozens of metals / minerals / materials, development stages, and 100s of jurisdictions.

A good approach to assess juniors is to look closely at; 1) the experience, track records & motivations of key team members, 2) a company’s ability to raise capital, and 3) the size of the prize.

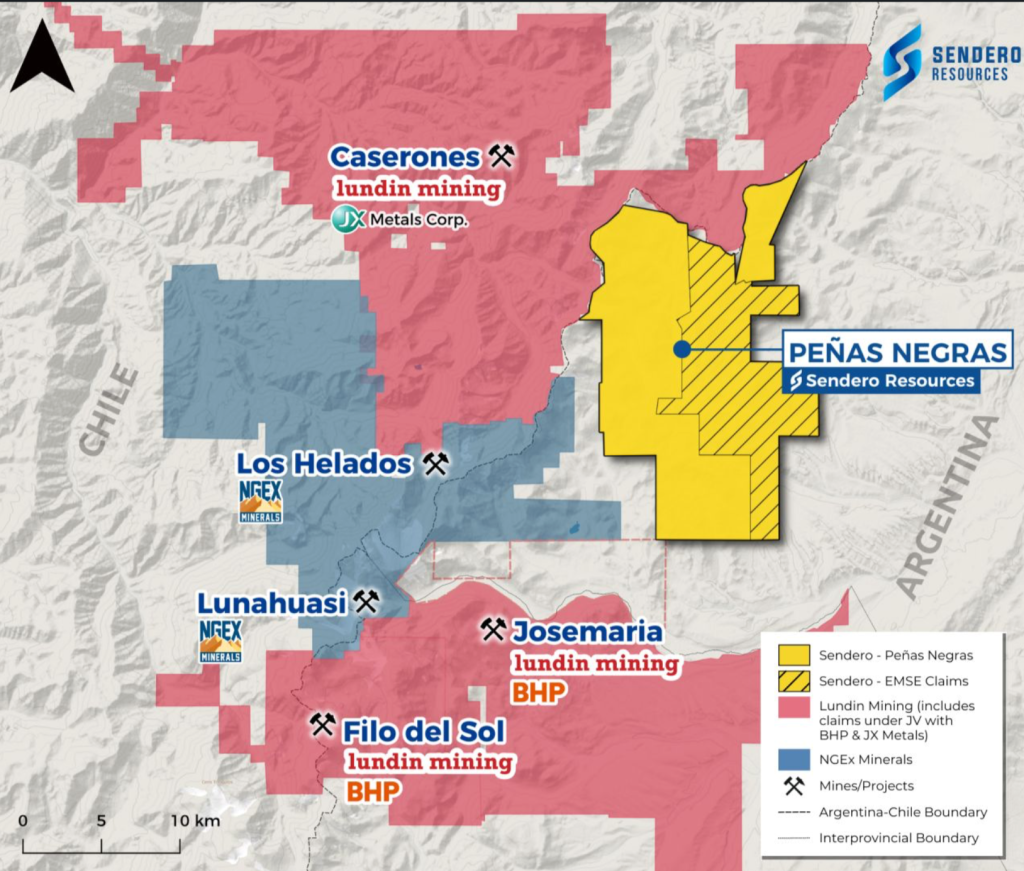

Argentina’s Vicuña District, one of the hottest Cu/Au regions

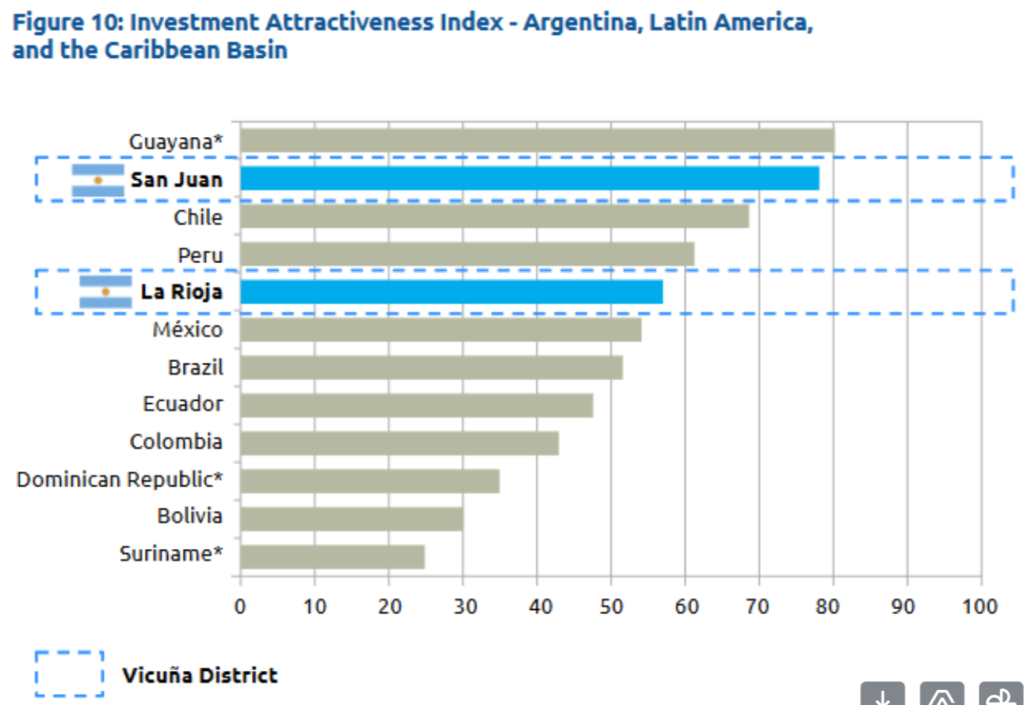

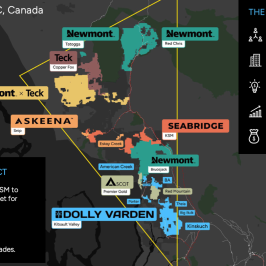

Let’s start with the size of the prize. Please Zoom in on the map to see key players in and around Argentina’s Vicuña District… A great jurisdiction compared to other top copper (“Cu“) / gold (“Au“) locations in Indonesia, Mongolia, Kazakhstan, Serbia, the DRC, Zambia & Namibia.

BHP, Lundin, NGEx, Teck, Newmont, Barrick, Kinross, Antofagasta…

Sendero Resources (TSX-v: SEND) has a large, contiguous land package in the heart of the Vicuña District surrounded by Majors.

The Company’s enterprise value is ~C$9M. (20M shares at C$0.41 + ~C$1M in net debt September 15th). Readers should note there’s 12.7M warrants struck at C$0.16. Sendero is not the only S. American junior near Cu/Au giants, but it’s one of the lowest valued and has the backing of legendary mining execs.

Sendero’s flagship Peñas Negras is 16 km East of Los Helados, 18 km SE of Caserones, 24 km NE of Lunahuasi, and 32 km north-NE of Filo del Sol. It’s within 200 km of assets held by Barrick, Teck, Newmont, Kinross, Anglo American, BHP/Lundin Mining & Antofagasta.

The Vicuña District spans parts of Argentina & Chile and is one of the world’s most exciting mining regions. The Josemaria + Filo del Sol projects alone host 157 billion Cu Eq. pounds.

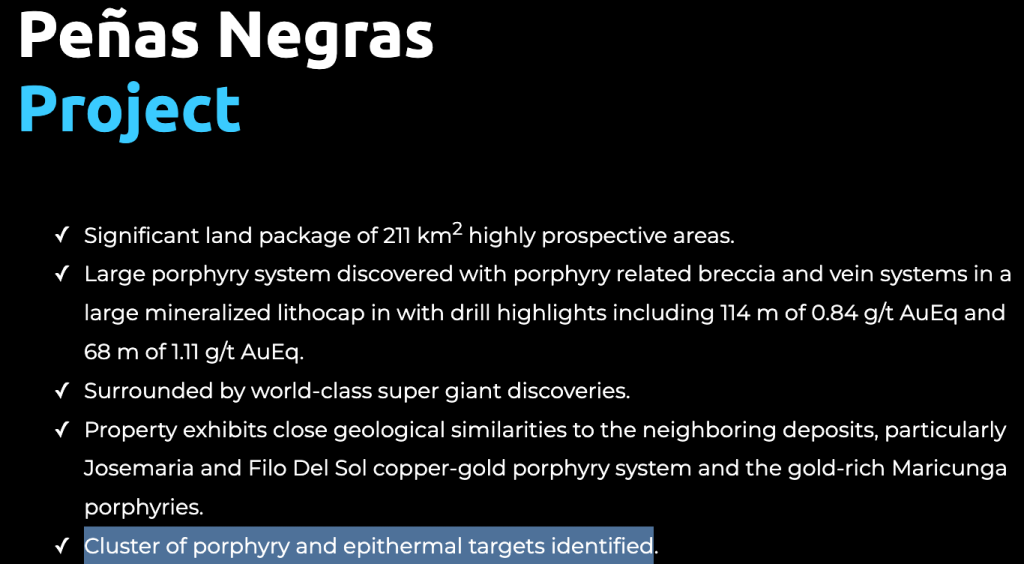

Multiple porphyry & high-sulphidation epithermal targets have been identified on Sendero’s property. Its project is surrounded on three sides by the Caserones, Los Helados, Lunahuasi, Filo de Sol & Josemaria mines/projects.

BHP is a Major miner, Lundin is a C$15.0B company, NGEx is valued at C$4.7B. It might seem likely that one of those will strike a deal with Sendero. However, they have a lot on their plates.

Gold companies soaring, many looking for undervalued Cu plays

Imagine how attractive Peñas Negras might be to new entrants like; Grupo México / Southern Copper, Glencore, Freeport, Rio Tinto, Vale S.A., Buenaventura, Hudbay Minerals, First Quantum, McEwen Mining, South32 or Capstone Copper.

Or, Japanese commodity traders; Mitsubishi, Mitsui & Co, Itochu & Sumitomo, have interests in mines/projects/companies across S. America. And, royalty/streaming giants Franco-Nevada, Wheaton Precious Metals & Royal Gold have significant S. American investment portfolios.

Any of those groups could easily deploy C$10s of millions to gain an inside track via a 10%-20% stake at the project level. Sendero has 100% ownership of 120 sq. km of claims, plus an option to earn up to 100% of another 91.77 sq. km.

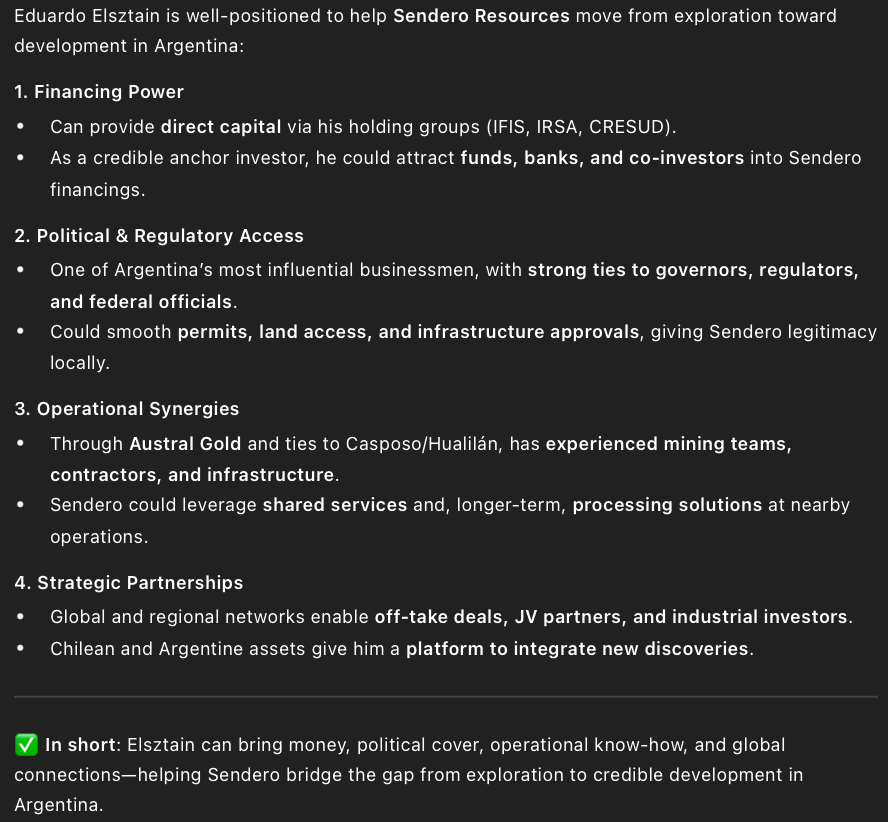

I mentioned how incredibly important access to capital is. Sendero has at least three aces in the hole, Eduardo Elsztain, Peter Marrone & Pasquale (Pat) DiCapo. Below, ChatGPT describes how Mr. Elsztain could help advance Peñas Negras.

Mr. Elsztain is one of Argentina’s most successful and well-connected businessmen. He’s been increasing his investments in junior minting companies like Sendero.

Peter Marrone is the Founder of Yamana [acquired for ~C$6.5B] and of Allied Gold). Mr. Marrone is currently Chairman, CEO and a significant investor [a C$100M shareholding] in Allied (C$2.5B market cap).

Three metals/mining Big Shots backing Sendero Resources

Peter has > 35 years’ experience in mining, business & capital markets and a highly impressive network of high net worth individuals and institutional groups that can be tapped for investment capital.

Pat DiCapo & PowerOne Capital Markets (owned by Mr. DiCapo) own > 10% of Collective Mining, worth > C$100M, and > 10% of White Gold, worth > C$10M. Execs like Eduardo, Peter & Pat with shareholdings this large have net worths in the C$100s of millions.

Why would they bother with Sendero Resources? Tremendous blue-sky potential and the opportunity if they’re right, to champion the next substantial Cu/Au project in a world-famous district.

Those three + associates, reportedly own over 45% of the Company. Operating plans (drill targets, exploration studies, etc.) are still being worked on, and trading volume is very low. Once the story becomes better known and drill plans are announced, volume should pick up.

Sendero Resources represents a truly unique & compelling opportunity. Significant investment by previous operators provides a low-cost entry into a property of proven merit—situated in one of the world’s most prolific Cu/Au regions, as demonstrated by our neighbors’ incredible successes. The Province is delivering exceptional support to projects in the Vicuña District, further enhancing the attractiveness of this investment proposition. With an unparalleled combination of accomplished technical expertise, and seasoned leaders in mining finance, Sendero stands on a foundation of strength & credibility. Coupled with a very low valuation, Sendero offers an exciting way for astute investors to get Cu/Au exposure.

— Jeremy Gillis — Director of Capital Markets

CEO/Dir. Alex Gostevskikh, MS Geology, MBA, QP MMSA has > 40 years’ experience in international mining & exploration specializing in mineral exploration & development of orogenic Au style mineralization Several senior & executive roles with companies incl. at Kinross & Centerra.

Director Steven McMullan, P. Geo, was a member of the Kamoa Copper (a Top-5 Cu complex in the world) discovery team, for which he received the Thayer Lindsley Intl. Discovery Award. Steven has > 40 years’ experience in mineral exploration/discovery, mine development & project management across five continents.

So far, [Filo del Sol + Josemaria + Los Helados] have booked > 14 billion tonnes of mineralization, and NGEx’s Lunahuasi looks like another monster. Yet, in my view, at a valuation of C$9M, the market seemingly ascribes < a 5% chance of an economic deposit

I think the chances are much better. The geology & structure appear to host low-grade, bulk tonnage Cu/Au mineralization. Peñas reportedly shares similarities with its neighbors, particularly the Josemaria Cu-Au porphyry system (23.7B pounds @ 0.45% Cu Eq.).

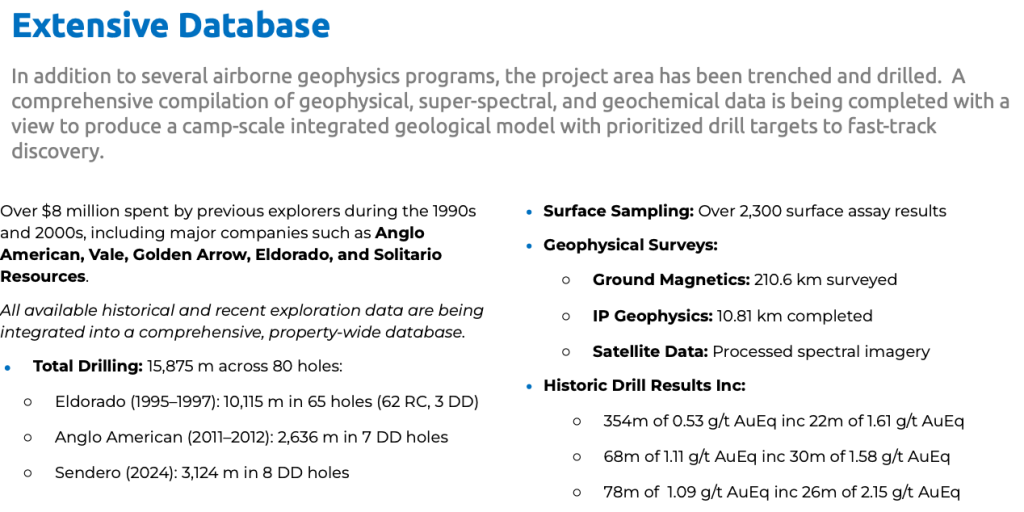

Historical drilling in the 1990s/2000s, and last year by Sendero, barely scratched the surface of this 212 sq. km property. Importantly, the new team has developed a robust geological model and compiled an extensive database on Peñas and the entire district.

Peñas is close to roads, deep-water ports, skilled labor, and will have access to power as nearby projects approach production. More infrastructure is coming, largely funded by neighbors.

While the market did not applaud last year’s 364 m of 0.51 g/t Au Eq., from 34 m, incl. 114 m at 0.84 g/t Au Eq. — at spot pricing, 0.51 g/t equals 0.58% Cu Eq. (assuming 100% recoveries).

Many juniors including Entrée Resources, Aldebaran Resources, Ero Copper, ATEX Resources, Osisko Metals, Marimaca Copper, Hot Chili, Faraday Copper, Firefly Metals & Panoro Minerals report sexier intercepts, but have market caps of C$260M to C$2.3B.

A Cu Eq. grade of 0.40%, in a billion tonne resource, is 8.8B Cu Eq. pounds. To be clear, no one knows if a property-wide grade of 0.40% is achievable OR how much mineralization there might be.

What is a pound of Cu Eq. in the ground worth in S. America? Valuations vary from ~C$0.005 to over $0.15/lb., with a median of ~C$$0.03/lb. At C$0.015/lb. 8.8B pounds is worth C$132M.

“Cluster” of targets… could there be new discoveries?

Jeremy Gillis is Director of Capital Markets. He’s done several video interviews extolling the virtues of the new & improved Sendero story. He has a meaningful shareholding + warrant position and has been buying shares in the open market.

Sendero is high risk, but some key risks have been mitigated

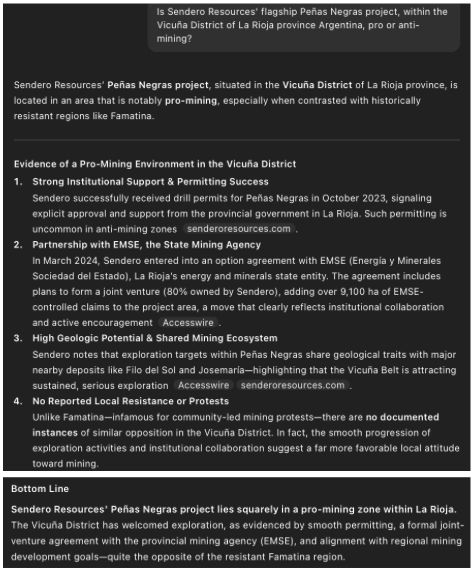

Knocks on Sendero are; 1) La Rioja province seen as anti-mining, 2) last year’s 10 for 1 rollback, 3) non-splashy grades, 4) a 4,000 meter elevation, 5) management/board turnover, 6) JV terms with EMSE, and 7) low trading volume.

The first concern is understandable as the La Rioja province has a checkered past. However, like in most countries, only certain parts are anti-mining.

BHP’s & Lundin’s active development plans alongside NGEx prove that local communities are on board. See commentary from ChatGPT below…

Regarding the share rollback, it was NOT done in desperation. It was deemed necessary to provide a clean slate to move forward.

Regarding altitude, yes, the 4,000 meter elevation impacts project economics & logistics, but it just means higher operating costs, it’s not a project-killer. The nearby, PFS-stage, Filo del Sol, in a 50/50 JV of BHP & Lundin Mining, is at ~5,100 m.

Regarding prior executive turnover, Sendero’s current team & financial backers is world-class. Finally, a critical agreement with EMSA has been renegotiated on more favorable terms.

Original Agreement:

- Ability to earn up to 80%, but without clarity for the remaining 20%

- US$5M in cash paid over 4 years

- US$10M in exploration expenditure over 4 years

- 1% NSR

New Improved Agreement:

- Ability to earn up to 100%

- US$65,000 in cash paid over 5 years

- US$5M in exploration expenditure over 5 years

- 1% NSR, with more favorable terms

If one’s impressed by the team assembled to move Peñas Negras forward, confident in its ability to raise capital, then investing at a C$9M valuation offers compelling risk/reward.

Sendero’s valuation a rounding error for prospective strategic partners

Dozens of companies should want a meaningful shot at greatness in the heart of the Vicuña District. However, will BHP/Lundin/NGEx allow a competitor to benefit from their years of hard work, capital deployed & infrastructure building?

All roads lead to a higher valuation for Sendero Resources, possibly much higher. Peñas Negras is mineralized, the questions are — how much, what grade, and will more discoveries be made?

At today’s Cu/Au prices, a resource grade of 0.35% Cu Eq. might be all that’s needed. Next door, Caserones is in production with a remaining resource grade of 0.28% Cu Eq.

Although certainly possible, I can’t imagine how Sendero could have meaningful downside from today’s valuation, while the upside potential is quite remarkable.

DISCLOSURES — Peter Epstein of Epstein Research [ER] owns shares in Sendero Resources acquired in the open market. [ER] has no existing or prior business relationship with Sendero or its management team/board/advisors. In the future, Mr. Epstein will consider inviting Sendero to become an advertiser on [ER], but no implicit or explicit agreement has been reached.

Leave a Reply