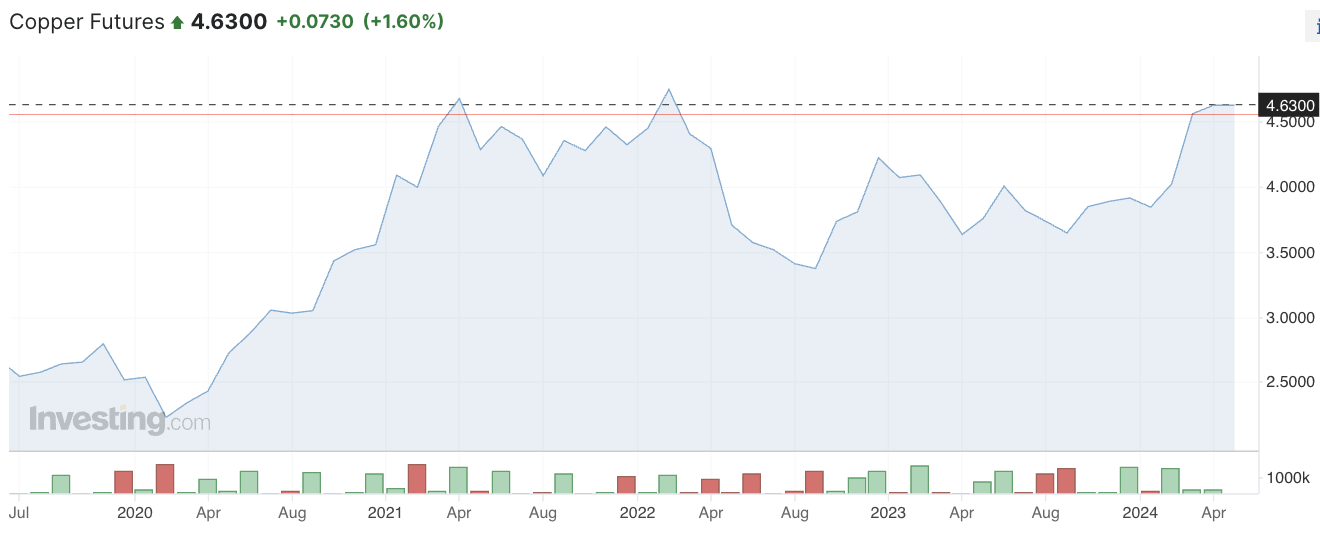

Year-to-date copper (“Cu“) is up +19% vs. +14% for silver & +13% for gold. Last week Goldman Sachs upped its 12/31/24 Cu forecast to $12,000/t = $5.44/lb. and reiterated that Cu will average $15,000/t = $6.80/lb. in 2025. If $6.80/lb. is the average, imagine how high the price might go… $8.00/lb.?

GS believes there will be a combined Cu deficit of 921k tonnes this year & next. There are hundreds of Cu juniors, of which dozens look promising.

However, even the most impressive ones could be 10-20 years from commercialization. And, some of the best projects might never reach production due to geopolitical constraints, local community opposition or environmental/water challenges.

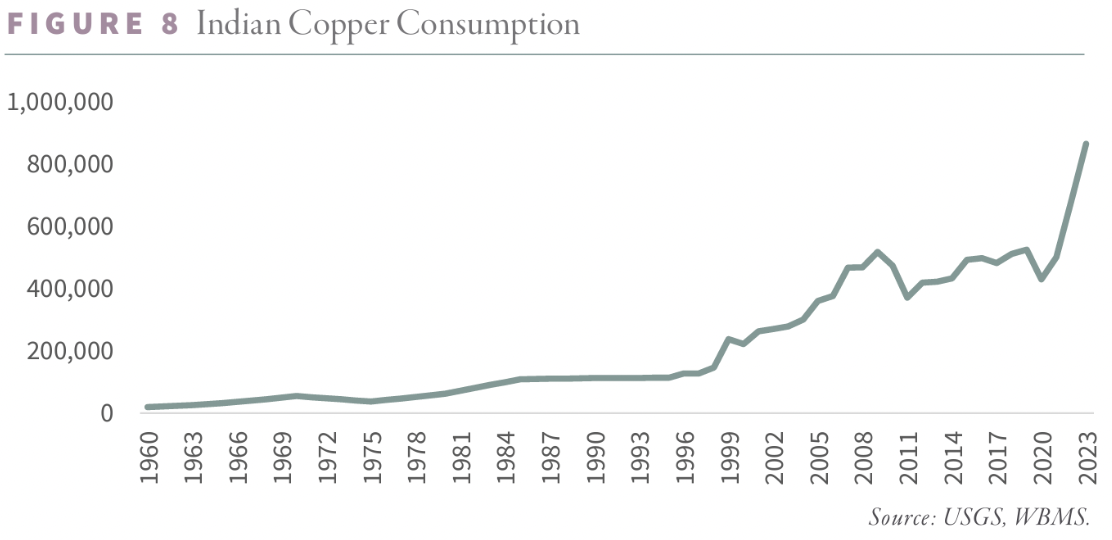

The long-term supply of Cu is highly uncertain, yet demand continues to grow at an above-average pace. Even though China’s economy has been weaker than usual, look at the chart of Cu demand from India. According to Goehring & Rozencwajg, India’s per capita GDP will reach $2,800 this year.

Despite a doubling of Cu consumption in the past two years, India’s per capita installed Cu base remains low at 15 pounds, a third of China’s level of 45 pounds in 2003, when China’s per capita GDP was $3,000.

Goehring & Rozencwajg point out that Chinese Cu demand increased over four-fold from 2000 to 2010. In addition to India’s ascendency, last month Trafigura said demand for electricity from AI, supercomputing & the cloud will require a million tonnes of incremental Cu not baked into analyst models a year ago.

That estimate could prove to be low, but it already adds ~0.5% to the CAGR through 2030. Cu consumption is now expected to grow ~3%/yr., up from ~2%/yr. from 2000 to 2022.

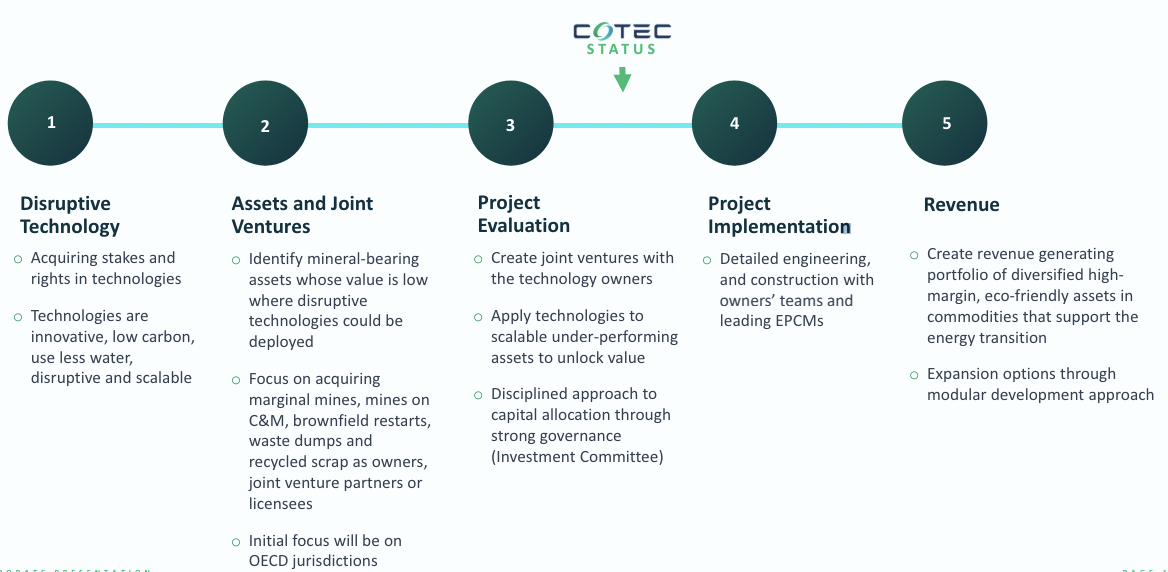

S&P Global recently commented that for new mines it takes an average of 18 years from discovery to first production. Clearly, something needs to change to better align anemic supply to robust demand. CoTec Holdings (TSX-v: CTH) / (OTCQB: CTHCF) offers a solution, not just in Cu, but in iron ore for green steel & REEs.

It plans to commercialize projects in 3-5 years instead of 18. In addition to speed to market, CoTec’s projects are very low cost & green. They are scalable & sustainable.

All of these factors point to the potential for strong long-term growth of high-margin segments. Underpinning CoTec’s business model is the use of disruptive technologies, in some cases more than one at a single site.

CoTec has an amazing management team & board (see above/below) that has vetted over 300 technologies and invested in three. In this prior article I described the blue-sky promise of each technology.

To learn more about the Company, I sat down for an exclusive interview of CEO Julian Treger, who through his family Trust is the largest shareholder.

Not many execs of junior mining companies have a degree from Harvard and an MBA from Harvard Business School…. There are several other high caliber team members, such as Dir. Tom Albanese was the CEO of Rio Tinto from 2007-2013.

Dir. Lucio Genovese has 33 years in the merchant & financial sectors of the metals & mining industry, including senior roles at Glencore Intl. Dir. Erez Ichilov served as a MD at Traxys Group, a well-established global physical metals trading house with ~US$10 billion in sales& ~500 employees.

Review bios of other key execs here. CoTec has an enterprise value of ~$32M. Without further ado, my interview with CEO Treger.

Hello Julian, thank you for your time. Could you please share the latest snapshot of CoTec Holdings?

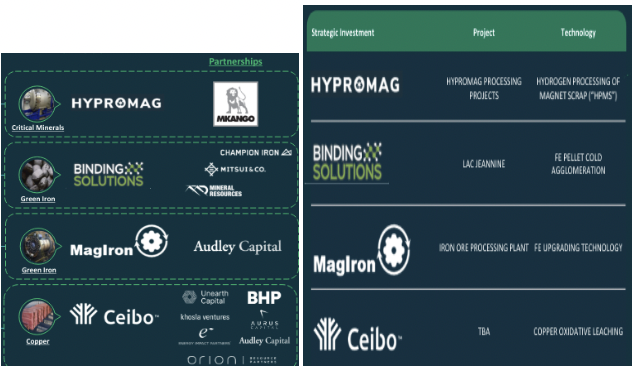

Yes, our team is excited about the progress we’re making. Having reviewed over 300 cutting-edge technologies to date, we have made minority technology investments in three that we think are disruptive and one investment in a green iron project based on patented technology.

Disruptive means, significantly better in several ways; cheaper, faster, greener, simpler, scalable & long-term sustainable. We are deploying three (and eventually more) technologies, mostly for reclamation & recycling.

We expect cash flow in the U.S. from our HyProMag segment, a 50/50 JV, from 2026 onwards. HyProMag recovers REEs from electronic scrap and manufactures new REE magnets.

In our Binding Solutions Ltd. (“BSL“) segment, fine materials from mines/waste dumps are converted into iron pellets or briquettes for use in the production of green steel, (steel with ~70% less carbon dioxide emissions).

Energy savings up to 90% drive capital costs much lower than traditional processes. It’s not just CoTec that sees BSL as disruptive, both Japan’s Mitsui and Australia’s MinRes have invested in it.

Ceibo, a technology backed by BHP Group, features a low-carbon, high-recovery methodology applied to either primary or waste Cu via a sulfide heap-leaching process.

MagIron will help decarbonize the U.S. steel industry. It has a patented process that converts waste materials into high-grade iron ore concentrate, which can be used as feedstock in the growing fleet of steel-making Electric Arc Furnaces.

Can you tell readers how you came upon disruptive technologies and why in the metals & mining space?

Mining is one of the few industries that has not yet been systemically disrupted by new technologies. There isn’t an Amazon or an EBay in the mining space, but there’s no reason why one can’t be created.

CoTec takes end-of-life materials & products created with a high-carbon footprint, and manufacture low-carbon replacements. The critical bottleneck to global decarbonization will be in the availability of materials like; Cu, iron ore (to make steel), and Rare Earth Elements (“REEs“).

For example, the markets for key REEs used in electronic motors for EVs & windmills, are dominated by China. Either geopolitics or soaring prices (or both) could make select REEs very difficult to source.

We focus heavily on process technologies in three main areas; 1) recycling/reclamation 2) small particle elements, and 3) especially hard materials that are energy-intensive & costly to break down to reusuable materials.

Our opportunities come from the mining industry’s inertia. For incumbents the mentality is, if it isn’t broken, don’t fix it. We can focus on opportunities that are uneconomic using conventional methods and therefore quite inexpensive to acquire.

CoTec adds tremendous value, often with a safe modular approach, requiring far less — water, energy, consumables & capital expenditures. Our team can commercialize in 3-5 years vs. up to 18 years for conventional projects, see chart below (source: S&P Global Market Intelligence).

Importantly, whenever possible, multiple technologies will be deployed side-by-side to turbo-charge operating & cost synergies. We benefit from improved logistics, simple permitting & cost savings opportunities while delivering the greenest critical materials in the world.

Someone commented that, “CoTec’s technologies are NOT disruptive, they are just a tailings reclamation company trying to be a little greener than the next guy.” What do you say about that viewpoint?

My team respectfully disagrees! We strive to deliver technology solutions that are so low-cost, reliable, sustainable & green that there are no reasons to replace them, leaving CoTec with decades of high-margin, rapid-growth in earnings.

For instance, with economies of scale, over time, our roll-out of HyProMag in the U.S. will get even cheaper, more efficient, and easier to permit & construct.

So, not just “a little bit greener than the next guy,” in many cases a lot greener, cheaper, faster & scalable — especially if multiple technologies can be deployed side-by-side.

Can you walk us through the HyProMag technology (in layperson’s terms)? Why is it disruptive?

Sure. HyProMag has been in development for over a decade at the UK’s Univ. of Birmingham, roughly US$100M has been invested in it to date. Rare Earth magnets are required for electrical motors in EVs & Windmills, and in aerospace & defense.

China dominates this critically important supply chain, controlling up to 90% of the market. HyProMag not only bypasses China, which alone would be a great strategic outcome, it does so at much lower cost & emissions, and is scalable, enabling long-term security of supply.

Less than 5% of REE magnets are recycled as existing methods are not that efficient, environmentally-friendly, logistically simple, or low cost. We’re developing a closed-loop supply chain for REE magnets in key industries. The size of the opportunity is enormous. The U.S. Departments of Energy & Defense are interested.

HyProMag avoids the most difficult part of the process — shredding, grinding & separating magnet components — (which can be energy and labor intensive). HyProMag uses a hydrogen process to reduce electronic scrap into powder that can be used by CoTec to manufacture new REE magnets.

We consider that to be disruptive, and we hope to generate a strong EBITDA margin across a growing number of sites in the U.S.

Please give an example of how CoTec would combine technologies at, for example, a tailings site containing low-grade Cu.

Yes, that’s a good question. You mentioned Cu tailings, so let’s talk about our Ceibo segment. Ceibo has developed a process to leach low-grade primary Cu sulfides & tailings with a high throughput inorganic methodology.

Sulfide leaching targets 65%-75% recoveries. Without sulfide leaching, recoveries fall to ~30%, the upper limit for traditional acid leaching. Bolting on a complimentary technology to optimize a low-grade Cu project’s flow sheet, by increasing throughput and/or boosting recoveries, would further enhance the economics.

That would make our use of Ceibo even more compelling, and open it up to a larger universe of mining sites.

Thank you Julian for the insightful updates on CoTec. I look forward to exciting developments later this year!

Disclosures/disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about CoTec Holdings, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party, or person. The shares of CoTec Holdings are highly speculative, and not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, CoTec Holdings was an advertiser on [ER] and Peter Epstein owned no shares in the company.

Readers understand and agree that they must conduct due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.