Funded Into q2 2017, Management’s Plan? Go it Alone

There’s been talk about NexGen Energy [TSX-V: NXE] & [OTC: NXGEF] selling a minority stake to a strategic investor, 9.9% being a figure I hear mentioned. However, it’s my understanding that the Company is not actively seeking out investors. Sitting on about $33 million, NexGen is in the enviable position of not needing additional capital. It has cash for this year’s prolific drilling and funds for ongoing Pre-Feasibility Study, “PFS” level testing on the environmental, metallurgical, geotechnical & hydrogeological fronts.

I think most would agree that drilling flat out for the remainder of the year will, over time, deliver a very substantial increase in NexGen’s NI 43-101 compliant resource estimate. Including the recently announced spring drilling, the Company plans a total (some results already reported) of up to 100 new drill holes. NexGen’s prior 82 drill holes delivered 201.9 million Inferred pounds uranium.

Management believes that the Company is funded into q2 2017, so there’s no urgency to pursue the sale of a minority stake, unless under favorable terms. The Company needs neither the cash, nor the technical validation of the Arrow deposit.

Importantly, management is not overly concerned with what its 2h 2016 resource estimate might show. That’s because they’re already looking beyond that static snapshot, occurring at an arbitrary date. In the meantime, the quality of new drill targets continues to benefit from data obtained, each batch of assays informing subsequent drilling activity. The higher-grade areas continue to be better understood, allowing for more focus on them. The Company continues to report blockbuster intercepts from among the assays released this year.

Next year’s drill targets & understanding of Arrow more important than a static # of pounds

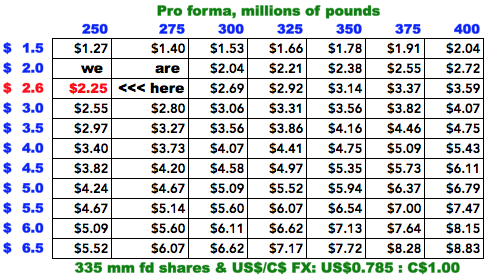

I think that the NI 43-101 compliant resource could grow to 300 million pounds, not necessarily in the Company’s 2h 2016, but …. after up to 100 new assays are plugged into the model. Still, more important will be, 1) the proportion of pounds potentially upgraded into the NI 43-101 “Indicated” category, 2) new interpretations of NexGen’s growing deposit and 3) the quality & location of new drill targets. There’s no looking backwards for a world-class deposit like Arrow. The following obligatory chart shows where we are on the popular EV(US$)/lb. spectrum. Share values have been discounted back 1 year at 12%.

For those who believe there’s a lot of hype in the NexGen story, please focus on these facts. Think about what’s changed in just the past 4 months:

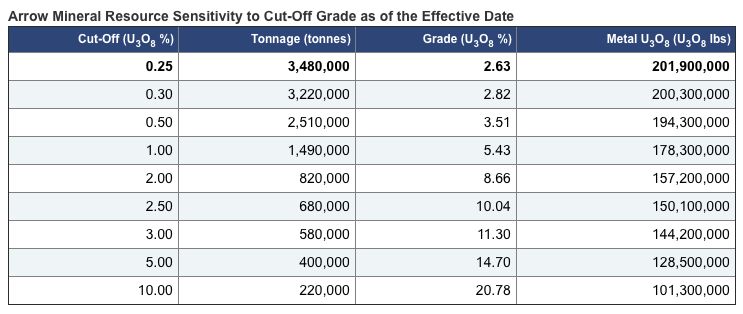

FACT: delivery of a NI 43-101 compliant maiden resource estimate, 201.9 mm Inferred lbs. @2.63% (0.25% cut-off) incl. 128.5 mm lbs. @ 5.0% cut-off & A2 high-grade domain of 120.5 mm Inferred pounds @ 13.26%. The maiden resource estimate includes holes to October 2015, it does not include an additional 40 drill holes completed through April 18th.

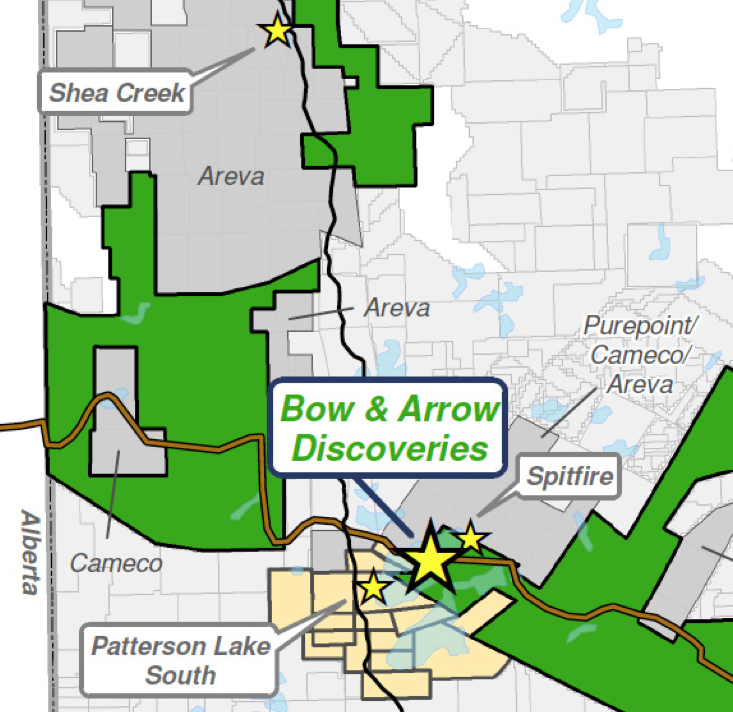

FACT: Rook 1’s Arrow deposit is partially de-risked post maiden resource estimate and strong drill results since. Arrow is now the largest undeveloped uranium deposit in the basin, open in all directions and at depth. Also, there’s 4km of untested strike length to the NE & 3km of untested strike length to the SW.

FACT: intersection of off-scale mineralization in a 180m step-out along strike to the SW of Arrow’s grade shell. Hole AR-16-77c2 represents a 25 m down-dip expansion of the current A2 high-grade domain, extending Arrow along strike to 865 m and laterally by 40 m to 275 m. There’s already been at least 11 holes drilled into the A2 Sub-Zone this year vs. 7 in 2015.

Regarding recent drill results, CEO Curyer commented,

“This winter program at Arrow has been incredibly successful. The objectives for the winter 2016 drilling program have been met on all fronts and there are many assays still pending. The decision to continue drilling uninterrupted is in direct response to the high level of success we have had with the infill of the A2 High-Grade Domain and the newly discovered southwest extension at Arrow. Further, the initiative to construct the all weather road to the Project reflects our commitment to exceptionally high standards of operations incorporating safety as our priority as we progress Arrow along its development path.”

FACT: AR-16-63c2 intersected 42.0 m at 15.20% & an additional 46.5 m at 12.99%, in the higher-grade A2 sub-zone. Including 3.5 m of un-mineralized core separating the 2 intervals, AR-16-63c2 returned 92.0 m at 13.51%, for a grade x thickness (“GT”) of 1,243. Further, holes AR-16-63c2 & AR-26-64c2 extend outside the defined high-grade domain grade shell, which, as mentioned, hosts 120.5 mm Inferred lbs. @ 13.26%. These 2 holes are among the most strongly mineralized at Arrow to date, and are not yet included in the resource estimate.

FACT: drill hole AR-16-78c4 returned 37.4 m of off-scale radioactivity, expanding the higher-grade A2 sub-zone. AR-16-78c4 also identified anomalous radioactivity 1.3 km NE of Arrow, in an area named Cannon. Cannon has very similar geophysical, lithological & alteration features to the Arrow deposit. On a radioactivity basis, AR-16-78c4 ranks as one of the best holes ever drilled at Arrow. Importantly, the high-grade mineralization was predominately intersected outside the current boundary of the A2 high-grade domain.

There’s a range of opinions regarding the possibility of a NexGen Energy takeout. Some think it’s a foregone conclusion, possibly as soon as this year. Others believe potential suitors have no reason to move anytime soon, if at all. Given Arrow’s early-stage, and a uranium price stubbornly below US$30/lb., it’s understandable that some feel this way. Evidence of a truly awful uranium market can be found in Cameco’s April 21st announcement that it’s putting Rabbit Lake on care & maintenance. Rabbit Lake accounts for roughly 4% of annual production, and it will very likely be down for at least 2 years.

Some think this action is a reason why Cameco will not be a suitor of NexGen, because it has plenty of standby capacity as is. With Rabbit Lake going offline, horrible uranium market sentiment just sank even lower. The prospect of raising capital to explore / develop or initiate / increase production on reasonable terms, is bleak. NexGen needs no influx of cash, and its fundamental valuation marches higher as the size & quality (Indicated vs. Inferred) of its estimated resource increases, and associated exploration risk at Arrow decreases.

Consider NexGen’s roughly C$30 million capital budget. In a scenario where NexGen is valued by the market at US$3 [EV/lb.], a hypothetical move from a 201.9 to a 300 million pound resource estimate, would add C$375 million (assuming C$0.785 FX rate) in equity market value. That would be a whopping 12 times return on investment. Looked at another way, the same C$30 million, would generate a break-even market cap gain of C$30 million, if ~8 million incremental pounds were booked. Just 8 million pounds, from upwards of 100 new drill holes.

Many have succumbed to the lure of the single-tracked takeout narrative, myself included. I believe that the above mentioned facts alone make for a highly compelling story. All of the above information can easily be found by reviewing the Company’s corporate presentation and this year’s press releases.

Given that TradeTech recently quoted the uranium spot price as low as $25.5/lb., ($27.5/lb. on April 29th) and the Rabbit Lake news, I’m backing away from a takeout scenario being front and center. A takeout thesis seems to foster short-term thinking, to the detriment of a management team that has consistently said they intend to advance the Arrow deposit through to production.

Conclusion

Driving shareholder value through aggressive drilling and optimization of engineering studies, for as long as possible, remains the game plan. Shareholders should be thrilled. The drill bit’s leverage on NexGen’s potential valuation and share price is outstanding. Time and time again, from day 1, drilling results from NexGen’s expert technical team have exceeded expectations. I wholeheartedly agree with the Company’s strategy and am more than happy to hold my NXE shares until Curyer sells his.

Disclosures: Readers fully understand and agree that nothing contained in this article authored by Peter Epstein, from EpsteinResearch.com [ER], including but not limited to, analysis, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered in any way whatsoever, implicit or explicit investment advice or guidance. Further, nothing contained herein is a recommendation or solicitation to buy, or sell any security. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer and does not perform market making activities. The shares of NexGen Energy are highly speculative, not suitable for all investors. Readers are urged to consult with their own financial advisors before making investment decisions.

At the time this article was posted, Peter Epstein owned shares of NexGen Energy and the Company was a sponsor of EpsteinResearch.com

Any comparison between or among stocks is for illustrative purposes only, and should not be taken as fact or relied upon. Readers understand and agree that they must conduct their own investment due diligence. While the author believes that he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein and [ER] is not responsible for any perceived, or actual, errors including, but not limited to, analysis, commentary, opinions, views, assumptions, reported facts & financial calculations, or for investment actions taken by readers.