After being the best commodity play for much of 2021 & 2022, then falling precipitously in 2023, lithium (“Li“) is now the contrarian investment of 2024, albeit looking stronger just this past week or two.

The spot price in China has rallied +13.6% from 95.5k yuan/tonne to 108.5k/t = ~US$15.1k/t. (March 4, investing.com). Platts is showing spodumene concentrate (6.0% Li2O) price up +15.2% from US$850 to $980/t.

Was last month’s low of US$13.3k/t the bottom? It sure seems like it, but I thought $25,000, $20,000 & $15,000/t were bottoms! For a more reliable long-term view of battery-quality Li carbonate pricing, SQM is the place to look. Its 4Q/23 avg. Li contract price was ~$16k/t.

SQM’s trailing 1, 2, 3, 4, 5, 6, & 7-yr. avg. quarterly contract prices are; US$32.5k, $42.1k, $31.0k, $24.8k, $21.2k, $20.0k & $18.8k, respectively. The uptick in Li prices has launched many juniors much higher. In the chart below are the Top-12 performing Li juniors, up an average of +90% from recent lows.

On March 4th Frontier Lithium announced an investment from Japan’s Mitsubishi for 25% of the Company. Frontier solves its funding needs for a few years and maintains 75% ownership. This is great news for Canadian Li juniors, showing that a wide range of groups are looking to secure Li assets.

In Canada there is a small handful of world-class hard rock Li projects owned by; Frontier, Patriot Battery Metals [PMET], Arcadium Lithium, Sayona Mining, Winsome Resources & Li-FT Power (TSX-v: LIFT) / (OTC: LIFFF). {see new corp. presentation}

Earlier I mentioned a dozen companies up an average of +90% from recent lows… By contrast, Li-FT is up just 6% and is 59% below its 52-week high & 75% below its all-time high. This makes no sense for a company with a Top-4 hard rock Li project in N. America.

Although early stage, Li-FT owns 100% of a large project in ultra-safe Canada, fast becoming a battery materials powerhouse for its simple, low-cost & low-technical risk hard rock Li endowment. In the chart above I compare Li-FT’s Yellowknife to other world-class, (early-stage) hard rock projects.

It compares reasonably well across all metrics, but is valued at C$50/tonne of Li Carbonate Equiv. (“LCE“) vs. an average of $216/t. from PMET, Azure Minerals & Wildcat Resources.

If, as planned, Li-FT delivers a 100M+ tonne maiden resource estimate (“MRE“) grading 1.10%+ Li2O by 12/31/24, that will be a globally significant Li project — not just in Canada or N. America — in the world. The 100M+ tonnes will come from 8 of 13 pegmatite systems, seven of the eight are road-accessible.

Of 240 Canadian & Australian-listed companies I’m tracking with Li properties in Canada, fewer than 10% have announced MREs. Looking beyond Canada, there are < 50 pre-production, hard rock Li resources, (> 10M tonnes), among publicly-listed companies.

Last year, PMET tabled a 109M tonne MRE at 1.42% Li2O and could end up with up to 350M tonnes at its Corvette project in Quebec. Li-FT is 12-18 months behind PMET, but could have 150-175M tonnes at the 100%-owned Yellowknife project in the Northwest Territories (“NWT“).

PMET is valued 5x higher than Li-FT (on an EV/tonne of LCE basis). Based on both companies’ flagship projects, I believe Li-FT should be valued at a 3x differential. To be clear, PMET is not overvalued, Li-FT is undervalued.

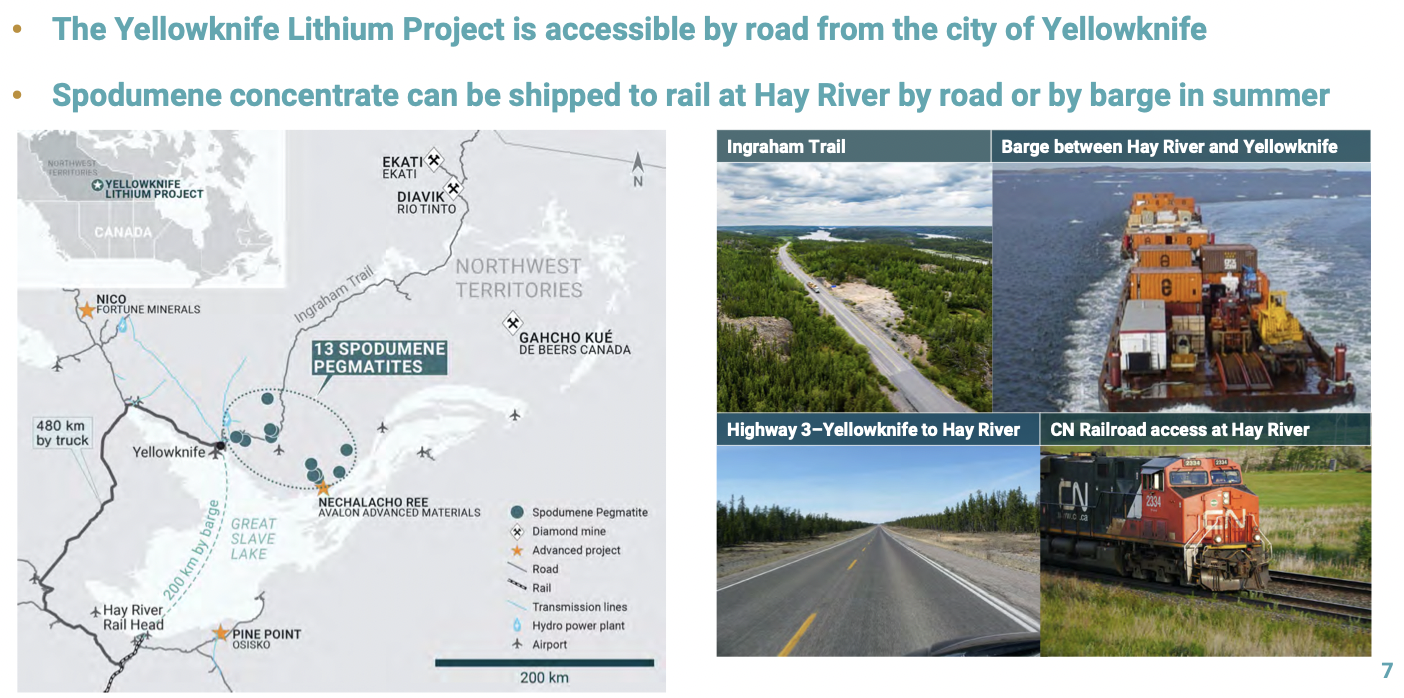

The Yellowknife project is well positioned in the NWT, remote, but no more so than mining projects in northern Quebec, Ontario & Manitoba. Rio Tinto has substantial diamond mines north of Yellowknife — operating for decades — but shutting down in the next 5-10 years.

A paved highway from Yellowknife comes within several km of seven meaningful Li deposits held by Li-FT. Trucking around, and/or barging across, Great Slave Lake (~4 months out of the year) to a rail line at Hay River is expected to be straightforward & low-cost, especially the barging part.

From Hay River, concentrate can be sent by train to a port at Prince Rupert or further south to the U.S.

For Li-FT, consistent drill results are baked into expectations. Investors might feel that only a strong MRE (in 10 months) can get the stock moving again. I disagree, relative value matters, not just Li-FT vs. PMET, or Li-FT vs. Frontier, but Li-FT vs. other juniors around the world.

Within 12-15 months, Li-FT will have a Preliminary Economic Assessment (“PEA“) on Yellowknife. If the Li market is stronger, as I believe it will be, a wave of M&A could be upon us. I think there’s a good possibility that PMET will be acquired next year.

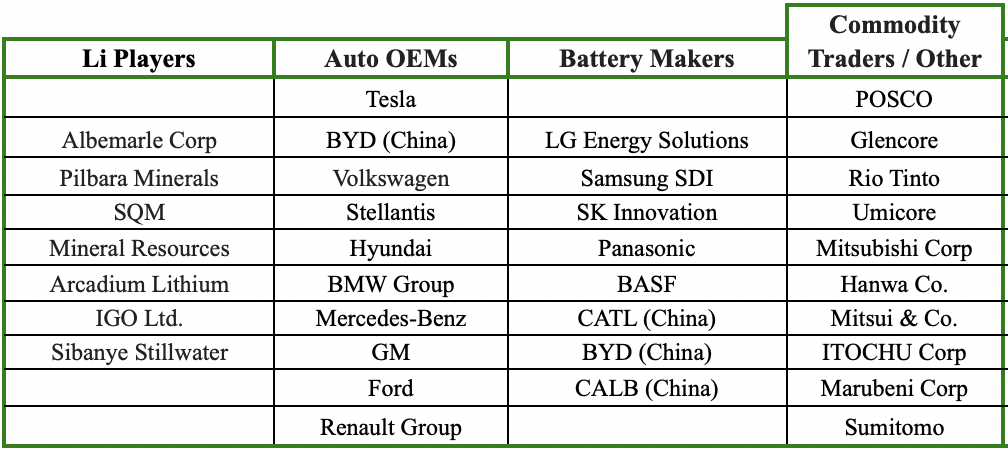

The list of potential acquirers for PMET, but also Li-FT & Winsome Resources is long, see the above chart. Excluding Chinese groups, there are still 32 names, and the list doesn’t include Major Oil & Gas companies, some of which are thought to be interested in Li.

If/when PMET is acquired, all eyes will turn to Li-FT as one of a few big plays in Canada. Readers should note, Li-FT’s other project in the Northwest Territories, the 100%-owned Cali project with a spodumene-bearing pegmatite dyke system up to 1,200 m x 60 m x 300 m deep.

Cali has the potential to be 50M tonnes, but there’s been no drilling on it. Last year, sampling & mapping was done to establish a rough estimate of grade & tonnage. Fifty million tonnes would be a Top-8 hard rock resource in Canada, yet Cali is barely noticed in the shadow of Yellowknife.

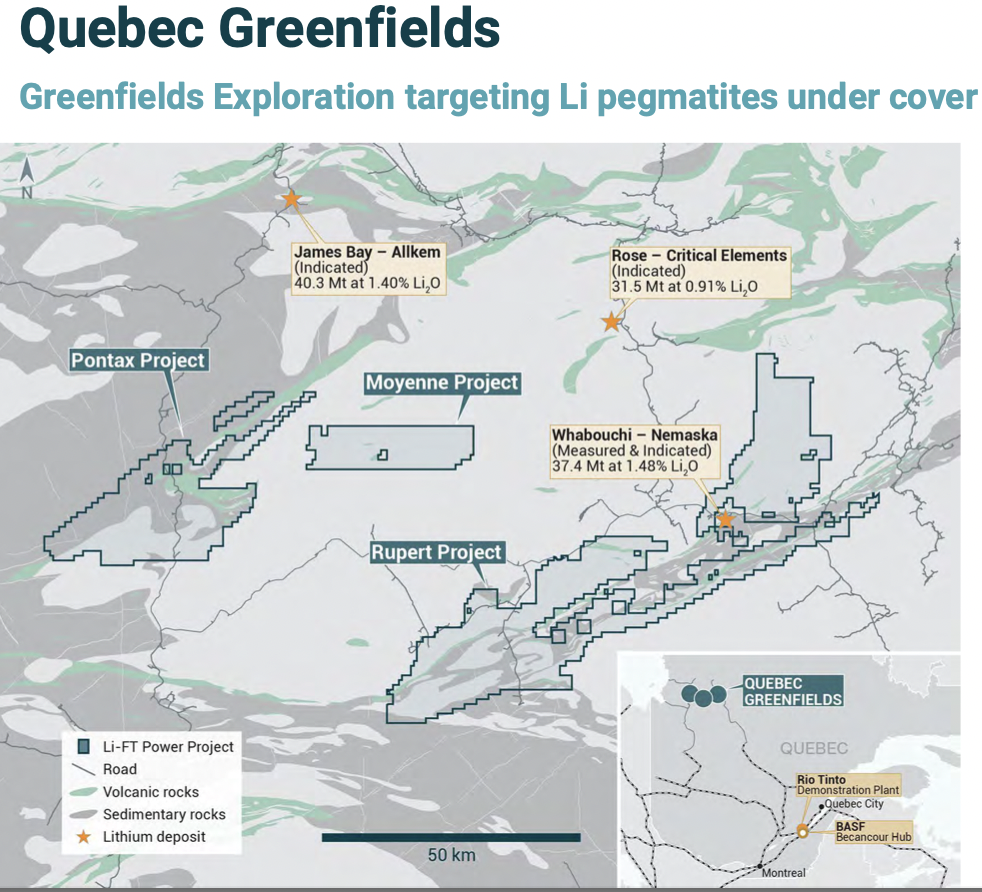

Importantly, the Company also has a large, early-stage, land package in Quebec. The 100%-owned [Rupert, Moyenne & Pontax] properties span 228,237 hectares.

Rupert (141,572 ha) surrounds Nemaska’s advanced-stage Whabouchi project {see map below}. As Li market sentiment improves, the value of these properties will become more meaningful. How meaningful?

They are in the heart of the James Bay region, I see no reason why they couldn’t be worth a total of C$50M, which is a lot compared to the Company’s enterprise value {market cap + debt – cash} of ~$153M.

To say that C$8B market cap Arcadium Lithium [formed in the merger of Livent & Allkem], 50% owner of Whabouchi, and 100% owner of the James Bay project {see map} should care about Li-FT’s Quebec projects would be a gross understatement.

Moyenne at 25,145 ha, about the same size as the Yellowknife project, and larger than PMET’s 21,400 ha Corvette. It’s within 50-60 km of James Bay & Critical Elements’ Rose projects.

Pontax is 61,520 ha and has the most extensive Li anomaly of the Quebec properties. It has highway access and is < 50 km south of the James Bay project. Any of the three Quebec prospects have the potential to be company-makers if farmed out to third parties.

Li-FT Power seems cheap vs. several Li peers, despite it having a world-class, Top-4 hard rock Li project in N. America AND very significant land holdings in Quebec, which should be of interest to many companies. Unlike other juniors, Li-FT has not rallied.

Of course, that fact alone does not necessarily mean it will rally — but, I continue to love the relative value at a share price of C$4.33, and enterprise value of just C$153M. {see new corp. presentation}

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Li-FT Power, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Li-FT Power are highly speculative, not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, Li-FT Power was an advertiser on [ER] and Peter Epstein owned shares in the company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, or reported facts.