For several months, investors in Sassy Resources (CSE: SASY) / (OTCQB: SSRYF) have been waiting for all the drill results from the sizable, 100%-owned, flagship Foremore project in the Eskay Camp, at the heart of the Golden Triangle in northwestern B.C. 11 of 17 holes have been reported, along with the highlights of > 1,000 samples.

Nicobat to be spun-out for shares in exciting new battery metals play

As we wait, shareholders have been advised to watch out for news on non-core asset Nicobat and for possible acquisitions outside the Golden Triangle. Well, that news arrived last week. Sassy is close to monetizing Nicobat by optioning it (for shares & a multi-year work commitment) to a private Canadian battery metals junior.

That company plans to list on the CSE in coming months. Management is optimistic about the prospects for battery metals, and Sassy would hold a meaningful position in this prospective play.

While the Nicobat news is very good, the more exciting development is that Sassy has formed a wholly-owned subsidiary, Gander Gold Corp., (“GGC“) to pursue opportunities in the province of Newfoundland and Labrador (“NF&L“). CEO Mark Scott has started in NF&L by optioning eight promising claim blocks from Vulcan Minerals.

NF&L is one of the most exciting exploration districts in Canada. It’s the focus of a mini gold rush. Much of the action is in the Central Newfoundland Gold Belt, a large region stretching across the island, ~250 km in length. For centuries NF&L was mined for base metals, but not until much more recently has anyone considered focusing on gold.

Sassy enters mini gold rush in Newfoundland, still at early-stage

In the 1980’s Noranda did a lot of drilling all over NF&L, but in many cases (reportedly) did not bother assaying for gold! As New Found Gold’s (NFG) corporate presentation explains, “the Fosterville epizonal high-grade model was not understood at that time.”

GGC will enable Sassy to pursue options to generate shareholder value through meaningful project diversification outside the Eskay Camp, with minimal shareholder dilution. NF&L offers under-explored opportunities, high-grade gold/silver + base metal potential, relatively low-cost drilling and the ability to explore year-round.

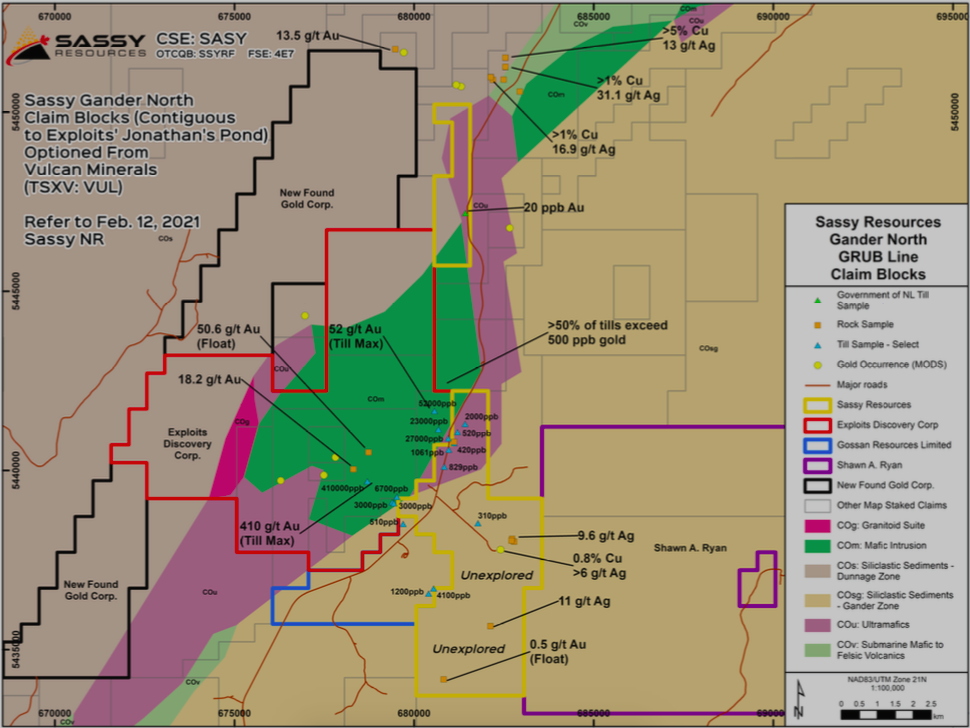

Management plans to execute reconnaissance / orientation diamond drilling on drill-ready targets at Gander East this Spring. Gander East adjoins Jonathan’s Pond, where some of the highest grade till anomalies ever discovered in NF&L (up to 410 g/t Au!) were found. That mineralization trends onto parts of Sassy’s optioned property. The Company now controls the closest claim block to NFG’s Eastern Pond discovery.

Exploration programs this year will cover the rest of that property, plus the other seven blocks — plus any new properties added to the portfolio — with airborne geophysical surveys & pattern soil/till sampling & prospecting.

Although not mentioned in the press release, it seems reasonable to wonder if one day GGC might be spun out into its own publicly-traded vehicle. Perhaps not anytime soon, and not without some exploration successes, but something to think about.

Mr. Mark Scott, President & CEO, commented:

“We’ve taken some creative, forward-looking steps aimed at year-long value creation with Sassy establishing a major foothold in the prolific Eskay & Newfoundland mineral districts during transformational periods for each region. The Gander Gold subsidiary gives us various attractive options to leverage success for our shareholders.”

Sassy entered into an option agreement with Vulcan Minerals to acquire a 100% interest in eight claim blocks, (624 claims / 156 sq. km) including the drill-ready Gander North area, a compelling target intersected by a major regional fault zone (the GRUB Line) ~15 km northeast of NFG’s tremendous new discovery — the Keats zone on its Queensway project.

NF&L stars Marathon Gold + New Found Gold leading the way….

In late 2019, NFG hit 93 g/t Au over 19 m and has had many other high & very-high-grade intercepts since then. Eight rigs are now turning as part of a 200k meter grid drill program. NFG’s Keats zone is one of the most significant discoveries in Canada of the past 20 years. (NFG market cap = $500M, pre-maiden resource). 200k m will focus a lot of attention on NF&L!

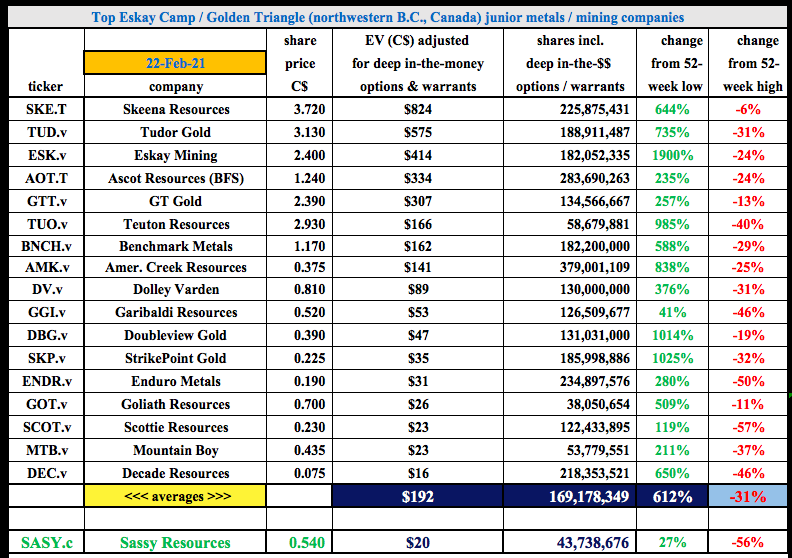

NFG’s Queensway project ranks among the top 5 pre-maiden resource juniors in Canada, along with projects owned by Great Bear Resources in the high-grade Red Lake mining district in Ontario (GBR market cap = $800M) and Eskay Mining’s (ESK) 50,000+ hectares near the center of the Golden Triangle (ESK market cap = $375M).

Since NFG’s discovery, a better understanding of the Gander Gold Belt’s blue-sky potential is emerging, making Sassy’s untested Gander North and its other claim blocks, highly prospective. Near Gander North’s western & northern boundaries, there are some extremely high gold-in-till anomalies.

Over a 4-yr. period, Sassy will pay $400,000 in cash to Vulcan, incur $2M in exploration expenditures and issue 2.5 million shares. Vulcan will retain a 3.0% NSR on the entire claims package, of which Sassy can repurchase 1.5% for $2M + 500,000 shares.

Marathon Gold has an Enterprise Value (“EV“) {market cap + debt – cash} of ~C$560M. Its single project, at PFS-stage, is in central NF&L. The Valentine project is expected to reach production within three years. At US$1,550/oz. gold, the after-tax NPV(5%) of the 12-yr. mine = C$671M / [48.8% IRR].

The AISC = US$739/oz. (bottom quartile). An NPV of C$671M is 2.5x the project’s upfront cap-ex of C$272M, making it one of the best in North America, which is why Marathon enjoys a premium valuation; EV/NAV = 0.83x.

Sassy’s Gander Gold subsidiary alone could be worth $20M+

There are no Major or mid-tier gold producers in NF&L. However, I would not be surprised to see Marathon & New Found Gold be acquired. After that, there are roughly three dozen juniors with gold prospects in NF&L, ~12 of which have market caps between $20-40M, one ~$55M.

If management can deliver good drill results, I think it’s reasonable to think that Sassy’s NF&L properties & exploration activities, (the assets held in GGC), could support a $20M+ valuation. Given Sassy’s tight capital structure, a $20M valuation for GGC alone would be worth ~$0.50 per Sassy share. Sassy’s shares are currently at $0.54.

And, if Sassy can conduct multiple drill programs that hit attractive grades, with multi-meter interval widths, then a valuation north of $25-30M would be reasonable. Having said that, it might be necessary for Sassy to spin out GGC for its value to be more fully recognized by the market.

There’s more news to come from Sassy in NF&L. Management continues to review possible farm-ins & acquisitions of exciting properties / projects under attractive deal terms. And exploration / prospecting will be starting this Spring, with the goal of identifying drill targets for 2H 2021.

The Copper price soaring is great news for Sassy Resources!

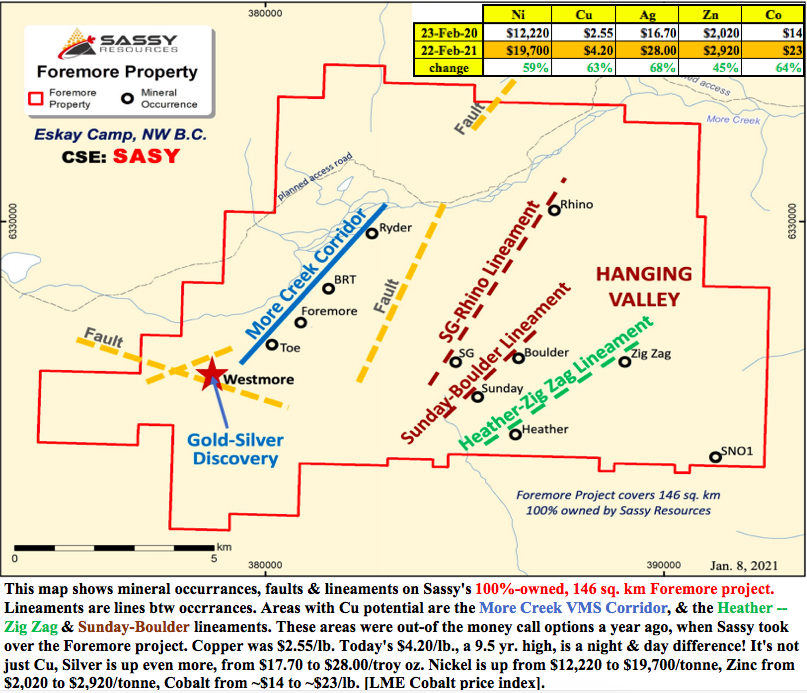

Finally, with the #copper price soaring, late last week surpassing $4.00/lb. for the first time in nine years, readers are reminded that Sassy’s flagship Foremore project has considerable copper showings that warrant further attention. Copper is now at $4.15/lb., a 9.5 year high. I asked CEO Scott about Sassy’s Cu prospects, he provided the following quote,

“There’s significant copper potential at the Foremore project, including along the > 5 km More Creek VMS Corridor, and on several potentially multi-km long lineaments in the Hanging Valley. In 2019, the Heather showing produced a grab sample containing 21.4% Cu. The province of Newfoundland and Labrador has a long history of Cu & Zn exploration & production.

We will certainly be sampling for these metals as we explore our new holdings there. Most of the properties we have optioned have some form of anomalous Cu soil / till / lake-sediment / stream-sediment / outcrop samples, together with known gold / pathfinder occurrences and favorable structural environments.“

Conclusion

An investment in Sassy Resources (CSE: SASY) / (OTCQB: SSRYF) gives investors exposure to two world-class, gold / silver projects. Both have copper kickers. Both are in safe, prolific jurisdictions. Both have high-grade potential. Both are sizable footprints (Foremore = 14,600 sq. km / Gander Gold Corp. 15,600 sq. km to start, expected to grow).

Management, led by CEO Mark Scott, is top-tier, especially for a company with an EV of just C$20M. The pullback in the gold price from over $2,070/oz. in early August 2020, to about $1,810/oz. today, has caused many top-quality gold juniors to trade 40%-60% lower from 52-week highs.

At $0.54/shr., Sassy is down 56%. Freegold Ventures & Fury Gold Mines are each down 63%, producers OceanaGold Corp. & Victoria Gold are down 53% & 44%. So, Sassy is not alone in this market sell-off.

Readers are encouraged to dig deeper into the Sassy Resources story, review recent press releases, and watch for upcoming news on both the NF&L strategy and the flagship Foremore project. With Copper, Zinc, Silver, Nickel & Cobalt up between 45%-68% from a year ago, it makes no sense for Sassy shares to be down so much from a high of $1.24.

At current levels, the Company’s EV is just $20M. This valuation could be a very good entry point for readers with an appetite for high risk/high potential reward investments.

Disclosures: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Sassy Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Sassy Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Sassy Resources was an advertiser on [ER] and Peter Epstein owned shares & warrants in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.