I have been impressed by CEO Jordan Trimble’s command of the uranium sector, he puts out the best market commentary in his press releases, and his team has a great corporate presentation. Skyharbour Resources (TSX-V: SYH) (Frankfurt: SC1P) (OTCQB: SYHBF) is well positioned with a strong flagship project in its 100% owned Moore project, and 5 other projects that are either optioned to partners, or in the process of potentially being optioned. Please continue reading for more information on this exciting company. {see latest press releases}

You have 6 properties in the eastern part of the Athabasca basin. Tell us about your most important project.

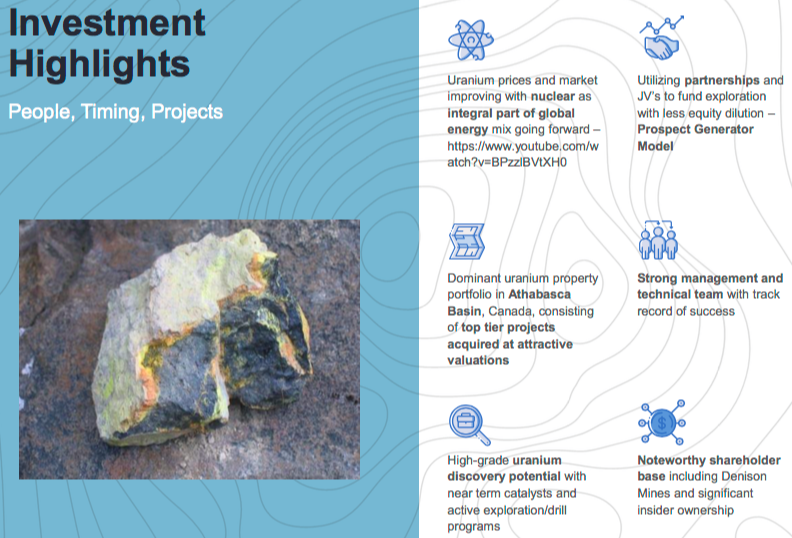

Skyharbour Resources (TSX-V: SYH) (Frankfurt: SC1P) (OTCQB: SYHBF) is a preeminent uranium exploration Company with projects in the prolific Athabasca Basin of Saskatchewan, Canada, ranked the best global mining jurisdiction by the Fraser Institute in 2017. The Company has acquired top tier exploration projects at attractive valuations culminating in 6 uranium properties totaling approx. 200,000 hectares.

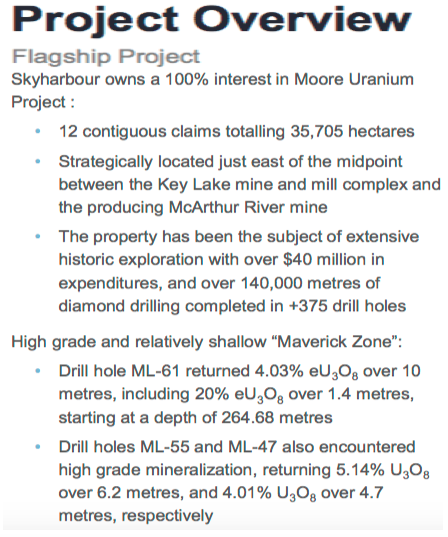

In July 2016, Skyharbour secured an option from Denison Mines (TSX: DML), a large strategic shareholder & partner of our’s, to acquire a 100% Interest in the Moore Uranium project. Skyharbour now owns 100% of this flagship project, which hosts the high grade Maverick Zonewhere previous drilling interested grades as high as 21% U3O8 over 1.5m.

There’s still strong discovery potential at the project in the sandstone and below the unconformity in the underlying basement rock, where little historical drilling has been done (recent discoveries like NexGen and Fission’s deposits are basement hosted). Skyharbour just commenced a 3,000m drill program to further test this, which will provide news flow in the near term. The Company is run by a strong management & geological team, who are major shareholders.

Can you provide some commentary on the uranium market?

The uranium market has shown notable signs of recovery with increasing uranium prices and improving sentiment. Analysts that cover the sector have stated that this could be a sustained upswing, as they are currently seeing some of the best fundamentals since pre-Fukushima. That should be supportive of higher uranium prices, as a major supply-side response is playing out while the sticky demand-side continues to improve.

Uranium production is on the decline and expected to be just 135 million lbs U3O8 in 2019 given recent closures & project deferrals, while demand continues to rise and is expected to be approx. 194 million lbs. The spot uranium price is just ~$27/lb. U3O8 which is still well below the average all-in global cost of production. Significant price appreciation is needed to justify production as well as developing new mines to meet growing global demand.

Mine closures and production curtailments continue to dominate headlines while U.S. lawmakers are starting to take notice of external pressures on what is deemed a strategic industry. Major production cuts and depleting mine reserves appear to be working their way into the uranium market, driving prices higher. The two largest producers, Cameco & KazAtomProm, announced large supply cuts in 2017 & 2018, including Cameco’s suspension of the world’s largest uranium mine, McArthur River, as well as KazAtomProm cutting 20% of its production over a three year period.

Additionally, several new uranium holding companies and funds have emerged including Yellow Cake PLC, Uranium Trading Corp. and Tribeca Capital Partners, which have collectively raised hundreds of millions of dollars to purchase physical material, effectively taking further spot supply from circulation. Lastly, Cameco recently announced plans to purchase 11-15 million lbs. of uranium directly in the spot market through 2019 to fulfill their contracts.

On the demand side, there are 450 operating nuclear reactors and ~50 new reactors under construction globally. China continues to be at the forefront and has the largest pipeline, including 45 operating reactors, ~15 under construction and 213 ordered, planned or proposed. According to the World Nuclear Association, at the end of 2018, just 4.2% of China’s electricity came from nuclear power. Officials want to triple that number by 2030. The situation in Japan finally seems to be improving with 9 reactors in full operation with several more coming back online this year, up from 3 in 2016.

What are Skyharbour’s 2nd & 3rd most important projects?

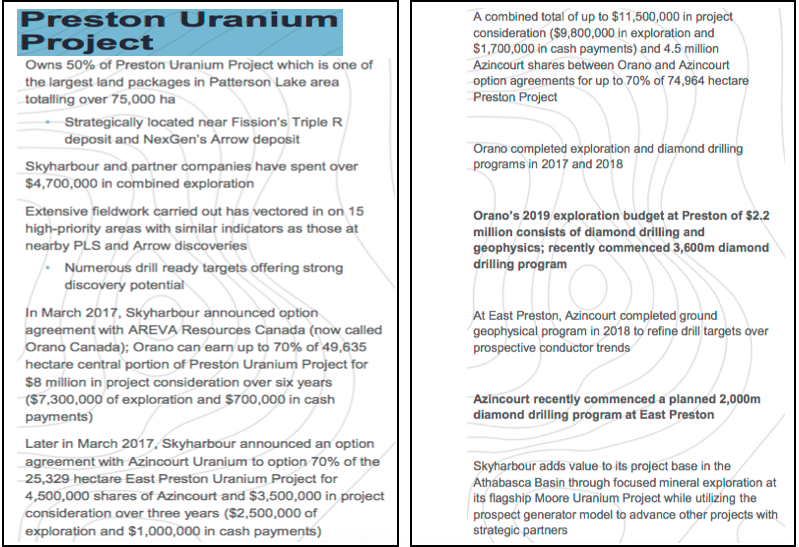

While focused on our core strategy as a discovery-driven exploration company at the Moore Project, Skyharbour also employs the prospect generator model to advance its other projects in the Basin. The Preston and East Preston properties are important for shareholders, as both are being actively drilled this year by partners Orano Canada Inc. (previously AREVA – France’s largest nuclear & uranium mining company) and Azincourt Energy.

Combined, the Preston projects comprise a large 74,965 hectare (185,164 acre) land position, strategically located to the south of, and adjacent to, NexGen’s Rook 1 project. It is also proximal to Fission Uranium’s (TSX: FCU) Patterson Lake South project.

As part of our prospect generation strategy, we optioned 70% of Preston to Orano who can earn up to 70% by spending up to $8 million (up to $7,300,000 of exploration work programs & $700,000 in cash payments) over six years. Orano is carrying out $2.2 million in drilling & exploration this year alone, which will generate additional news flow for Skyharbour.

The Company also entered into an agreement with Azincourt whereby it has an earn-in option to acquire 70% in the East Preston project. They have to issue shares, contribute cash and they have exploration expenditure requirements totaling up to $3.5 million ($1 million in cash payments & $2.5-million in exploration expenditures) over a 3-year period. Azincourt just commenced a drill program at East Preston.

The Company also owns a 100% interest in the Falcon Point Uranium project on the eastern perimeter of the Basin, which contains a NI 43-101 Inferred resource totaling 7.0 million pounds of U3O8 at 0.03%, plus 5.3 million pounds of ThO2 (thorium) at 0.023%. The project also hosts a high-grade surface showing with grab samples of up to 68% U3O8 from a massive pitchblende vein, the source of which has yet to be discovered.

Can you summarize the significant amount of drilling being done this year on your properties, both internally and by your partners?

Skyharbour plans to carry out exploration & drilling programs at our flagship Moore project over the course of the year. Given the success of the 2017/2018 drilling programs, the Company recently commenced a winter diamond drilling program of a minimum of 3000m. The Moore project will provide steady news flow over coming months, supplemented by news from partner-funded projects and potential prospect generator transactions. Skyharbour’s strategic partner Orano has commenced its 2019 winter diamond drilling program consisting of 11 to 15 holes for a total of about 3,600m on the Preston Project.

More recently, Azincourt announced that it has commenced drilling at Skyharbour’s East Preston Uranium project consisting of 2,000 – 2,500m. So, among the 3 drill programs, the Company is poised to enjoy news flow from approx. 9,000 meters of drilling, and we highlight that the bulk of this drilling is partner funded.

Uranium is one element where a strong & experienced management team & Board is critical. Does Skyharbour make the grade?

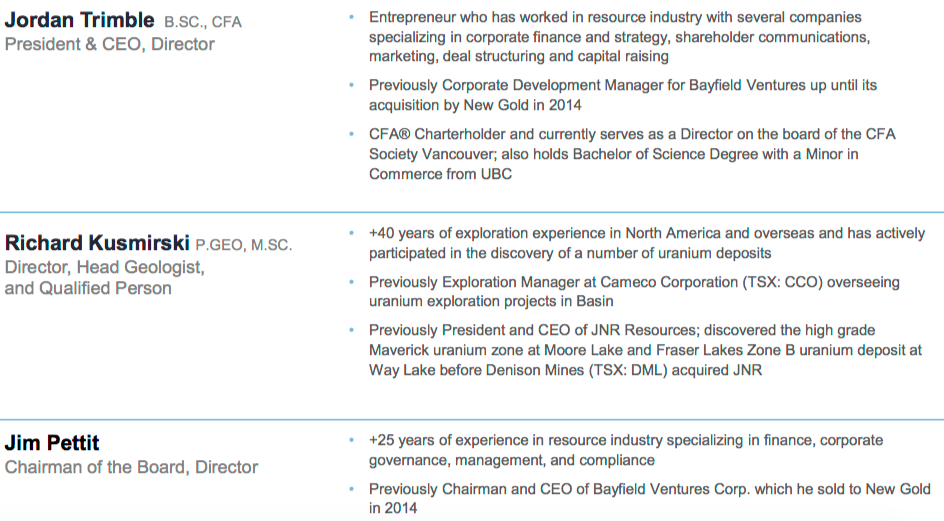

Yes, we do! Skyharbour is managed by a team with vast experience in capital markets, mineral exploration & discovery & mine development. Specifically, Skyharbour’s technical team is led by Rick Kusmirski, P.Geo, M.Sc., Head of our Advisory Board, who has over 40 years’ of global exploration experience. Rick actively participated in the discovery of a number of uranium, gold & base metal deposits. He was Exploration Manager for Cameco Corporation’s (TSX: CCO) exploration projects in the Athabasca Basin.

In 1999, Rick joined JNR Resources becoming VP of Exploration in 2000. Subsequently, he directed the exploration program that led to the discovery of the Maverick Zone on the Moore Lake uranium JV with partner Kennecott Canada. In 2013, Denison Mines acquired JNR in a friendly all-share take-over bid.

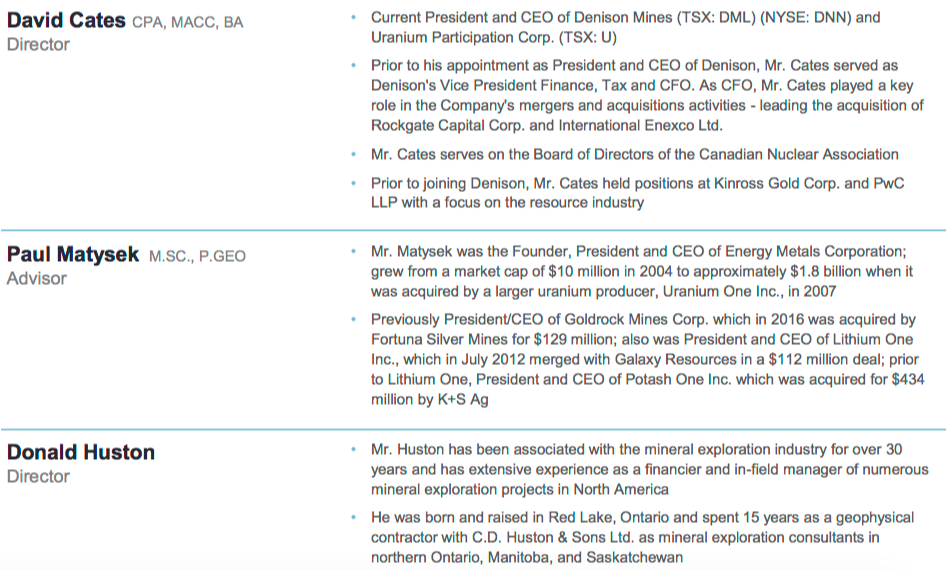

Our largest shareholder, Denison Mines, is represented by their President & CEO David Cates. He is also President & CEO of Uranium Participation Corp (TSX: U). Prior to being appointed to those positions, Mr. Cates served as Denison’s VP Finance, Tax and as CFO. Mr. Cates played a key role in M&A activities – leading the acquisition of Rockgate Capital Corp. & International Enexco Ltd. Prior to that, Mr. Cates held positions at Kinross Gold Corp. and PwC LLP with a focus on the resource industry.

Paul Matysek is a large shareholder & Strategic Advisor. He’s a mining entrepreneur, professional geochemist & geologist, with over 35 years’ experience. He was the Founder & CEO of Energy Metals Corporation, increasing its market cap from C$10 million to approx. C$1.8 billion when it was acquired by Uranium One Inc., in 2007. Last year, Mr. Matysek, as Chairman, successfully sold Lithium X for $265M to NextView in Hong Kong. He has built and sold several other mining companies over the course of his career.

Finally, I have been running the Company as the President & CEO since it started as a uranium company in 2013. I have worked in the resource industry with numerous TSX Venture-listed companies specializing in corporate finance & strategy, shareholder communications, marketing, deal structuring & capital raising. Prior to Skyharbour, I managed Corporate Development for Bayfield Ventures, a gold company with projects in Ontario, which was acquired by New Gold (TSX: NGD) in 2014.

I hold a Bachelor of Science Degree from UBC, and I am a CFA Charterholder, currently serving as a Director of the CFA Society Vancouver. My Chairman Jim Pettit brings over 30 years’ experience within the industry specializing in finance, corporate governance, management & compliance. He was previously Chairman & CEO of Bayfield Ventures Corp.

Can you talk about your largest shareholders, what percentage of the Company does management own?

Denison Mines is our largest shareholder and a strategic partner. There are several other noteworthy shareholders including; Marin Katusa and the KCR Fund, OTP Fund Management, Extract Capital, Sachem Cove Partners, Paul Matysek, Doug Casey & Jeff Phillips. This group, in addition to management & insiders, controls a large portion of the Company’s outstanding shares.

Your corporate presentation mentions several high-grade discoveries by peers. What makes your technical team believe there’s a reasonable chance of delineating a high-grade resource at the Moore project?

NexGen Energy, Fission Uranium, Alpha Minerals, Denison Mines & Hathor Exploration are just a few examples of successful uranium discovery stories in the Athabasca Basin.

It’s worth noting that traditional Athabasca exploration involved rudimentary geophysical targeting and widely spaced vertical drill holes, which led to a high cost of discovery and a low probability of success. However, new exploration techniques & strategies have led to new discoveries through new target types and improved targeting methodologies, leading to lower costs and a higher probability of success. Skyharbour is utilizing these new techniques and is entering overlooked projects, at low cost, with robust discovery potential.

Does Skyharbour require blockbuster 10%+ Uranium grades at Moore to host an economic deposit? If not, what approximate grade might be needed?

No, uranium is a valuable commodity, especially compared to traditional metals. For example, 1% U3O8 = 20.0 g/t Gold or 1,404 g/t Silver, or 13.7% Copper, or 28% Zinc. Furthermore, there are new innovative mining methods being proposed for Athabasca Basin deposits that could bring costs down including SABRE and ISR mining methods.

If a lot more high-grade Uranium were to be found at Moore, is the Maverick zone alone large enough to potentially host an economic deposit?

Yes, potentially it is, but this will be determined by further drilling.

Are you in discussions with potential strategic partners on your other properties?

Yes, management is continually assessing new opportunities to add value for our shareholders. At a high level, we have a dual track strategy of 1) discovering more high-grade uranium at Moore, and 2) prospect generation from our portfolio, ex-Moore, as exemplified by the 2 option agreements with Orano & Azincourt. We would like to find partners at our Falcon Point, Mann Lake & Yurchison properties, which we own 100% of.

What should readers make of the occasional showings of high-grade Cobalt & Nickel? Just noise, or potentially more important?

This is positive, however, the extent of how meaningful the discovery of Cobalt & Nickel is will be determined with further drilling. It’s fair to say it’a an interesting development that will certainly be followed up on.

Why should readers consider buying shares of Skyharbour Resources?

When the uranium market turns, it can turn fast, and stock gains can be large. The underlying uranium price can double or more in under a year. This has happened twice in the past 12 years or so. Are we at an inflection point where select uranium stocks are poised for big gains? We might be, and if not this year, I think it’s likely in 2020. If one believes as I do that the uranium price is headed higher and that nuclear power is hear to stay, then Skyharbour Resources is a good bet.

With 6 properties in the best uranium basin on the planet, and partners funding a significant portion of this year’s exploration, there’s a decent chance of new discoveries and favorable drill hole results. Skyharbour Resources (TSX-V: SYH) (OTCQB: SYHBF) will be very active on multiple fronts this year. The same can not be said about many other uranium juniors. {see latest press releases} {corporate presentation}

Thank Jordan, a very good update and review of Skyharbour Resources, I look forward to drill results from you and your partners later this year.

Disclosures: The content of this interview is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Skyharbour Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Skyharbour Resources are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this interview was posted, Peter Epstein owned no shares in Skyharbour Resources, and it was an advertiser on [ER]. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.