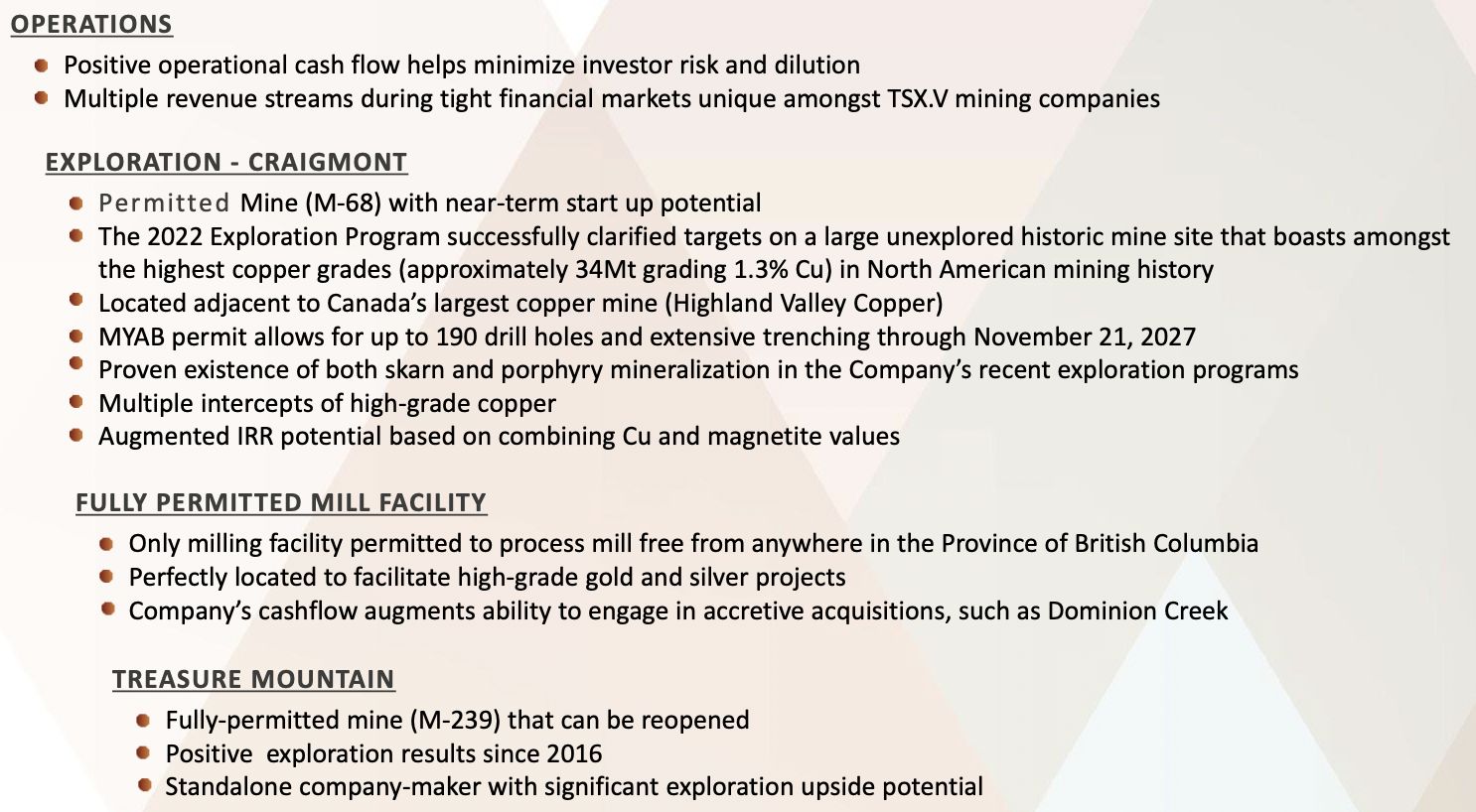

Nicola Mining (TSX-v: NIM) / (OTCQX: HUSIF) has just announced positive operating cash flow from its innovative business operations, which include a permitted gravel pit and rock quarry, gravel, ash & soil segments, and an operating gold / silver mill facility that is currently producing gold concentrate with Osisko Development (NYSE: ODV).

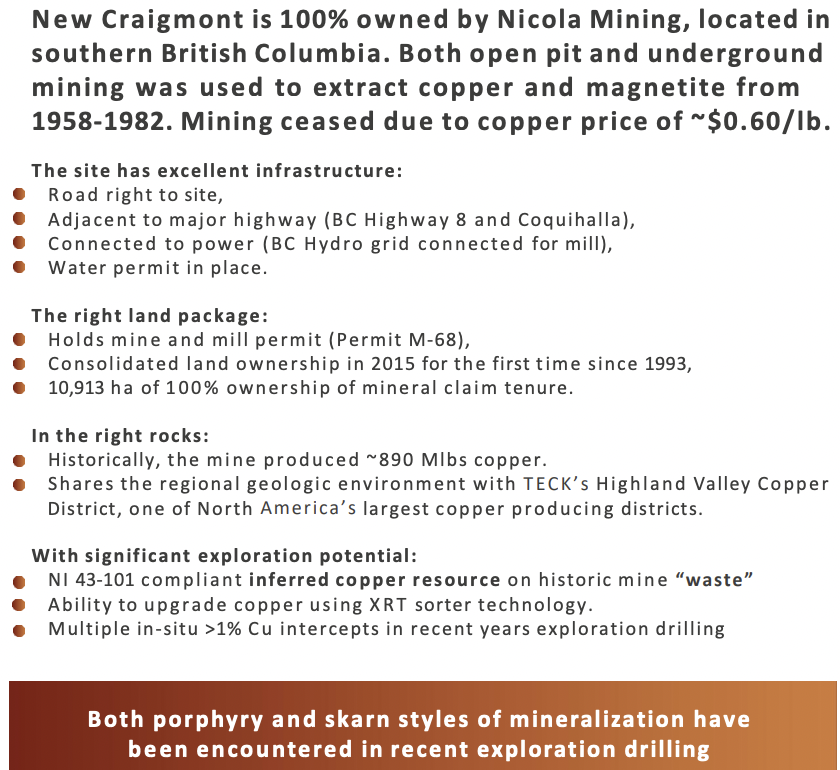

In addition, Nicola holds two valuable mine permits: M-68 (for the 100%-owned New Craigmont Copper Project) and M-239 (for the 100%-owned Treasure Mountain Mine Project), the latter of which is silver focused. CEO Peter Espig points out that obtaining mining permits in B.C. typically takes 10-15 years.

Last month Nicola commenced shipping concentrate produced jointly with Osisko Development at the strategically valuable Merritt mill facility. To date ~160 dry metric tonnes of gold (“Au”) concentrate, grading ~90 g/t Au, has been shipped.

The Company has secured an off-take agreement with Ocean Partners U.K. Ltd. to sell the concentrate. Ocean Partners is a strong partner and a shareholder in Nicola that could help fund & advance acquisitions of stranded deposits and larger opportunities.

The Merritt mill + lined tailings storage facility is unique as it sits on ~950 acres of free-hold land. It has highway access and is connected to the grid. B.C.’s hydroelectric power offers some of the most sustainable, greenest, low-cost power on the planet.

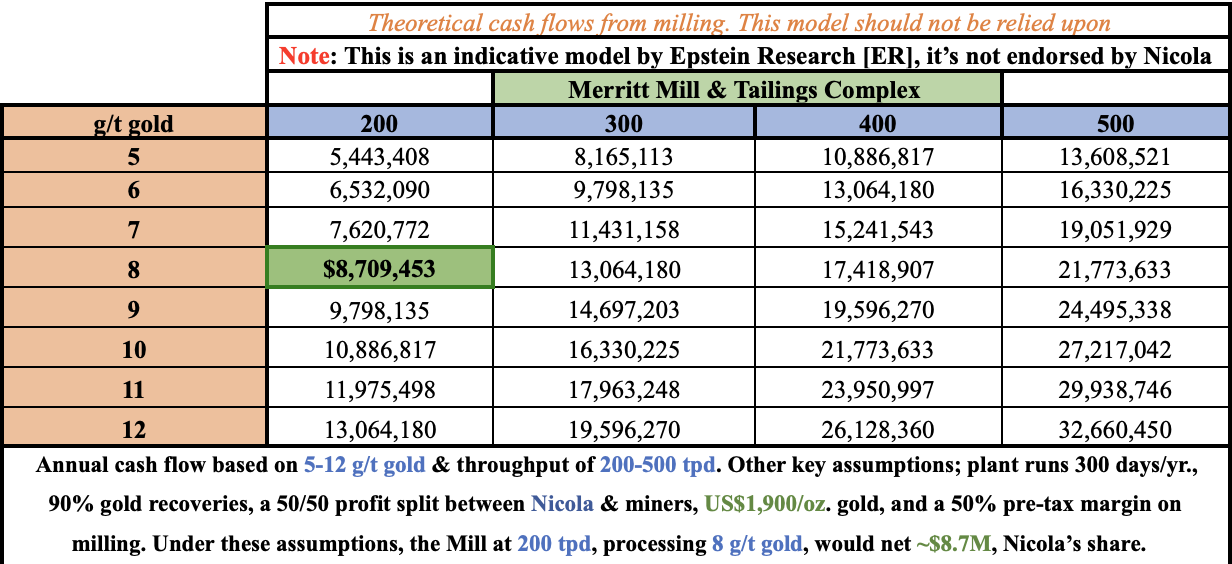

The mill operates at up to 200 tonnes per day (“tpd”), but could be expanded to 500 tpd if warranted.

cash flows from gravel, ash, soil & other sources…

The mill site is industrial-zoned and is the only facility in B.C. permitted to accept Au & Ag feed from anywhere in the province. In my view, a high quality mill & tailings storage facility with decades of operating life ahead should be worth up to 10x annual cash flow.

As can be seen in the chart below, cash flow has the potential to grow to significant sums, but the mill has been vastly underutilized for years due to third-party mines being slow to obtain mining permits.

That should change with higher Au prices… Owners are keenly incentivized to get their deposits permitted. CEO Espig notes that there are many dozens of deposits within reasonable trucking distance, {see slide 7 of corporate presentation}.

It’s important to recognize the income Nicola’s valuable assets are currently generating. Operating income could amount to ~$11M this year, (annualizing first half results, not company guidance). That’s significant cash flow for a company with an Enterprise Value {market cap + debt – cash} of ~C$48M.

Cash will be invested into drilling the New Craigmont Copper Project (“NCP”) & share buybacks. Nicola is authorized to buy back up to 4M shares.

As cash builds, $6.4M [current assets – current liabilities on 6/30/23], management continues to actively consider acquisitions of additional properties. Today’s junior mining environment offers a huge buyer’s market.

Management’s investment + profit-sharing agreement (for a combined 75% economic interest) in the high-grade Dominion Creek mine is a prime example of the compelling stranded deposits opportunity.

Switching gears to another company-making crown jewel, why am I so excited by the NCP when there are dozens of promising Cu-heavy projects around the world? Nicola has a potentially world-class porphyry / high-grade skarn Cu system.

of global peer Cu projects, ask yourself…

- How many are fully-funded for robust exploration & development with internally-generated, positive cash flow?

- How many have Both high-grade & large-scale potential?

- … have extensive historical exploration work, incl. 12,000+ meters of drilling?

- … have potential world-class projects in a brownfield (past-producing mine) setting?

- … are in a Tier-1 jurisdiction like B.C., Canada?

- … are surrounded by clean, green hydro-electric power?

- … have ample access to highways, water, labor & mining services?

- … have strong relationships with local communities & First Nations groups?

- … have 5-yr. “carte blanche” exploration permits?

- … have mine permits in place facilitating a fast-track to production?

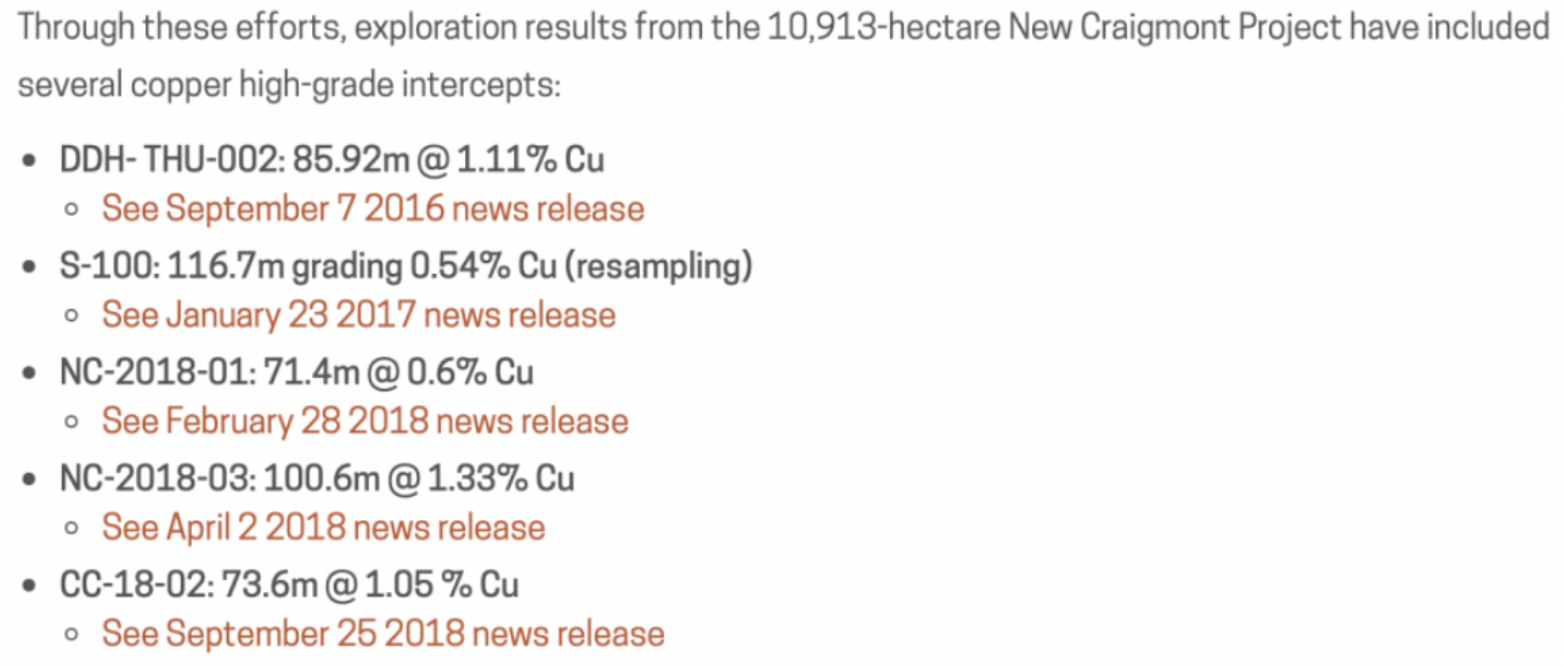

Not many projects check most of these boxes. I strongly believe that despite its early stage, the past-producing NCP is moderately de-risked. Management recently announced the completion of the first four drill holes and has logged & shipped core to the lab.

Initial drilling this year is focused on skarn mineralization ~500 m east of the historic pit. Assays should start arriving by the end of August.

After a two-year administrative process, management received an area-based drill permit in 4th qtr. 2022 allowing for five years of in-depth exploration (190 holes + 12 km of trenching + 12 km of bulk sampling).

Key to understanding this valuable drill permit is that it opens up project areas never before explored. In 2015 management consolidated a significantly larger land package than the former Craigmont mine had and commenced comprehensive exploration activities.

It’s critically important to note that the NCP’s high grade AND large scale potential come from it being on the, “corner lot” for prolific Cu mineralization.

The NCP sits at the intersection of the Nicola & Highland Valley faults. Directly north is Highland Valley Copper’s multiple porphyry pits, owned by Teck Resources, and then along the Nicola fault, New Gold’s New Afton mine & Hudbay’s Copper Mountain mine.

Newmont/Newcrest, Seabridge Gold, Centerra Gold, Taseko Mines & Tudor Gold also own major Cu-focused mines/projects in B.C.

In addition to these eight prominent companies, players from around the world are seeking entries into Canada as jurisdictions in S. America & Africa become more challenging {see recent headlines in Niger, Mali & Burkina Faso}.

Local community opposition, political populism, water/infrastructure constraints, safety/security — are of increasing concern. In addition, China & Russia are being shut out of N. America & Europe, leaving them scrambling for higher-risk opportunities in Africa.

some strong drill results, but the NCP is vastly under-explored…

The Craigmont mine, 14 km from Merritt, British Columbia, was the highest grade / largest Cu mine of its time (1958-82). It produced ~900M pounds of Cu at an average grade of 1.28%. However, from the early-1980’s to 2016 fragmented ownership prevented any meaningful exploration.

Since 2016, completion of a Z-axis Tipper Electromagnetic (“ZTEM”) survey, soil sampling, property-scale mapping, electromagnetic & induced polarization programs were combined with a detailed review of historical data.

Further work included 10,498 meters of diamond + 1,869 m of RC drilling, upgrading Cu grades through the utilization of X-Ray Transmission sorter technologies, and publishing a NI 43-10 technical report on historic mine waste terraces.

As mentioned, Nicola owns 50% [and a 75% economic interest] in the Dominion Creek project, which reported grab samples in July, 2020 averaging 61.3 g/t Au + 174 g/t Ag. Dominion has submitted a mine plan for a permit to collect a 10,000-tonne bulk sample and remains optimistic that the permit will be issued this year.

The Company also owns the fully-permitted, Treasure Mountain Silver project. Treasure Mountain hosts high-grade Ag in south central B.C. Soil samples from 2019 & 2020 returned strong values including; 813 g/t Ag + 0.52 g/t Au + 19% zinc & 4.66% Cu.

A vein sample came back at 1,300 g/t Ag, 2.59 g/t Au, 1.16% Cu, 27.4% lead & 27.2% zinc. Treasure Mountain is permitted to mine 60,000 tonnes/yr. Importantly, management is pursuing a 5-yr. exploration permit (like the one it has on the NCP) for Treasure Mountain.

With upcoming drill results + possible M&A + share buybacks & positive cash flow — Nicola Mining (TSX-v: NIM) / (OTCQX: HUSIF) should be attracting a lot more attention in the months to come. Readers are encouraged to visit the Company’s website & review the corporate presentation.

Disclosures / Disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Nicola Mining, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market-making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Nicola are highly speculative, not suitable for all investors. Readers understand and agree that investments in small-cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Nicola Mining is an advertiser on [ER] and Peter Epstein owned shares and/or stock options in the Company.

Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reason whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.