Adjusted for inflation, the silver (“Ag“) price peaked at ~$195/oz. in 1980. The last multi-yr. episode of very high inflation was from 6/30/73 to 12/31/82 when it averaged 8.95%.

After 23 months above 5%, U.S. inflation is back below 4%, but investors & the Fed are worried that inflation & interest rates are not contained. Inflation has been inching back up and the 10-yr. treasury yield jumped 45 basis points in September, plus 28 bps this month to 4.82%, the highest since 2007.

I firmly believe precious metal prices will continue last week’s trend higher. Today the spot Ag price is 72% below $83/oz., the average inflation-adj. level for all of 1980!

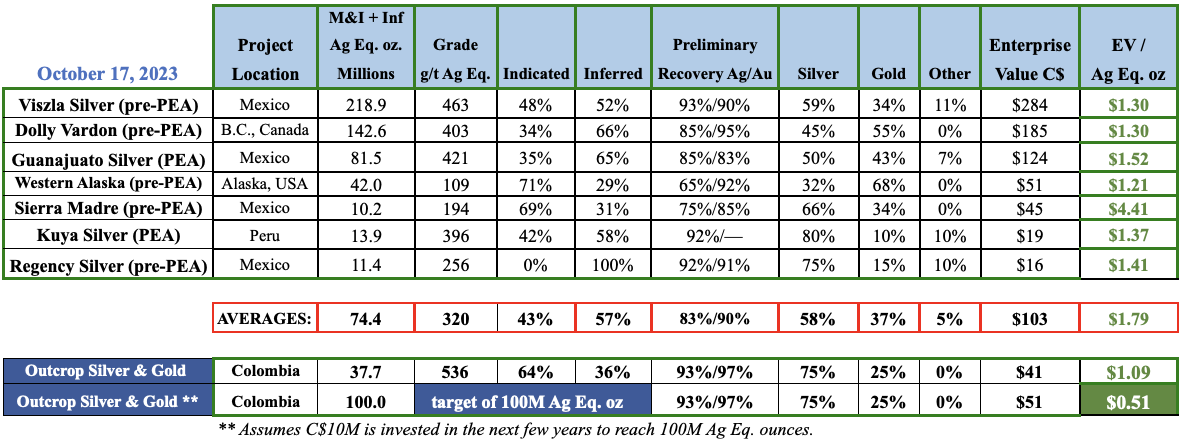

If one believes that precious metals will outperform in the coming quarters and years, and that silver often rises more than gold in bull markets, investing in Ag-heavy juniors like Outcrop Silver & Gold (TSX-v: OCG) / (OTCQX: OCGSF) makes tremendous sense. Although pre-production, Outcrop has already checked several key investment boxes.

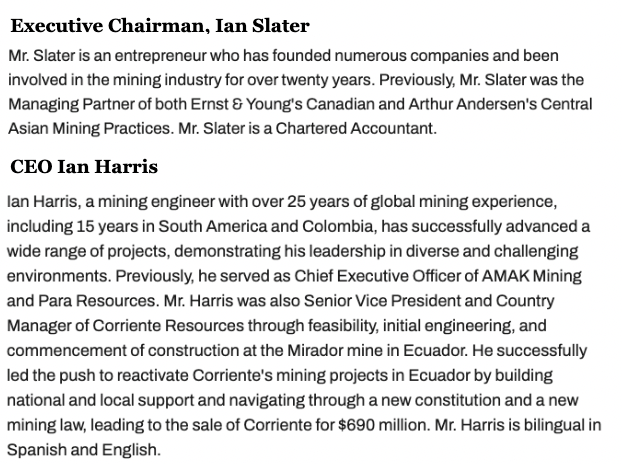

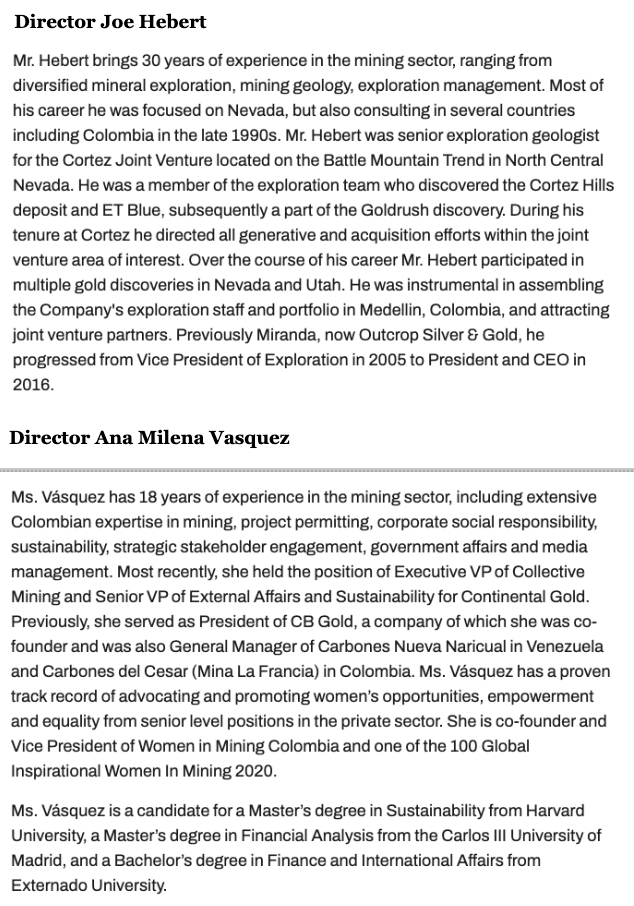

Led by CEO Ian Harris and surrounded by a seasoned group of execs & board members with explicit boots-on-the-ground experience in S. America & Colombia. Mr. Harris has lived in S. America / Colombia for 15 of his 25 year (Mining Engineer) career. Please take a moment to read the five bios below.

Outcrop’s 27,000+ hectare, 100%-owned Santa Ana project in Colombia is ~190 km from the Country capital city of Bogota. It hosts very high-grade silver, {see comps below}, and has a clear path to 100M Ag Equiv. ounces.

Santa Ana covers a majority of the Mariquita District, the highest-grade primary silver district in Colombia, where mining dates back to the late 1500s. Outcrop Silver’s drilling indicates that mineralization extends to a depth of at least 370 m. In total, > 46 km of mapped & inferred vein zones have been found.

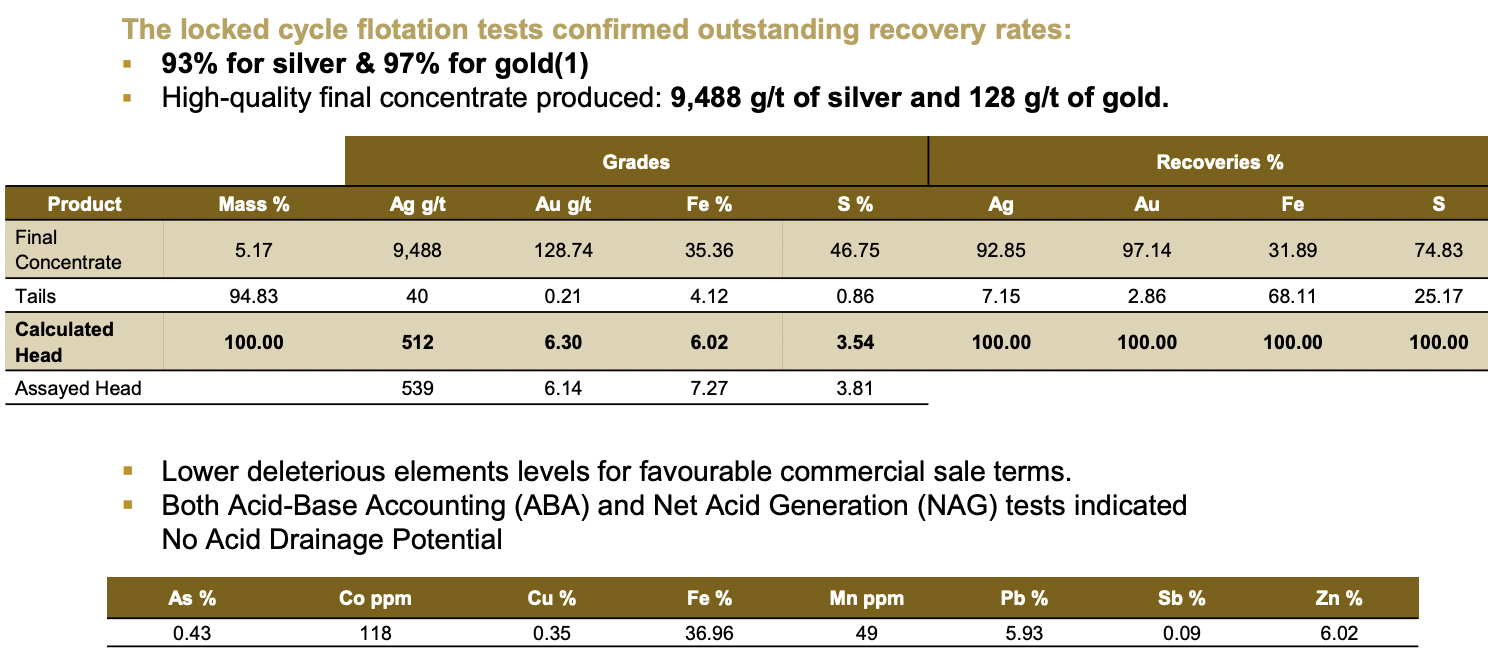

The resource has already demonstrated strong preliminary metallurgical results; {93%/97% Ag/Au recoveries from floatation alone} — with possible upside if combined with gravity separation. These preliminary results are extremely important.

CEO Harris believes that high recoveries of ONLY silver & gold could enable Outcrop to produce doré bars onsite, thereby getting paid for 98%-99% of the contained precious metals. Compare that to payables on peer concentrates ranging from ~75% to 90%. And, Santa Ana’s preliminary recoveries at 93%/97% Ag/Au are better than peers at an average of ~83%/90%.

Given that Outcrop’s resource is 75% silver & 25% gold — with low impurities + high preliminary recoveries — tailings from a mining operation (with no leaching or cyanide) should be environmentally-friendly.

For example, no acid drainage is expected. Importantly, there are past-producing mines on Outcrop’s property, and mining in the region dates back centuries.

According to the latest corporate presentation, Santa Ana enjoys, “highway access, grid power, water, strong community support, and excellent security conditions.” All of these critical factors suggest permitting should be fairly straightforward.

An initially small-scale mine could be up & running within 4-5 years. Mr. Harris points out that many of S. Americas’ large, high-grade, narrow vein mines, like Zijin Mining’s giant Buritica mine, started out small.

As proof of concept that the narrow high-grade veins hold together along strike and to depth, management delivered a maiden mineral resource estimate (MRE) of 37.7M Ag Eq. ounces based on drill results on just seven veins. Importantly, 64% of the resource is in the Indicated category.

The reason management is comfortable with a conceptual resource target of 100M Ag Eq. ounces is that there are 23 mapped veins (so far), 16 of which have no ounces booked, and those [7 + 16 = 23] veins are found on 20% of the total property package.

While it’s too soon to make even a rough estimate of the resource potential, one cannot rule out blue-sky figures above 100M ounces given the overall size of the property, analog high-grade, narrow vein projects & mines and the parameters of the known resource.

Dolly Varden has ~143M Ag Eq. ounces (34% in the Indicated category) and an Enterprise Value [EV] {market cap + debt – cash} of ~C$184M (C$1.30/ Ag Eq. oz.). Like Outcrop, its flagship project in B.C.. Canada is pre-PEA stage. Dolly Varden’s C$1.30/oz. valuation is close to Outcrop’s corresponding C$1.09/oz.

Readers should note that 64% of Outcrop’s resource is Indicated vs. 34% for Dolly.

Outcrop has better preliminary metallurgy with initial recoveries of 93% Ag / 97% Au, vs. Dolly at 85%/95%. Like many juniors, Dolly proposes to use cyanide, Outcrop does not.

At 75% Ag, Outcrop is a better pure-play on the silver price than Dolly at 45%. Outcrop has a higher Indicated + Inferred Ag Eq. grade at 536 g/t vs. 403 g/t. Higher grade provides for a margin for error.

Dolly is in a less risky jurisdiction, but Outcrop could reach initial production sooner (via a smaller mine plan) with a potentially easier permitting path. As mentioned, Dolly & Outcrop are pre-PEA, so it’s impossible to compare project economics.

However, one important factor, labor costs, are much lower in Colombia at roughly a fifth or a sixth that of Canada (Australian & U.S. labor costs are even higher). Mexico’s labor costs have increased a lot lately as its currency has strengthened considerably vs. the US$.

Both Dolly & Outcrop appear to be strong takeover targets. If one assumes that Outcrop can reach 100M Ag Eq. ounces in the next few years by spending an additional C$10M on drilling, its pro forma EV/oz. figure is C$0.51/oz.

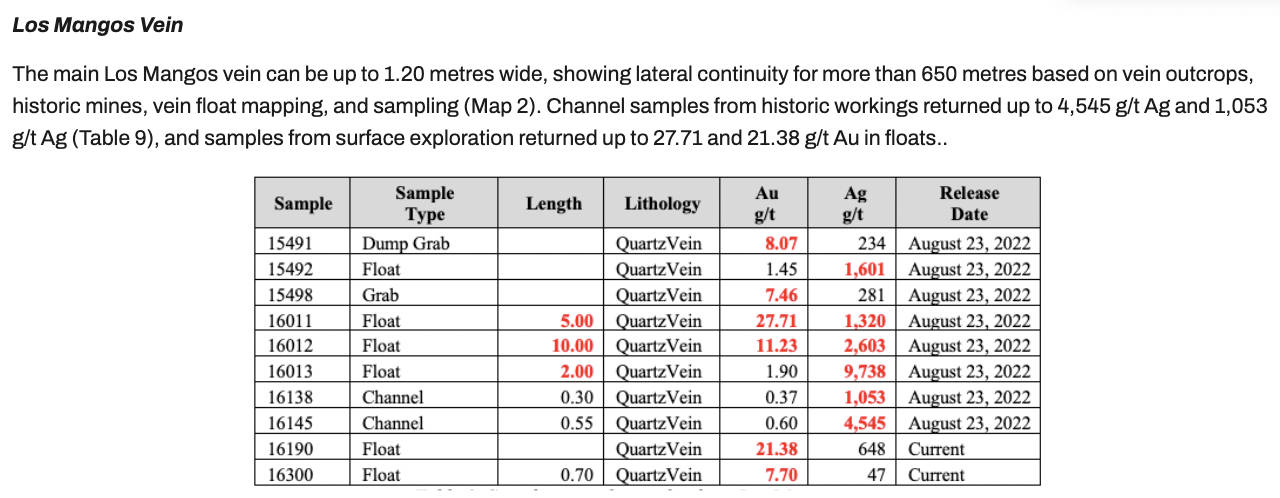

The description above of the Los Mangos vein comes from the April 26, 2023 press release announcing the MRE. This is just one of many targets not yet included in the resource.

Notice the float sample lengths of 2 to 10 meters at bonanza grades. Float samples were taken on boulders that are not necessarily connected to nearby mineralization. For instance, the boulders may have rolled down the side of a mountain.

In terms of country risk, Colombia sits one notch ahead of Mexico, and 1 & 2 spots, respectively, behind Chile & Peru. It ranked above Papua New Guinea, South Africa and the Argentinian provinces of Catamarca, Jujuy & Salta. {source: Fraser Institute Mining Survey, 2022}

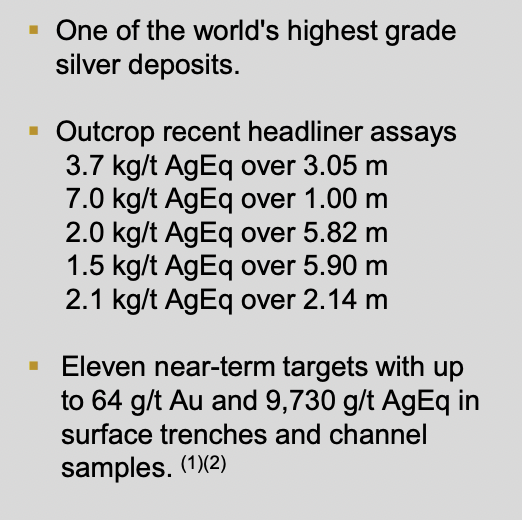

Outcrop Silver has reported some spectacular drill intervals…

The average grade of the above intervals is ~3,260 g/t Ag Eq. (over multiple meters), equivalent to a tremendous 38 g/t Au Eq. Drill results over the next several months should continue to show very high-grades over narrow widths. Next year, management will update the MRE with a very significant increase in ounces.

In addition to the promising Santa Ana project in Colombia, Outcrop is pursing several U.S. projects via the proposed acquisition of Zacapa Resources.Zacapa has a sizable gold project in Nevada that’s surrounded by AngloGold Ashanti, Kinross & Augusta Gold. AngloGold has been vocal about its big plans for the Beatty district where it has amassed an 8M oz. gold resource.

Augusta’s flagship project is well advanced with a BFS on the way. It seems likely to me that Zacapa’s South Bullfrog project will play a meaningful role in the rapid development of the district.

Zacapa also has an interesting porphyry copper exploration play immediately north of BHP’s past-producing San Manuel-Kalamazoo mining complex in Arizona, USA. Both of Zacapa’s projects will be on the back burner. The main focus this year and next is Santa Ana.

Outcrop Silver & Gold (TSX-v: OCG) / (OTCQX: OCGSF) has plenty of cash to keep drilling for several more months. As investors continue to see great drill results, interest in the Company should grow. Silver is up 12% from its October low and was above $25/oz. as recently as July. Now could be an ideal time to increase one’s bets on silver juniors.

Disclosures / disclaimers: The content of this article is for information only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about Outcrop Silver & Gold, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of Outcrop Silver & Gold are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own financial advisors before making investment decisions.

At the time this article was posted, Peter Epstein owned stock in Outcrop Silver & Gold and the Company is an advertiser on [ER].

While [ER] believes it is diligent in screening out companies that are unattractive investment opportunities, [ER] cannot guarantee that its efforts will be, (or have been), successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not an expert in any company, industry sector or investment topic.